News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Corporate crypto treasuries are entering a new phase: simply holding Bitcoin (BTC) is no longer enough to justify premium valuations. As 2026 unfolds, investors are increasingly rewarding companies that can turn digital assets into repeatable cash flows—shifting the conversation from balance-sheet accumulation to 'earnings power' and capital efficiency.

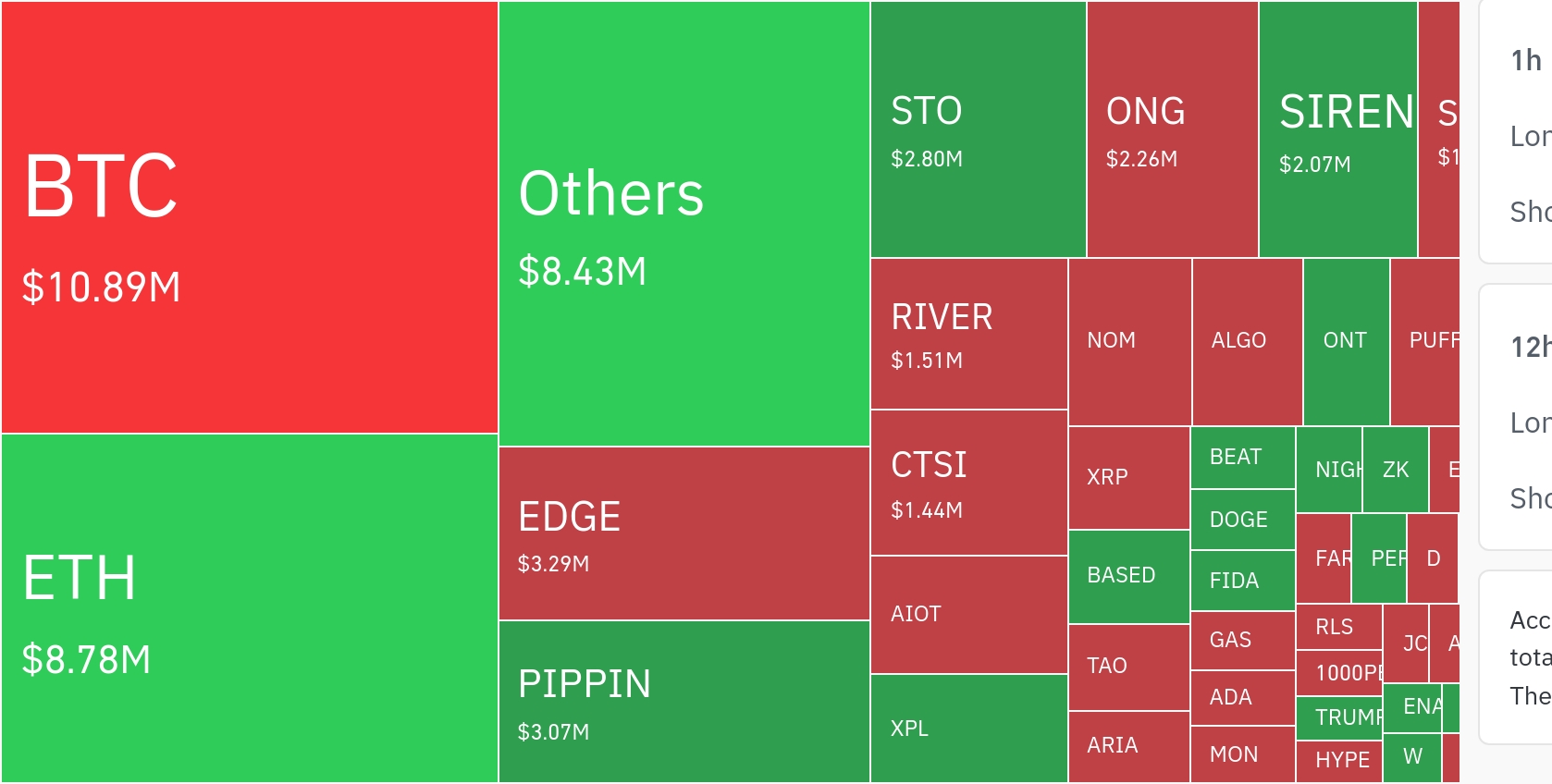

The change comes after a rapid expansion in corporate participation. By October 2025, more than 200 listed companies held digital assets, with aggregate holdings valued at roughly $115 billion. In September 2025, the combined market capitalization of these firms climbed to about $150 billion—nearly quadrupling year over year. Yet recent price action has revealed a new skepticism: some companies now trade below the value of their on-chain holdings, a clear signal that the market is applying a discount to passive exposure and demanding a credible path to monetization.

In response, corporates are adopting equity-friendly metrics and policies—such as buybacks and 'BTC per share' disclosures—aimed at demonstrating discipline and shareholder alignment. More broadly, a 'DAT 2.0' playbook is emerging, referring to digital-asset treasury strategies designed not just to store value but to actively generate yield and operating profit through on-chain and market-structure tools.

Staking and infrastructure participation

The most 'protocol-aligned' approach centers on staking—contributing assets to network security and operations in exchange for rewards—an area dominated by Ethereum (ETH)-based strategies. Bitmine Immersion Technologies, for example, has staked more than 3 million ETH as of early 2026, managing roughly $9.9 billion in assets and generating an estimated $172 million in annual staking income. The firm has also emphasized its own validator infrastructure as a way to outperform average network yields, underscoring how operational execution is becoming a differentiator, not just asset size.

Another variation is restaking, which reuses staked assets to secure additional services—often pitched as infrastructure for AI, identity, and other middleware—seeking incremental yield at the cost of added complexity and risk. SharpLink Gaming has deployed approximately $200 million worth of ETH into restaking infrastructure, illustrating how some corporates are moving beyond basic staking into layered yield strategies.

Trading-driven treasury income

A second route relies on derivatives and market microstructure—capturing options premium, running basis trades between spot and futures, and harvesting funding-rate spreads. One Japan-listed company holding more than 35,000 BTC reportedly generated around $55 million through options strategies, helping lift operating profit by more than 1,600% from the prior year.

However, the example also highlights a growing tension in crypto-treasury accounting: despite strong cash-generation, mark-to-market valuation swings can produce headline losses and push net income into the red. For global investors, the widening gap between operating cash flow and reported earnings complicates valuation and raises questions about how sustainable—and how hedgeable—these strategies are across cycles.

Galaxy Digital has pursued a more diversified model, combining asset management, collateralized lending, advisory services, and infrastructure businesses. The firm posted more than $730 million in adjusted gross profit in the third quarter of 2025, according to the report, with a notable shift toward converting mining facilities into AI data centers. That repositioning reflects a broader theme: companies are looking to reduce reliance on single-source crypto beta by building multi-stream revenue across digital assets and adjacent compute demand.

Credit strategies and interest-rate arbitrage

A third model resembles traditional banking: borrowing against digital assets and deploying proceeds into higher-yield credit markets. In practice, companies can use BTC as collateral to raise stablecoin liquidity, then allocate that capital into private credit strategies to earn interest spreads. Done well, the structure can layer potential BTC upside on top of interest income—while requiring rigorous liquidity management, credit underwriting, and leverage controls to avoid forced liquidations during drawdowns.

Supporters of the approach point to stablecoins’ accelerating role in real-economy settlement. By 2026, stablecoins have increasingly been framed as core infrastructure for B2B payments and near-instant settlement, with projections in the report suggesting the market could reach $1.2 trillion by 2028. If that trajectory holds, it could expand the pool of liquidity and counterparties needed for credit-style treasury strategies to scale.

A new valuation yardstick

The overarching takeaway is that the market’s corporate-crypto scorecard is changing. The key question is no longer who holds the most Bitcoin, but who can operate it most 'disciplined'—producing durable yield, managing volatility, and translating digital assets into consistent financial performance.

Different approaches—staking, derivatives, and credit—are likely to coexist. But the direction is consistent: passive accumulation is losing persuasive power, while hybrid models that combine multiple revenue engines are emerging as the clearest route to sustaining investor confidence in the next stage of corporate crypto adoption.

🔎 Market Interpretation

- Valuation regime shift: Public markets are moving from rewarding asset accumulation (simply holding BTC) to rewarding earnings power—repeatable cash flows, capital efficiency, and risk controls tied to digital-asset holdings.

- Passive exposure is being discounted: Some listed treasuries now trade below the on-chain value of their holdings, signaling investors view “buy-and-hold” crypto balance sheets as insufficient without a monetization plan.

- Corporate participation has scaled fast, scrutiny is rising: By Oct 2025, 200+ listed companies held ~$115B in digital assets; combined market caps reached ~$150B by Sep 2025. The next phase is proving conversion of crypto holdings into sustainable operating performance.

- DAT 2.0 emerges: A new playbook frames crypto treasuries as operating strategies (yield + services + infrastructure) rather than static stores of value.

💡 Strategic Points

- Investor-facing discipline tools: Companies are adopting buybacks and “BTC per share” disclosures to communicate capital allocation discipline and alignment with shareholders—attempting to justify premiums (or avoid discounts).

- Staking as protocol-aligned income: ETH staking/validator operations are highlighted as a relatively direct way to turn assets into yield. Execution matters (validator uptime, fee capture, infra efficiency), not just scale (e.g., large ETH staking programs targeting material annual income).

- Restaking raises yield—and complexity: Reusing staked assets to secure additional services can enhance return potential, but introduces additional layers of technical, smart-contract, and slashing/operational risk.

- Derivatives as a treasury “income desk”: Options premium, basis trades, and funding-rate strategies can generate sizable operating cash flow; however, outcomes are path-dependent and require strong risk management.

- Accounting and optics risk: Even when strategies generate real cash, mark-to-market swings can create reported losses, widening the gap between operating cash flow and net income—complicating valuation and making “earnings quality” a key debate.

- Hybrid business models reduce crypto beta: Diversification into asset management, lending, advisory, and infrastructure (including repurposing mining into AI data centers) can stabilize revenue and reduce reliance on directional crypto price moves.

- Credit + collateral model (bank-like): Borrowing against BTC (often via stablecoins) and deploying into higher-yield credit markets can add interest spreads while maintaining BTC upside exposure—but raises liquidation, leverage, and counterparty risks during drawdowns.

- Stablecoins as scaling rail: If stablecoins expand as B2B settlement infrastructure (projection: potentially $1.2T by 2028), liquidity and counterparties for credit-style treasury strategies could deepen, enabling broader institutional adoption.

- New yardstick for “best” treasury: The market is increasingly asking: Who can run a disciplined, hedgeable, and durable multi-engine model (staking + trading + credit) versus simply holding the most BTC?

📘 Glossary

- Corporate crypto treasury: A company strategy that holds and manages digital assets (e.g., BTC/ETH) as part of reserves, capital allocation, or operating strategy.

- Premium/Discount to NAV: When a company’s market value trades above/below the estimated net asset value of its crypto holdings (and other assets), reflecting investor expectations for profitability, risk, and governance.

- BTC per share: A disclosure metric expressing Bitcoin holdings relative to shares outstanding, used to signal per-share exposure and capital discipline.

- DAT 2.0: “Digital Asset Treasury 2.0” — an approach that aims to generate recurring yield/operating profit from treasury assets rather than only storing value.

- Staking: Locking or delegating tokens (commonly ETH) to help secure a network and earn rewards; returns depend on protocol rules and operational performance.

- Validator: Infrastructure/software that participates in block production/verification in proof-of-stake networks; operational excellence can impact realized staking yield.

- Restaking: Using staked assets (or their representations) to secure additional services beyond the base blockchain, aiming for extra rewards while adding risk.

- Derivatives strategies: Trading approaches using futures/options to earn yield (premium), capture spreads (basis), or harvest funding-rate differences—often sensitive to volatility and liquidity.

- Basis trade: Profiting from the price difference between spot and futures markets, typically via hedged positions; returns depend on the spread and funding/carry conditions.

- Funding rate: Periodic payments between long/short positions in perpetual futures; can be harvested when imbalances persist but may reverse quickly.

- Mark-to-market (MTM): Accounting method that revalues assets to current market prices, which can create reported earnings volatility even if cash flow is positive.

- Collateralized borrowing: Raising liquidity by pledging crypto (e.g., BTC) as collateral; can trigger liquidation if collateral value falls below required thresholds.

- Stablecoin: A token pegged to fiat (often USD) used for settlement and liquidity; central to many trading and credit flows in crypto markets.

Comment 0