News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Ethena’s native token ENA jumped over 20% following its listing on South Korea’s largest crypto exchange Upbit on July 11. While investors initially cheered the debut, concerns are mounting over the sustainability and regulatory vulnerability of the underlying system—USDe, a synthetic stablecoin backed not by fiat or treasuries, but by crypto derivatives.

The listing marks Ethena’s full entry into the Korean retail market after earlier listings on Bithumb in February and Coinone in April. Upbit’s dominance over local trading volumes gave ENA an immediate liquidity boost, yet analysts warn that its complex structure—combining crypto collateral, perpetual futures, and yield incentives—could expose the system to the same kind of systemic failure seen in Terra’s 2022 crash.

A “Crypto-Native” Dollar, but at What Cost?

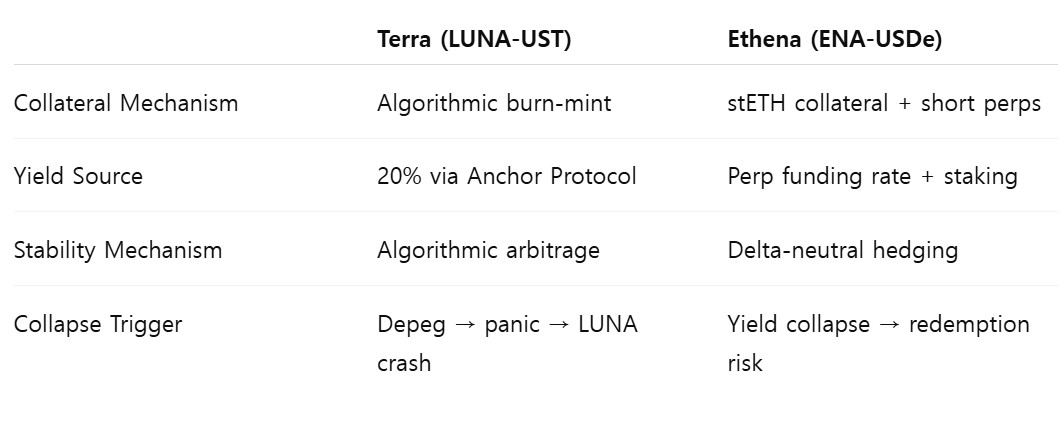

Ethena describes USDe as a fully-backed, censorship-resistant, and scalable synthetic dollar. Unlike traditional stablecoins such as USDT or USDC, which are backed by fiat reserves, USDe is minted when users deposit Ethereum (ETH) or staked ETH (stETH) as collateral. The protocol then opens short positions in ETH perpetual futures to hedge against market volatility—a strategy known as delta-neutral positioning.

Staked assets and funding rate spreads become yield-generating sources, converting USDe into sUSDe, which at one point offered more than 60% annualized yield. Today, that figure has dropped below 5%, raising questions about the longevity of this model.

While marketed as innovative, the mechanism is essentially a basis trade: earn the funding rate by shorting perpetuals while holding the underlying asset. This arbitrage-like setup is fragile, depending on consistently positive funding rates and tight price correlation between spot and futures markets.

Regulatory Concerns Cloud the Horizon

A more pressing concern may lie in Washington. Ethena’s USDe structure appears to violate core provisions of the GENIUS Act, passed by U.S. lawmakers in June. The law mandates that any stablecoin must (1) maintain 1:1 backing with fiat or government securities and (2) refrain from offering interest or yield to users.

USDe fails on both counts: it’s backed by crypto and provides yield. Ethena has reportedly held closed-door meetings with the SEC to clarify legal standing, but no public resolution has emerged.

If classified as an unlicensed stablecoin or a yield-bearing security, Ethena could face enforcement actions in the U.S.—a jurisdiction that heavily influences global crypto policy. Without regulatory clarity, the project’s global scalability and institutional adoption may be severely limited.

Echoes of LUNA

ENA’s model is drawing inevitable comparisons to Terra’s LUNA-UST system. While structurally different—UST relied on algorithmic mint-burn dynamics, USDe uses derivative hedging—the incentive structure is strikingly similar: high yields in exchange for confidence in a pegged asset.

Analysts point out that USDe’s reliance on leveraged perp markets exposes the system to crowding risk. If too many participants pursue the same carry trade, funding rates compress and yields vanish—undermining the very mechanism USDe depends on.

Already, sUSDe staking yields have plunged from over 60% to under 5% in just six months, data from Ethena’s dashboard shows. The capital buffer, reportedly at 1.18%, provides little cushion in the event of market turbulence.

Short-Term Price Action vs. Structural Risk

Following the Upbit listing, ENA’s market cap temporarily spiked as Korean retail traders rushed in. Yet insiders remain cautious. Arthur Hayes, former BitMEX CEO and early advisor to Ethena, is said to have sold a sizable portion of his ENA allocation in December for a reported $7.7 million. Since its March high, ENA has lost more than 80% of its value.

The Korean listing comes at a time when Ethena’s momentum is slowing. On-chain activity has plateaued, and sUSDe’s TVL has begun to decline. The price surge may reflect opportunistic inflows rather than fundamental demand.

A local blockchain security researcher told Tokenpost, “It’s a technically ambitious project, but its real-world survivability is questionable. With funding rates declining and regulators circling, the upside is capped while downside risks grow.”

Legal Limbo and Institutional Aversion

Without U.S. compliance, Ethena’s model may remain relegated to offshore venues and retail-focused platforms. Institutional platforms are unlikely to onboard USDe due to potential exposure to enforcement action. This puts the project in a precarious position—popular enough to attract scrutiny, but not compliant enough to be legitimized.

Korea’s major exchanges may see ENA as a source of trading volume, but if U.S. regulators issue warnings or sanctions, domestic scrutiny could follow. Korean investors are already familiar with the consequences of unregulated crypto experiments.

A High-Wire Act

Ethena is a bold experiment, blending advanced derivatives strategy with the ambitions of a decentralized stablecoin. But the model’s survival depends on three volatile variables: a persistently favorable market structure, legal tolerance, and investor trust.

All three are fragile. Perp markets are cyclical. Legal clarity remains elusive. And investor trust is fleeting—especially when memories of Terra’s collapse are still fresh.

ENA may not be the next LUNA. But unless Ethena evolves from an exciting yield engine into a legally sound and economically sustainable platform, the similarities may become more than symbolic.

Comment 0