News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

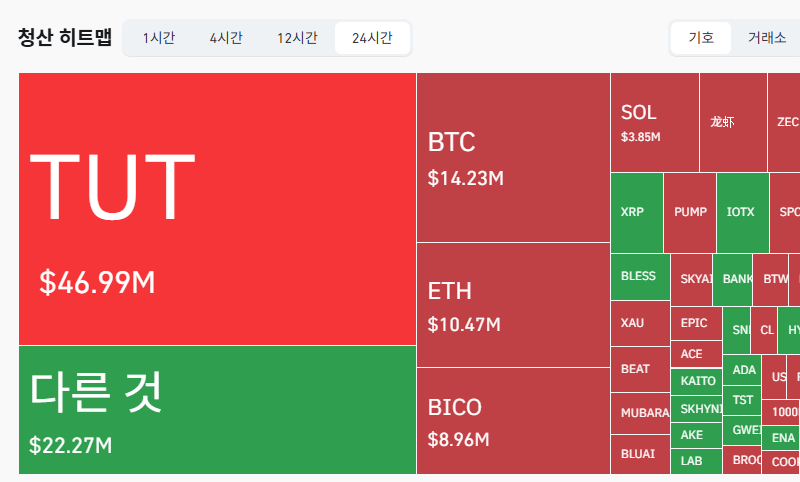

South Korea’s cryptocurrency market saw a wave of new token listings in the first half of 2025, widening investor choice — but also exposing the market’s persistent volatility and regulatory fragility.

According to new data from the Financial Intelligence Unit (FIU) and the Financial Supervisory Service (FSS), the number of cryptocurrencies available for trading on Korean exchanges rose to 1,538 as of June, up 13% from 1,357 at the end of last year. That expansion came even as delistings, risk warnings, and project failures accelerated.

More Coins, But Investors Stick to Majors

The increase in listed tokens was driven largely by Korea’s won-denominated exchanges, which added an average of 36 new assets per platform, bringing their average coverage to 260. Coin-to-coin markets remained flat, offering about 20 assets on average.

Excluding duplicate listings across multiple exchanges, there were 653 unique assets traded domestically — a 9% rise from six months earlier. Yet, despite the proliferation of tokens, investor attention remained heavily concentrated in global blue chips.

Of the top 10 cryptocurrencies by domestic market capitalization, six — Bitcoin, Ethereum, XRP, Solana, Dogecoin, and Cardano — overlapped with the global top 10. Together, these major assets accounted for 78% of Korea’s total crypto market capitalization, underscoring how both institutional and retail investors continue to cluster around large-cap tokens.

Homegrown Coins Shrink as Single Listings Decline

The number of tokens listed exclusively on a single domestic exchange fell slightly to 279, down from 287 at the end of 2024. Among these, 86 were locally issued Korean projects — an 11% decline.

The market capitalization of single-listed tokens dropped 33% to ₩1.3 trillion ($940 million), just 1% of the total domestic crypto market.

Within that, homegrown single-listing projects made up ₩780 billion — up 9% from the previous half, but still a negligible fraction of total market value.

In coin-to-coin markets, single-listed tokens continued to dominate, representing 96% of total capitalization at ₩470 billion — a 14% rise. Eight of the top 10 assets traded in those non-fiat markets were single listings.

Yet almost half of all single-listed tokens — 43% or 121 projects — had market caps under ₩100 million ($70,000), reflecting extremely low liquidity and high volatility. Regulators warned that such small-cap projects pose elevated risks to market stability and investor protection.

Listings Surge 83%, Delistings Nearly Double

The report showed an 83% jump in new listings, reaching 232 during the first half of 2025. Won-based markets accounted for most of the activity with 207 new listings (+80%), while coin-to-coin markets saw 25 (+108%).

However, delistings also surged. A total of 58 tokens were removed from trading — an 87% increase from the previous half.

Most were attributed to project-level failures (80%), including unsustainable business models, poor token management, or foundation-related risks. Other causes included investor protection concerns (2%) and technical issues (2%).

Of the 47 unique assets delisted during the period, two-thirds (31 tokens) were single-listed projects — underscoring the vulnerability of tokens that lack global exposure or multi-exchange support.

The number of “watchlist” tokens flagged for potential problems also climbed to 72, up 11% from late 2024, suggesting persistent structural risks in Korea’s altcoin ecosystem.

A Maturing But Risk-Prone Market

The findings come from the FIU and FSS’s semiannual survey of 25 domestic virtual asset businesses, including 17 exchanges and 8 custodians, covering the period from January to June 2025.

While the data point to a broadening of crypto assets available to Korean investors, they also highlight the market’s bifurcation — between a few global blue chips commanding the bulk of capital and a long tail of speculative, thinly traded coins.

That contrast underscores a paradox of Korea’s crypto industry: one of the most active retail markets in the world, yet still dominated by speculative microcaps and regulatory uncertainty.

Comment 0