News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

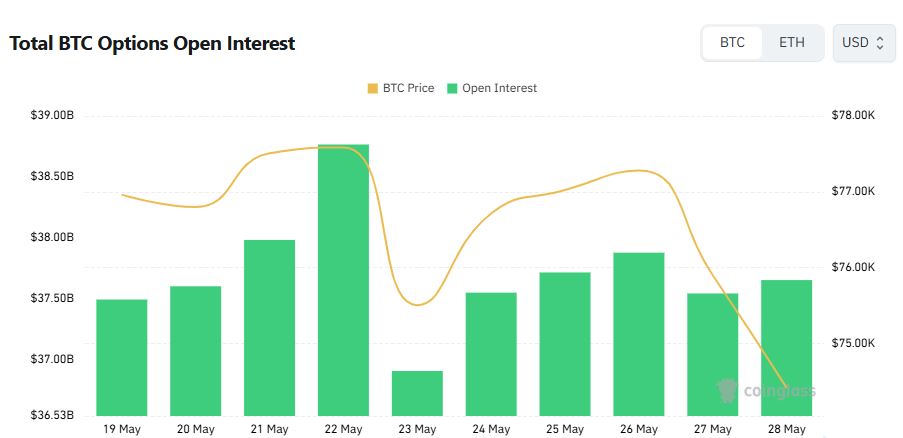

Bitcoin (BTC) options positioning held broadly steady on Wednesday, but short-term flow tilted defensively as traders concentrated activity in put contracts around the $70,000 strike—an indication that hedging demand remains elevated even as broader positioning still leans bullish.

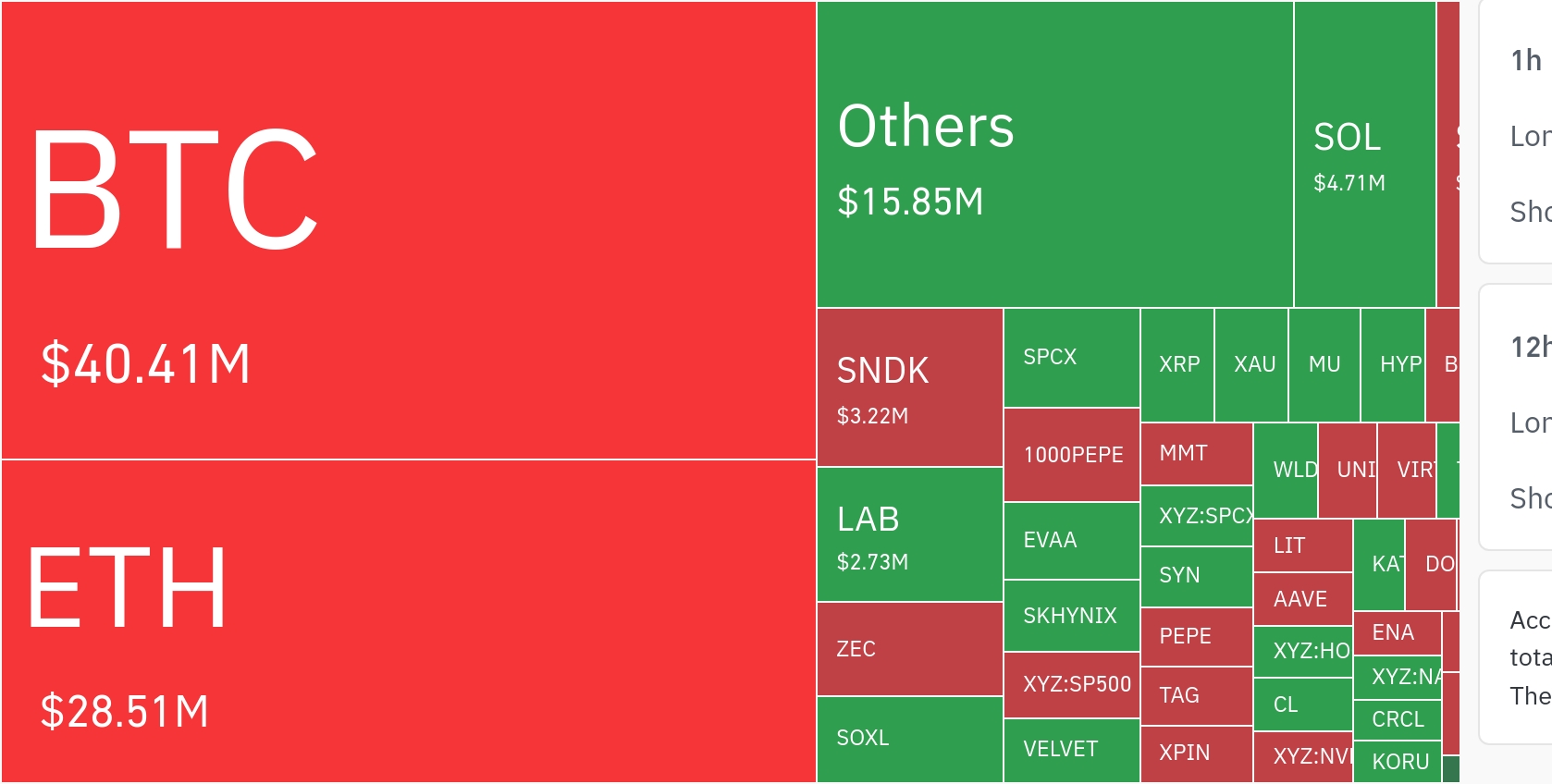

As of 12:00 a.m. ET on May 28, data compiled by Coinglass showed total Bitcoin options 'open interest' (OI)—the notional value of outstanding contracts—at about $37.565 billion, up roughly 0.1% from the prior day’s $37.54 billion. Calls accounted for 57% of open interest versus 43% for puts, suggesting the market’s accumulated exposure continues to favor upside scenarios.

Trading activity, however, pointed in a different direction. Aggregate options volume was approximately $3.663 billion over the last 24 hours, with puts narrowly leading at 50.36% compared with 49.64% for calls. Deribit remained the dominant venue with about $1.76 billion in volume, followed by Bybit at $845 million, Binance at $580 million, OKX at $441 million, and CME at roughly $47 million.

In terms of positioning, the largest concentrations of open interest were seen in the $80,000 call expiring May 29 on Deribit, the $120,000 call expiring Dec. 25 on Deribit, and the $60,000 put expiring Dec. 25 on Deribit. The mix highlights a market holding both optimistic longer-dated upside exposure and sizable downside protection into year-end.

By contrast, the top contracts by 24-hour volume were led by the $70,000 put expiring June 26 on Deribit, followed by the $55,000 put expiring Sept. 25 and the $80,000 call expiring June 26. The prominence of near-dated puts alongside an actively traded upside call reflects a two-track approach: traders appear to be paying for short-term protection while keeping optionality for a rebound or volatility-driven upside move.

Options are derivatives that allow investors to express leveraged views on price direction or hedge existing exposures. A 'call option' confers the right to buy at a preset price by a specified date, while a 'put option' provides the right to sell—often used to protect against declines. Because open interest captures the stock of outstanding positions while volume reflects fresh turnover, a steady OI base with put-heavy short-term activity can signal that longer-term bullish structures remain in place, even as participants brace for potential near-term drawdowns or choppier price action.

🔎 Market Interpretation

- Positioning steady, but hedging rises: Total BTC options open interest held near $37.565B (+0.1% day/day), indicating no major unwind or re-leveraging. However, 24h flow leaned defensive as put volume slightly exceeded call volume.

- Structural bias still bullish: Calls remain the majority of outstanding exposure (57% calls vs 43% puts), implying the broader market is still positioned for upside scenarios.

- Short-term fear vs long-term optimism: The most-traded contract was the $70,000 put (Jun 26), signaling concentrated near-term downside hedging. Meanwhile, large longer-dated call OI (e.g., $120,000 call (Dec 25)) suggests investors continue to carry bullish year-end optionality.

- Two-track behavior: Traders appear to be buying near-term protection while keeping upside exposure via actively traded calls (e.g., $80,000 call (Jun 26)), consistent with expectations of higher volatility or choppy price action rather than a single-direction conviction.

- Venue concentration: Liquidity and price discovery remain centered on Deribit (largest volume), with meaningful activity across Bybit, Binance, OKX, and a relatively small share on CME—suggesting predominantly crypto-native participation.

💡 Strategic Points

- Hedging signal at a key strike: Heavy interest in the $70k put implies traders are actively insuring against a drawdown toward/through that level; this strike can act as a psychological and positioning “magnet” into the June expiry.

- Watch OI vs volume divergence: With OI stable but put volume leading, the market message is: core positioning hasn’t flipped bearish, yet participants are adding incremental protection (often consistent with uncertainty, event risk, or volatility repricing).

- Risk reversal mindset: The combination of large upside call OI (e.g., $80k May 29, $120k Dec 25) plus sizable downside put OI (e.g., $60k Dec 25) resembles a market that expects wide price distribution—not just a gentle trend.

- Expiry-driven sensitivity: Concentrated positions in near-dated May/June contracts can amplify spot sensitivity via hedging flows as expiry approaches, potentially increasing short-term volatility around key strikes.

- Practical takeaway for traders: If replicating this stance, the implied approach is retain upside exposure (calls or call spreads) while buying short-dated puts (or put spreads) to manage near-term downside—recognizing that protection costs rise when demand for puts increases.

📘 Glossary

- Options: Derivatives granting the right (not obligation) to buy/sell an asset at a preset price by a certain date.

- Call option: Right to buy at the strike price by expiration; typically benefits from price rises.

- Put option: Right to sell at the strike price by expiration; commonly used for downside protection.

- Strike price (e.g., $70,000): The preset price at which the option can be exercised.

- Expiration: The date the option contract ends (e.g., May 29, Jun 26, Dec 25).

- Open Interest (OI): Total notional value/number of outstanding option positions; reflects the existing stock of exposure.

- Volume: Amount traded over a period (here, 24h); reflects new turnover/flow and short-term sentiment.

- Notional value: The face value used to represent the size of a derivatives position, typically linked to the underlying asset price.

- Hedging: Taking positions (often puts) to reduce risk from adverse price moves in an existing exposure (e.g., spot BTC holdings).

Comment 0