News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

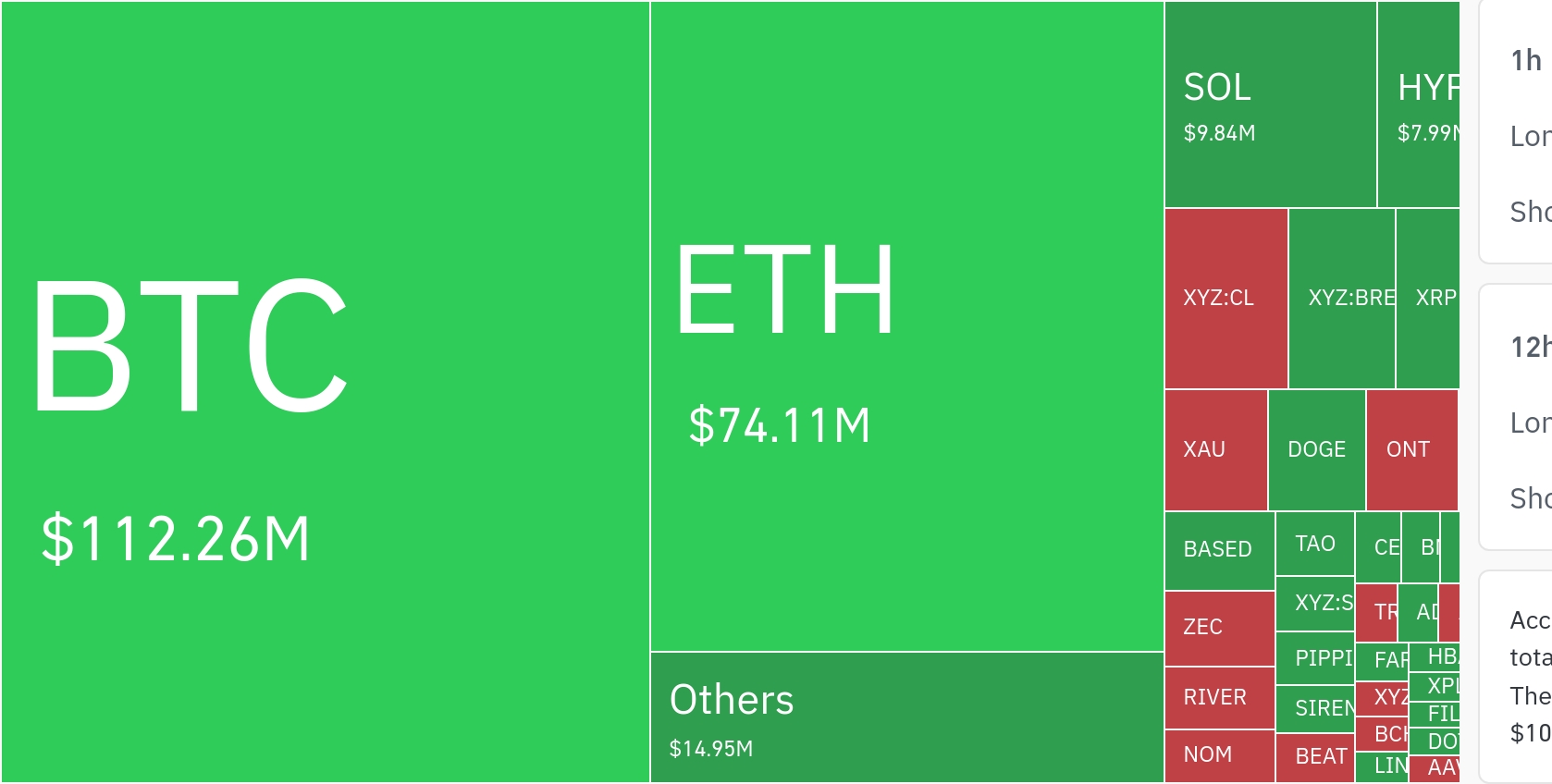

Ethereum (ETH) and Solana (SOL) are increasingly being compared through a single, headline-friendly metric: fees. But the latest data suggests the rivalry has moved beyond “who earned more” and into a more consequential question—where value is being created, and who ultimately captures it.

As of April 2, 2026 UTC, Ethereum generated $4.75 million in 24-hour fees, down 2.94% from the prior day, while Solana posted $6.67 million, up 24.87% over the same period. On a daily snapshot, Solana is clearly ahead. Over longer windows, however, Ethereum remains in front: $317.49 million in fees over 30 days versus Solana’s $186.02 million, preserving roughly a 1.7x gap. The divergence points less to a simple demand difference than to a structural split in how each network monetizes activity.

Ethereum’s shift: fee revenue is being ‘externalized’ into a broader stack

The most important change in Ethereum’s fee dynamics has accelerated since the Dencun upgrade, which reinforced Ethereum’s migration toward a Layer 2-centric economy. Network usage metrics remain elevated—daily active addresses are reported around 2 million, with smart contract calls near 40 million—yet base-layer fees have not risen in tandem. The implication is not that revenue “disappeared,” but that it has been redistributed across a wider economic perimeter.

In practical terms, value capture is increasingly fragmented across three layers:

- Base layer (L1): positioned for higher-value settlement such as bridging, large DeFi flows, and institutional transactions.

- Layer 2s: optimized for high-volume, low-cost execution, where revenues concentrate in sequencers rather than on L1 gas.

- MEV supply chain: block-building and transaction ordering that can monetize activity in ways that do not always show up as simple “fees.”

This has created what some analysts describe as Ethereum’s ‘invisible revenue’ expansion: economic activity that is real and monetizable, but not fully reflected by L1 fee totals alone. The growth of stablecoin settlement and real-world asset tokenization has been central to this narrative. With stablecoin liquidity estimated at $1.62 trillion and tokenized Treasury-style instruments and corporate cash management increasingly moving on-chain, Ethereum’s role looks less like a consumer app platform and more like a financial settlement backbone—where per-transaction charges can be low even as the underlying value being settled grows sharply.

Solana’s model: speed-first, on-chain monetization with direct attribution

Solana, by contrast, keeps activity and monetization largely on its L1. Transactions are processed directly on the base chain, and fees flow to validators in a more transparent, easily measured loop. The latest 24-hour fee surge is widely interpreted as a response to short-term trading intensity—often linked to heightened activity in derivatives, memecoins, and high-frequency DeFi strategies that benefit from Solana’s throughput and latency profile.

Recent aggregates illustrate the split:

- 24-hour fees: Ethereum $4.75M (-2.94%) vs. Solana $6.67M (+24.87%)

- 7-day fees: Ethereum $55.07M vs. Solana $35.93M

- 30-day fees: Ethereum $317.49M vs. Solana $186.02M

From an economic lens, Solana is optimized for high ‘velocity’ revenue—capturing monetization from rapid, frequent transactions—while Ethereum increasingly captures higher ‘margin’ settlement flows across a layered ecosystem.

The capital-flow variable: stablecoin issuers and tokenized assets

One of the most closely watched drivers this quarter has been Circle (CRCL) and the broader expansion of stablecoin-based payments and tokenized real-world assets. Market participants argue that the infrastructure built around USDC settlement and tokenized government debt has strengthened Ethereum’s case as a de facto ‘global settlement layer.’

Critically, that shift does not necessarily translate into higher headline fee totals. Instead, it can produce second-order effects: larger gross settlement volumes despite lower unit fees, increased bridge and institutional routing activity, and higher MEV and settlement-related monetization—while execution migrates to Layer 2s where fees accrue elsewhere. In this framework, declining or stagnant L1 fees do not automatically imply declining network relevance; they can also signal that larger pools of capital are moving more efficiently through the stack.

Flash spike or structural rotation?

The short-term picture favors Solana, with a clear daily revenue lead. But the 7-day and 30-day totals still point to Ethereum’s persistence as the dominant fee generator in aggregate terms—and, more importantly, to its growing role in longer-duration capital settlement. The roughly $131 million 30-day gap is being read by some analysts as evidence that institutional-style flows are still concentrating more heavily around Ethereum’s ecosystem, even as execution-heavy segments of crypto trading periodically surge on Solana.

Ultimately, the fee race has become harder to adjudicate with a single scoreboard. Solana is positioning itself as the winner in ‘speed’ and high-frequency monetization, while Ethereum is building a case as the winner in ‘value settlement’ across a modular stack. The key question for the market is no longer just who earns more fees on a given day, but who is moving—and retaining—larger pools of capital over time.

Comment 0