News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

This week’s crypto market saw a rare convergence of big-ticket fundraising, aggressive corporate Bitcoin (BTC) accumulation, and payments-focused M&A—signals that the industry’s next phase may be defined less by new tokens and more by consolidation, treasury engineering, and tighter links to traditional financial rails.

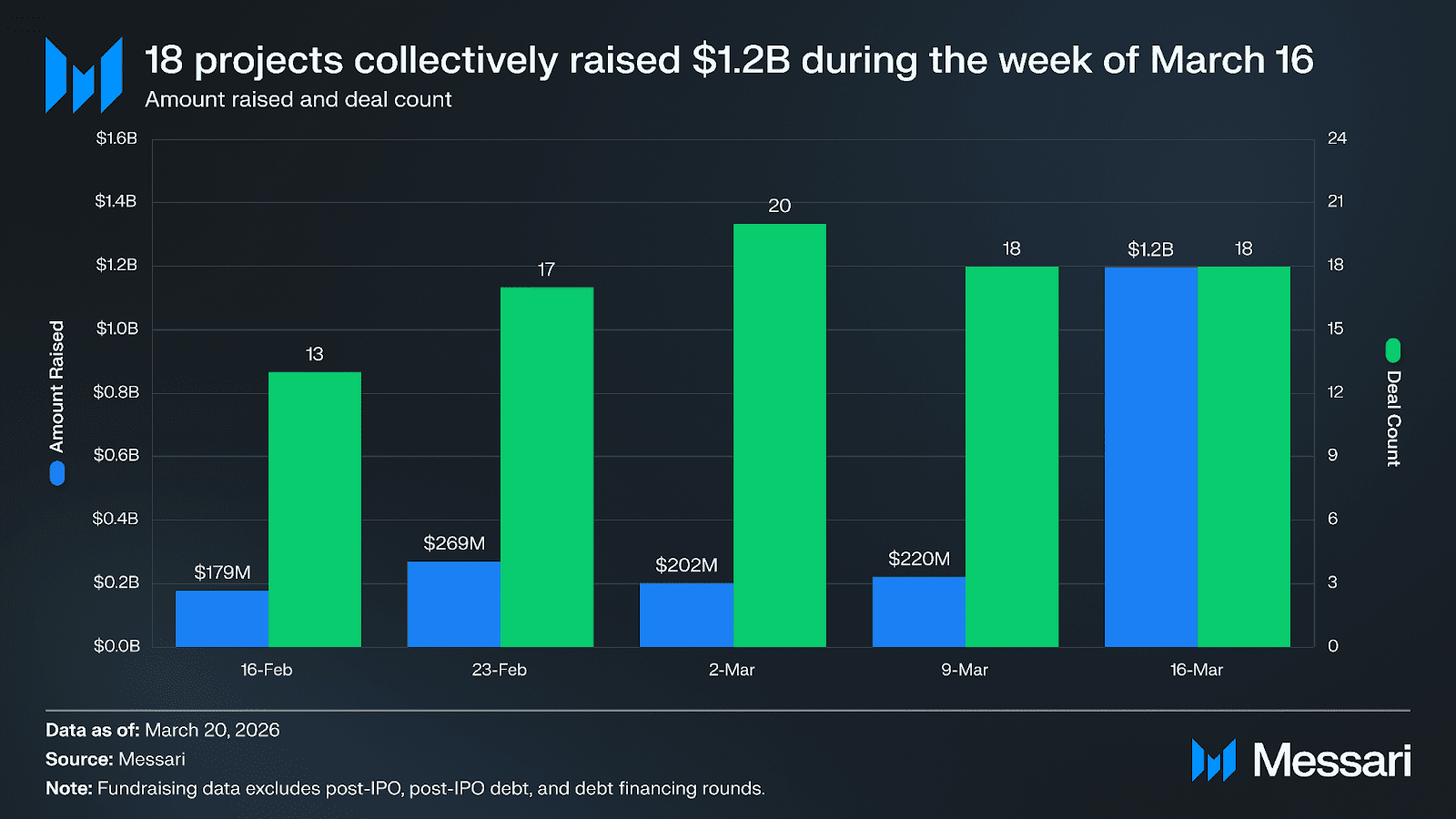

Data compiled by Messari on Sunday ET (March 23) showed 18 projects raised roughly $1.2 billion over the week, with capital clustering around a handful of heavyweight rounds. Kalshi led the tape with a $1 billion raise, while Bluesky brought in $100 million, underscoring continued investor appetite for regulated-market infrastructure and consumer-facing networks even as broader risk sentiment remains choppy.

Beyond the headline deals, funding flowed into niche infrastructure plays. Ironlight raised $21 million to build out 'tokenized securities' infrastructure—tools that aim to bring real-world assets and regulated instruments onto blockchain rails. GENCY AI secured $20 million to develop an AI- and blockchain-based advertising network, a segment investors increasingly view as a test case for whether onchain identity, attribution, and payments can compete with Web2 incumbents.

Early-stage capital also targeted market structure and execution technology. Silhouette, an exchange designed to support confidential execution of onchain orders, closed an $8 million seed round, reflecting persistent demand for privacy-preserving trading in public-blockchain environments. Derivio raised $6 million to develop an AI-driven trading terminal, part of a broader wave of products aiming to compress research, execution, and risk oversight into unified interfaces.

In parallel, corporate digital-asset treasury strategies continued to expand, with Bitcoin accumulation serving as both a balance-sheet narrative and a capital-markets strategy. Strategy ($MSTR) deployed approximately $1.57 billion to purchase 22,337 BTC, lifting its total holdings to 761,068 BTC. Messari put the company’s average purchase price for the latest tranche at roughly $75,696 per coin—an indication that large-scale buyers remain willing to add exposure at levels near recent cycle highs, betting that 'liquidity inflow' and institutional adoption will sustain the long-term bid.

Japan-listed Metaplanet, meanwhile, strengthened its accumulation playbook via a $255 million equity raise. The company introduced a net-asset-value-linked warrant structure designed to increase BTC per share—an approach that mirrors the growing sophistication of 'Bitcoin treasury' vehicles seeking to optimize dilution, leverage, and market timing. Stack BTC raised $2.4 million and outlined a dual track of acquiring cash-generating businesses while continuing additional Bitcoin purchases, a model that blends operating income with digital-asset exposure rather than relying purely on capital markets.

Consolidation was equally visible on the M&A front, spanning capital markets, payments, and infrastructure. Crypto market maker GSR acquired Autonomous and Architech for $57 million, positioning the combined entity as an integrated capital-markets and treasury platform for tokenized organizations. The aim, according to Messari’s summary, is to cover the full project lifecycle—token design, 'liquidity strategy,' exchange listings, and treasury management—packaging services that previously required multiple vendors and fragmented execution.

The week’s most consequential deal centered on stablecoins and payments. Mastercard ($MA) agreed to acquire stablecoin infrastructure firm BVNK for up to $1.8 billion, a move that would deepen Mastercard’s push to connect onchain settlement to its global network. BVNK supports stablecoin payments across more than 130 countries and is expected to become a core layer in Mastercard’s effort to expand interoperability between fiat systems and digital assets—an increasingly strategic battleground as stablecoins migrate from crypto-native rails into mainstream cross-border commerce.

Elsewhere, prediction market Polymarket acquired DeFi infrastructure company Brama to streamline user experience and reduce onchain complexity—an acknowledgement that interface friction, wallet management, and transaction flow remain key bottlenecks to mass adoption even when demand exists.

Venture investors also used the week’s activity to frame where market structure may be heading. Sunny Shi argued that decentralized-exchange-based perpetual futures could expand beyond crypto into traditional assets such as equities and commodities, potentially capturing meaningful share of the global retail derivatives market. Simon Dedic pointed to the emergence of an 'agent-centric economy'—where autonomous software agents transact at high frequency—as a catalyst for a sharp rise in DeFi usage, warning that today’s lending protocols, AMMs, oracle systems, and wallets were not designed with autonomous, always-on participants in mind.

At the same time, the industry’s growing reliance on AI drew more nuanced assessments. Carl Vogel said AI agents can meaningfully improve diligence and market analysis, but emphasized that trust, relationships, and human judgment remain decisive in final investment decisions—an important counterweight as capital allocators weigh automation against accountability.

Taken together, the week’s fundraising, treasury accumulation, and acquisitions suggest crypto’s center of gravity is shifting toward 'institutional-grade' infrastructure and integrated platforms. As payments giants pull stablecoin rails closer to traditional networks and service providers consolidate offerings for tokenized capital formation, the market’s next re-rating may depend less on narratives and more on execution, compliance, and scalable distribution.

Comment 0