News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

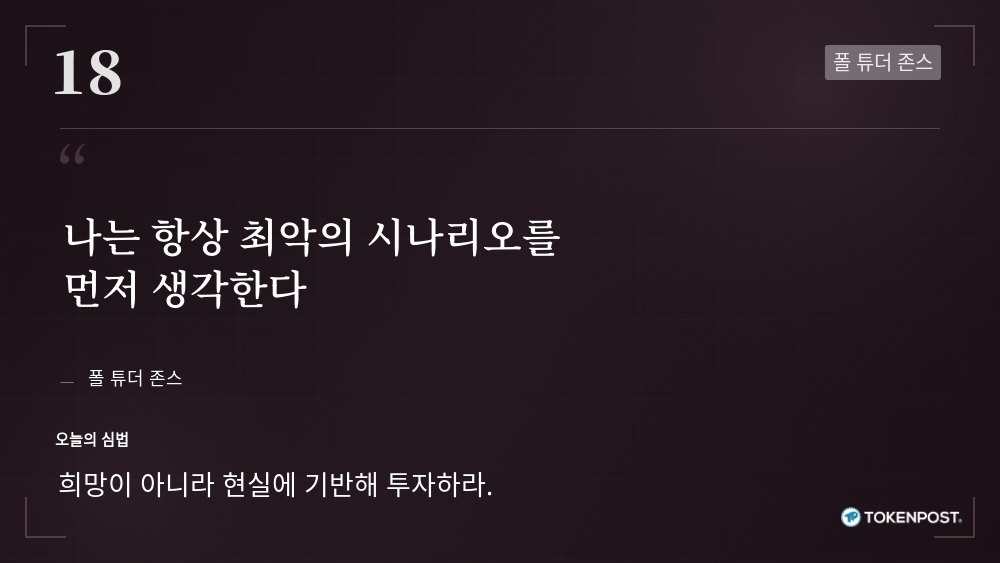

Macro trading veteran Paul Tudor Jones is again being cited in crypto circles for a simple but often ignored principle: start with the worst-case scenario, not the dream outcome. The reminder lands as digital-asset markets remain prone to sharp, liquidity-driven swings that can punish overconfident positioning.

The quote—“I always think about the worst scenario first”—has resurfaced in a Korean-language investor education series this week, framed as a psychological guardrail rather than a trading signal. The message is aimed at helping participants build a steadier decision-making process in high-volatility markets, where narratives of “it could go 10x” frequently become the emotional trigger for hitting the buy button.

Jones’ approach flips that impulse. Before entering a position, he is known for imagining the most damaging plausible outcome and asking whether he can withstand it—financially and psychologically. In practical terms, the framework encourages sizing a trade so that even a near-total loss would not destabilize one’s broader financial life. Put bluntly: only allocate an amount that still allows for a calm answer to the question, “What happens if this goes to zero?”

That risk-first mindset is a recurring theme in Jones’ career. Born in 1954, he rose to global prominence for his macro trading and is widely associated with anticipating the 1987 “Black Monday” crash and profiting from aggressive bearish positioning. As the founder of Tudor Investment Corporation, he built a reputation for pairing technical analysis with global macro views—while consistently prioritizing preservation of capital. Market participants often summarize his philosophy as ‘risk management before returns,’ emphasizing quick loss-cutting and preparation for adverse scenarios as non-negotiable habits.

The renewed attention to Jones’ cautionary framing also reflects a broader shift in crypto market culture, where institutional participation has increased but retail behavior can still be driven by momentum and social-media narratives. In that environment, disciplined position sizing and scenario analysis become less about sophistication and more about survival—especially when leverage, thin liquidity, or sudden policy headlines amplify moves.

Jones has in recent years also pointed to Bitcoin (BTC) as a potential inflation hedge, a view that helped legitimize the asset for some macro-focused investors. Even so, the central lesson highlighted by the series is not about any single asset, but about process: investing based on reality rather than hope, and ensuring that the downside—however uncomfortable—has been fully priced into the decision before the trade is even placed.

🔎 Market Interpretation

- Risk-first framing is resurfacing as a counterweight to crypto “10x” narratives: The article highlights Paul Tudor Jones’ habit of starting with the worst-case scenario, a particularly relevant mindset in markets known for sudden, liquidity-driven spikes and drawdowns.

- Crypto volatility makes psychology a core market variable: The quote is presented not as a signal to buy/sell but as a behavioral guardrail meant to reduce impulsive entries driven by FOMO and social momentum.

- Institutional growth hasn’t eliminated retail-style reflexes: Even with more institutional participation, leverage, thin liquidity, and headline risk can still produce abrupt moves that punish oversized or poorly planned positions.

- The key takeaway is process over prediction: Rather than focusing on Bitcoin as an inflation hedge, the emphasis is on building a repeatable decision process that “prices in” downside before entering a trade.

💡 Strategic Points

- Start every trade with a “go to zero” test: Ask, “If this position goes to zero (or drops 50–80%), what happens to my finances and my ability to think clearly?” If the answer is distress, the position is too large.

- Position size is the primary risk control in high-volatility assets: The framework encourages allocating only an amount that won’t destabilize one’s broader financial life—even under severe loss scenarios.

- Separate excitement from execution: Treat upside stories (e.g., “it can 10x”) as hypotheses, while making entry decisions based on defined downside, invalidation points, and survivability.

- Plan for liquidity and headline shocks: Assume spreads widen and exits get harder during stress; size and structure trades so forced selling (or liquidation) is unlikely.

- Make loss-cutting non-negotiable: The article reinforces Jones’ reputation for capital preservation—cutting losses quickly and preparing for adverse scenarios as core habits, not optional tactics.

- Use scenario analysis before conviction: Map at least three paths (base, bullish, bearish) and decide in advance what actions you will take in each, rather than improvising under pressure.

📘 Glossary

- Worst-case scenario analysis: A planning method that begins by identifying the most damaging plausible outcome and designing the position so it remains survivable.

- Position sizing: Determining how large a trade should be relative to total capital to control risk and avoid catastrophic losses.

- Liquidity-driven swing: A sharp price move caused by thin order books, forced liquidations, or sudden shifts in available buyers/sellers rather than gradual fundamentals.

- Leverage: Borrowed exposure that magnifies gains and losses; in crypto it can trigger forced liquidation during rapid drawdowns.

- Scenario analysis: Evaluating multiple potential future outcomes (including adverse ones) to pre-commit risk limits and responses.

- Capital preservation: A risk management priority focused on avoiding large drawdowns so an investor can remain in the game long enough to capture future opportunities.

- Inflation hedge: An asset expected to hold value when purchasing power declines; Bitcoin is sometimes framed this way, though outcomes can vary by regime.

Comment 0