News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

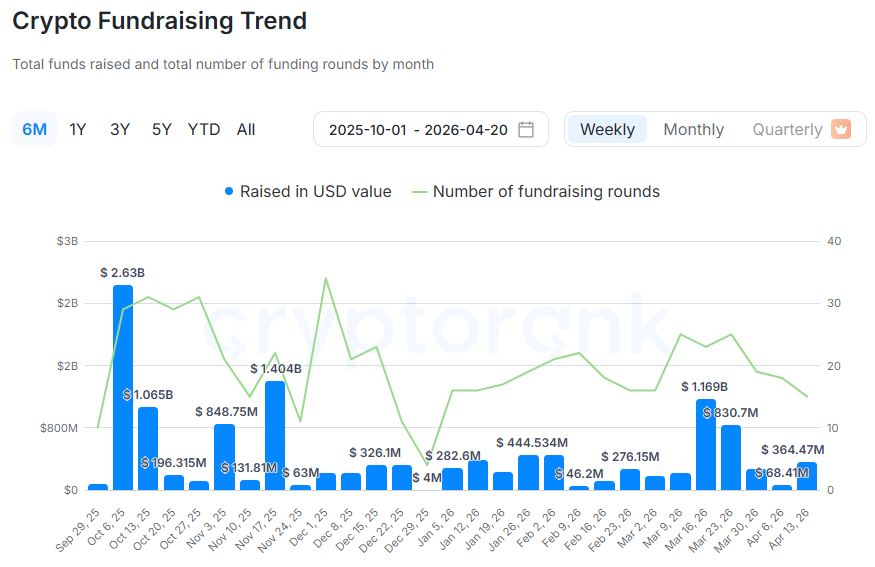

Crypto funding surged in the third week of April, with weekly capital raised jumping to roughly $364.5 million even as the number of deals declined—an indication that investors are concentrating their bets into fewer, larger transactions.

According to data compiled by CryptoRank, crypto and blockchain companies closed 15 funding rounds between April 13 and April 19 UTC, raising a combined $364.47 million. That compares with the prior week (April 6–12 UTC), when 18 rounds brought in $68.41 million. While deal count fell from 18 to 15, total funding expanded more than fivefold, underscoring a shift toward ‘mega-round’ dynamics rather than broad-based early-stage momentum.

The week’s activity was headlined by a cluster of outsized transactions across payments, derivatives, and on-chain trading infrastructure. Deutsche Börse-backed Payward raised $200 million in an undisclosed round, one of the largest financings reported during the period. Paxos Labs secured $12 million in an undisclosed round led by Blockchain Capital, while Drift Protocol raised $147.5 million via debt financing backed by Tether, highlighting continued appetite for structured capital in established on-chain venues.

Traditional venture-style rounds also appeared, including Slash’s $100 million Series C led by Ribbit Capital and Spectre’s $20 million Series A anchored by New Enterprise Associates. Seed-stage rounds remained active in count, with Pumpcade raising $5 million in a seed round involving Jump Crypto and Nava AI securing $8.3 million in seed funding led by Polychain Capital.

M&A activity played a notable role in the week’s headline totals. Zengo was acquired in a $70 million deal by eToro, reflecting ongoing consolidation among wallet and consumer-facing crypto platforms. In another attention-grabbing transaction, Bitnomial was acquired for $550 million in a deal involving Payward, signaling that exchange-adjacent infrastructure and regulated derivatives capabilities remain strategically valuable even amid uneven market conditions.

Despite the week’s spike, broader indicators point to a cooling environment. CryptoRank’s monthly tallies show January closed with 69 deals totaling $1.34 billion, February recorded 77 deals totaling $894.34 million, and March saw 101 deals totaling $2.6 billion. In April so far, 40 rounds have collectively raised about $496.78 million, suggesting the month’s pace remains subdued unless additional large financings land late in the period.

Over the past 30 days, CryptoRank’s investment activity index fell 31% month over month to a ‘Low’ reading. The dataset recorded 84 rounds during that window, down 9.68% from the prior month, while total funding slipped to roughly $3.0 billion—about a 37.3% decline—signaling that both deal flow and aggregate capital are softening in tandem. Average round sizes clustered between $3 million and $10 million, with seed investments the most frequent stage by count.

Sector allocation data suggests capital continues to follow ‘payments’ as the dominant theme. Over the past six months, payments accounted for 34.3% of funding activity, followed by decentralized exchanges (DEX) at 19.42%, real-world assets (RWA) at 18.6%, Binance Alpha at 14.46%, and API-related projects at 13.22%. The mix highlights a market still willing to fund revenue-linked rails and trading infrastructure, while also keeping exposure to tokenization narratives.

On the investor side, Coinbase Ventures led activity by deal count with 29 investments over the tracked period, followed by GSR (16), Tether (15), Animoca Brands (14), Castrum Capital (13), and both a16z Crypto and Paradigm with 11 deals each. The roster points to a blend of strategic crypto-native balance sheets and established venture franchises continuing to set the tempo in a more selective funding market.

Overall, the week’s data paints a two-speed picture: marquee financings and acquisitions can still pull significant dollars into the sector, but the underlying trend in deal frequency and broader activity metrics suggests investor sentiment remains cautious, with capital increasingly concentrated in companies viewed as durable infrastructure or strategically essential platforms.

🔎 Market Interpretation

- Funding spiked despite fewer deals: April 13–19 saw $364.47M across 15 rounds versus $68.41M across 18 rounds the prior week—capital is concentrating into fewer, larger checks.

- “Mega-round” dynamics dominate: Large financings (e.g., Payward $200M; Drift Protocol $147.5M debt) drove totals, masking weaker breadth in early-stage momentum.

- M&A inflated headline numbers: Wallet and derivatives infrastructure consolidation (e.g., Zengo acquired for $70M; Bitnomial acquired for $550M) indicates strategic buyers are active even amid uneven conditions.

- Broader market is cooling: The investment activity index fell 31% MoM to “Low,” with ~37.3% decline in total funding and fewer rounds, signaling tightening risk appetite.

- Capital preference remains pragmatic: Funding continues to favor categories tied to payments and trading infrastructure, suggesting investors prioritize business models closer to revenue and essential market plumbing.

💡 Strategic Points

- Watch concentration risk: Weekly totals can look strong when driven by a handful of mega-rounds; assess market health using both deal count and median/average round size.

- Debt financing is back for mature venues: Drift’s debt-backed raise highlights demand for structured capital where cash flows, collateral, or strategic backers (e.g., Tether) can support non-dilutive funding.

- M&A signals strategic value in regulated rails: Large acquisitions in exchange-adjacent and derivatives infrastructure imply premiums for compliance-ready, licensed, or institutional-grade capabilities.

- Seed remains active but smaller: Seed rounds lead by count, but most checks cluster around $3M–$10M; early-stage teams may face tougher follow-on conditions unless they show traction quickly.

- Sector positioning: Over six months, funding emphasis skews to payments (34.3%), then DEX (19.42%) and RWA (18.6%)—suggesting a barbell of (1) revenue rails and (2) tokenization/trading narratives.

- Investor leadership mix: Coinbase Ventures leads by count, alongside GSR, Tether, Animoca, a16z Crypto, Paradigm—implying continued influence of both strategic balance sheets and top-tier VC in a selective market.

- Operational takeaway for founders: Position fundraising around durable infrastructure, clear monetization, and regulatory readiness; expect diligence to focus on unit economics, custody/security posture, and go-to-market defensibility.

📘 Glossary

- Mega-round: An unusually large financing round that meaningfully lifts total funding figures for a period, often concentrated in later-stage companies.

- Deal count: The number of completed funding rounds; a measure of breadth of investor activity.

- Undisclosed round: A financing where key terms (valuation, structure, sometimes investors) are not publicly revealed.

- Debt financing: Borrowed capital that must be repaid (often with interest); can be less dilutive than equity but increases financial obligations.

- Series A / Series C: Venture equity rounds typically indicating increasing maturity—Series A (early scaling) and Series C (later-stage expansion).

- Seed round: Early-stage funding used to build a product, validate market fit, and establish initial traction.

- M&A (Mergers & Acquisitions): Transactions where companies buy, merge with, or absorb other businesses; often reflects consolidation or strategic capability acquisition.

- DEX (Decentralized Exchange): On-chain trading venue using smart contracts rather than a centralized operator.

- RWA (Real-World Assets): Tokenized representations of off-chain assets (e.g., treasuries, credit, real estate) brought onto blockchain networks.

- On-chain trading infrastructure: Protocols and tooling that enable trading, liquidity, execution, and risk management directly on blockchain.

Comment 0