News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

The stablecoin business is entering a new phase as the long-standing model of issuers capturing most of the yield on customer-backed reserves comes under growing pressure—from crypto-native challengers to global payment giants—and is beginning to ripple through public markets.

At the center of the debate is a simple question that has increasingly shifted from technical trust to economic fairness: if stablecoins function as a kind of ‘digital dollar’ built on user deposits, who should benefit from the interest generated when those dollars are invested in short-term U.S. Treasuries and other cash-like instruments?

For years, the dominant stablecoin model has been straightforward. Users deposit $1, and an issuer mints a token intended to hold a $1 peg on-chain. The issuer does not store the cash in a vault. Instead, it typically allocates reserves to Treasury bills and highly liquid instruments, collecting the yield as interest rates rise. That spread—generated by customers’ deposited funds—has been the industry’s core profit engine. Tether, and later Circle ($CRCL) with USD Coin (USDC), became emblematic of how lucrative this structure could be in a higher-rate environment.

In effect, stablecoin issuers built a lightweight alternative to banks: they accumulated large pools of dollar-like liabilities, moved value faster than card rails, and monetized reserves without the same balance-sheet complexity as traditional institutions. The higher the policy rate, the stronger the economics. In a market starved for durable revenue, this ‘interest machine’ looked unusually scalable.

That profitability, however, is precisely what is attracting competitors—and triggering a re-pricing of incumbents. Crypto markets first responded with experimentation: decentralized alternatives argued that users should not have to rely on a single company’s credibility, while “yield-sharing” designs questioned why issuers alone should capture reserve income. Now, the competitive set is broadening further as some of the world’s largest financial and technology firms explore stablecoin infrastructure and settlement networks.

Companies such as Visa ($V), Mastercard ($MA), BlackRock ($BLK), Stripe, and Google ($GOOGL) have recently signaled interest in stablecoins not merely as a blockchain novelty, but as a new economic layer where value moves—and where value sits. In payments, that distinction matters: transaction flows create fees, while stored balances create yield and data. Stablecoins can potentially generate both.

One project often referenced in this context is OpenUSD (OUSD), which promotes a structure designed to reduce issuance and redemption friction and limit ‘interest monopoly’ dynamics by distributing economic benefit more broadly rather than concentrating it at a single issuer. Whether OUSD becomes a dominant product is less important than what it represents: a credible challenge to the assumption that reserve yield naturally belongs to the stablecoin company.

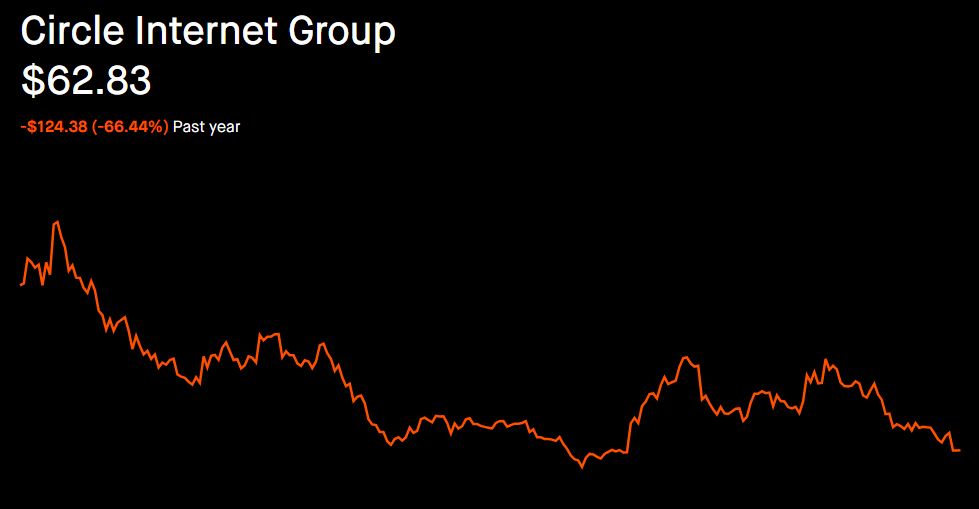

Markets appear to be taking the shift seriously. Circle ($CRCL) shares fell sharply after attention coalesced around models that could compress issuer economics, drawing investor focus to how much of Circle’s profitability depends on capturing yield. The move looked, on the surface, like a company-specific selloff. But the underlying message was broader: investors are reassessing the durability of the issuer-centric stablecoin business model as competition intensifies and product design evolves.

Critically, the implications extend beyond crypto firms. If stablecoins become common payment instruments—whether for cross-border transfers, exchange settlement, or consumer purchases—they could weaken two of banks’ most reliable profit centers: deposit economics and card-related fee income. Stablecoins can move value outside the traditional loop of bank accounts and card issuance, reducing the number of toll gates through which payments must pass.

That does not mean card networks are simply “attacking” banks. Historically, Visa ($V) and Mastercard ($MA) have operated as partners to issuing banks, powering rails that banks rely on for consumer payments. But as the route money takes changes, incentives shift. For card networks, the strategic imperative is not the form of the dollar but the pathway the dollar travels. If dollars move via cards, they need to sit atop card rails; if dollars move via tokenized cash, they need to integrate with that ecosystem as well. Participation becomes a defensive posture against being bypassed by a new settlement layer.

Banks face a more complicated calculus. Embracing stablecoins that return more value to users—directly or indirectly—could challenge the traditional logic of taking deposits, deploying them, and retaining much of the upside. Even if regulators restrict explicit “interest-bearing stablecoins,” the market may still recreate similar outcomes through adjacent mechanisms. Platforms can offer benefits—points, discounts, cashback-like rewards—without labeling them as interest, mirroring the incentives that have long driven credit card adoption. The economic effect for users can be similar: the appeal is not yield as a financial product, but rewards as a consumption incentive.

In South Korea, the argument is not theoretical. Domestic banks have already experienced how customer relationships can migrate toward platforms. As Kakao Pay, Naver Pay, and Toss expanded, banks increasingly played a behind-the-scenes role in account rails and settlement while consumer attention—and valuable behavioral data—shifted to the front-end apps. Observers warn that won-denominated stablecoins could replicate this pattern: even if banks help provide stability and compliance, platforms may control the user interface, rewards, and data—capturing the highest-leverage parts of the value chain.

That is why the emerging debate around stablecoins is no longer just about who issues them. It is about who owns the customer relationship, who captures reserve-generated income, who governs the incentives that drive usage, and who controls the payment data generated by everyday transactions. Designs that prioritize bank-centered stability can reduce certain risks, but they may not prevent platforms from becoming the primary distribution channel—and the primary beneficiary—if they control the rewards and the user experience.

Ultimately, the industry’s defining shift is conceptual. The old question was whether a stablecoin could be trusted to hold its peg. The new question is who should receive the economic upside created by the system. Circle’s volatility is being read as a signal that the ‘issuer-keeps-the-interest’ era is being challenged. The larger implication is that the same question will increasingly confront banks and payment incumbents as stablecoins move from trading venues toward everyday settlement. The real battle is not about token prices—it is about reassigning ownership of yield and payment economics in a tokenized dollar world.

Comment 0