News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Options positioning in major altcoins diverged on Thursday, with Solana (SOL) showing a clear tilt toward upside bets while Ethereum (ETH) and XRP (XRP) reflected heavier near-term demand for downside protection—an important signal as traders gauge whether the broader market is entering a consolidation phase or setting up for a rebound.

Data from Deribit, the largest crypto options exchange, showed that as of 2:05 a.m. ET on June 5 (6:05 UTC), options open interest for contracts expiring the same day stood at 153,417 contracts for Ethereum (about $269.11 million), 12,069 contracts for Solana (about $8.25 million), and 5,175 contracts for XRP (about $5.97 million).

The open interest put/call ratio—a commonly watched gauge of whether traders are positioned more defensively ('puts') or more optimistically ('calls')—came in at 0.92 for Ethereum, 0.55 for Solana, and 1.16 for XRP. A ratio below 1 suggests call open interest exceeds puts, while a figure above 1 indicates the opposite.

Ethereum’s reading of 0.92 pointed to a slight call skew, implying modest upside expectations. However, the ratio’s proximity to parity also underscored a cautious stance, with substantial put positioning suggesting traders remain sensitive to drawdown risk around key support levels.

Solana, by contrast, posted the strongest call dominance of the three, with a put/call ratio of 0.55. The distribution suggested traders were leaning into a near-term recovery narrative, with positioning clustered around strikes that typically reflect expectations for a quick move higher rather than a slow grind.

XRP’s put/call ratio of 1.16 signaled comparatively more defensive positioning, indicating that market participants were more focused on hedging downside scenarios than on maximizing exposure to an immediate rally.

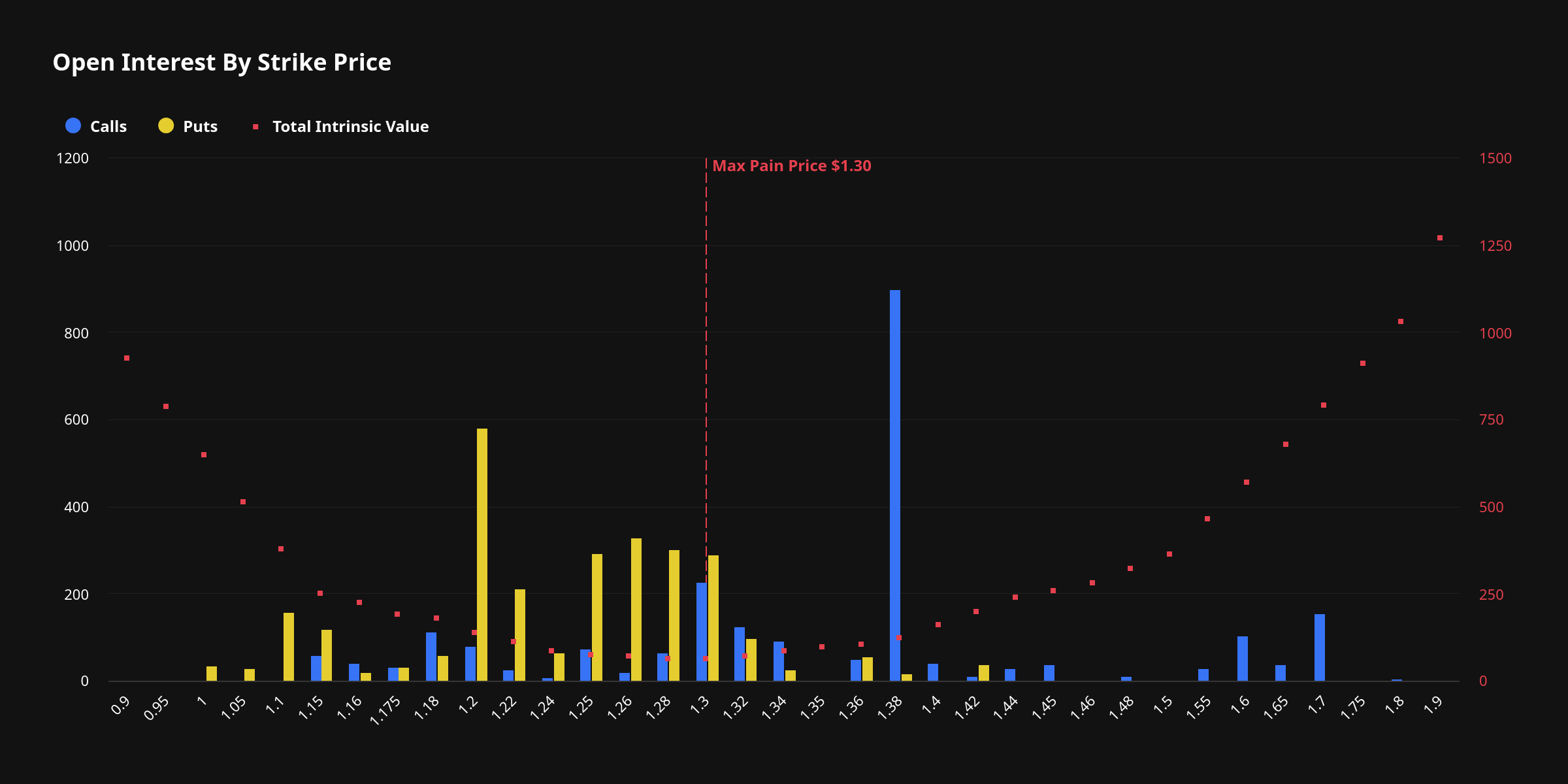

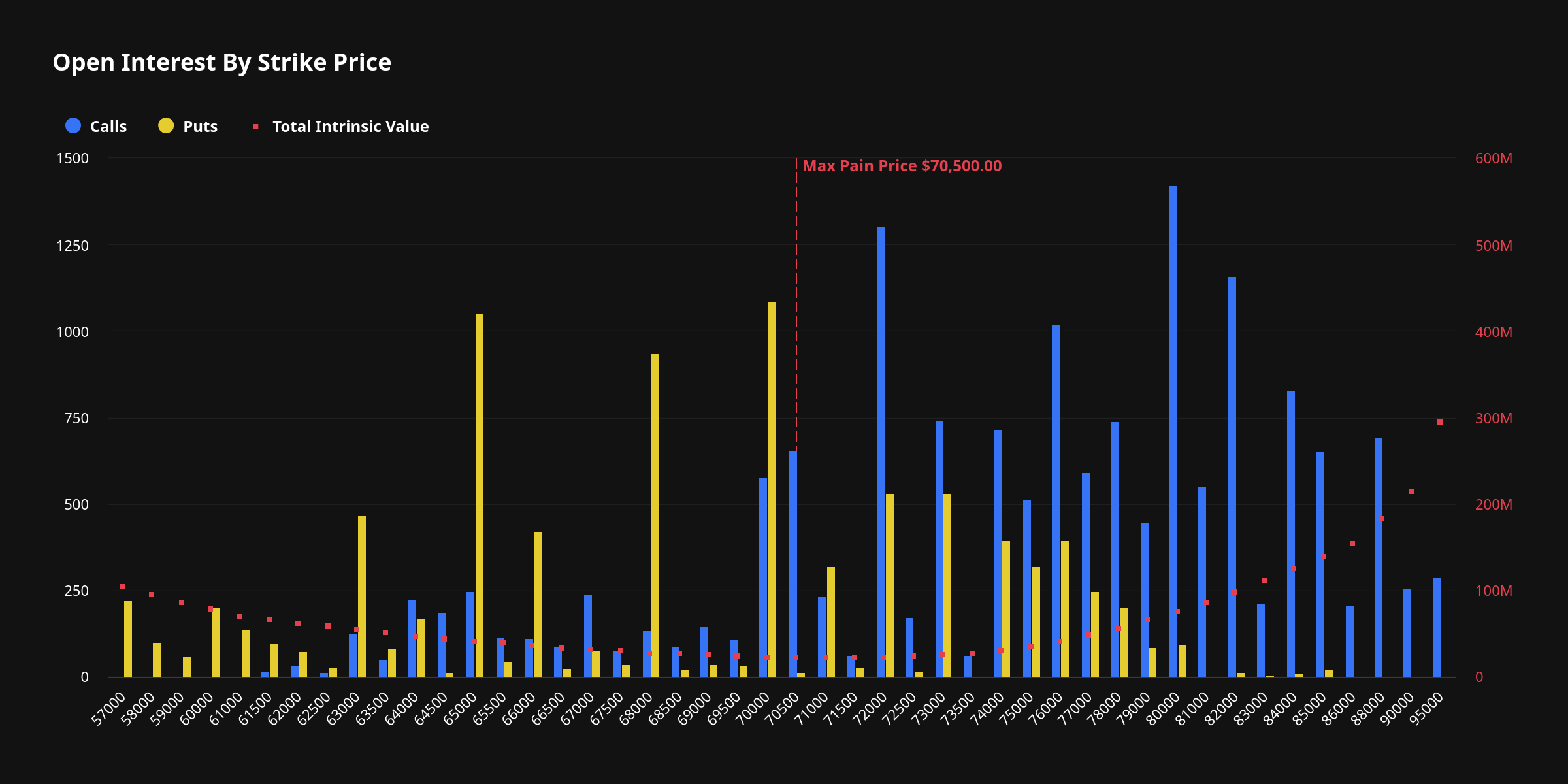

Deribit’s 'max pain price'—the strike level where option buyers would collectively incur the greatest losses at expiry, and which traders sometimes use as a proxy for where price may be magnetized into settlement—was estimated at $2,000 for Ethereum, $82 for Solana, and $1.30 for XRP.

Looking at the largest open interest clusters by strike, Ethereum’s heaviest positioning included $2,150 calls alongside substantial put interest at $2,000 and $1,800. The mix suggested that while some traders were still positioning for a move back toward higher resistance, a significant portion of the market remained concerned about a retest or breakdown of widely watched support zones.

For Solana, the most concentrated open interest was dominated by calls near $82–$88, including $87, $82, and $88 call strikes. That clustering at adjacent upside levels typically reflects traders targeting a near-term rebound and attempting to capture a potential breakout move rather than merely insuring existing spot holdings.

XRP’s largest open interest strikes, meanwhile, were led by calls at $1.38, $1.20, and $1.26, indicating a notable amount of upside positioning despite the overall open interest put/call ratio leaning bearish. The apparent contradiction highlights a nuance of the options market: aggregate put/call ratios can be pulled by strike distribution and contract concentration, even when the most popular individual strikes are skewed toward calls.

Short-term flow data over the prior 24 hours further emphasized the split in sentiment. Total options volume was reported at 216,135 contracts for Ethereum, 119,670 for Solana, and 5,251,000 for XRP. Over that period, the volume-based put/call ratio rose to 1.48 for Ethereum and 1.32 for XRP—both pointing to stronger put activity—while Solana remained call-heavy with a ratio of 0.51.

The most actively traded contracts reflected that defensive bias in Ethereum, with put activity concentrated in strikes such as $1,600 and $1,700 for June 26 expiries, alongside notable interest in shorter-dated $1,700 puts and $1,800 calls expiring June 5. Solana’s top-traded contracts included an $80 put expiring June 5 and a mix of calls at $70, $86, and $94 across near- and late-June expiries—suggesting traders were simultaneously hedging near-term volatility while keeping upside optionality. For XRP, high-volume trades included a $1.36 put expiring June 5 as well as longer-dated September contracts spanning $1 puts and $2 calls, consistent with both downside hedging and longer-horizon upside speculation.

Spot prices were broadly lower at the time of the snapshot. Ethereum fell 1.22% on the day to $1,756, Solana slid 2.34% to $68.27, and XRP dropped 2.15% to $1.156, according to TokenPost Market data cited in the report.

Overall, the options tape suggests a market that is not moving in lockstep: Solana traders appear more willing to express 'risk-on' views via calls, while Ethereum and XRP show stronger 'risk management' demand through puts. If the skew persists, it could shape liquidity and volatility dynamics into upcoming expiries—particularly as traders reposition around key technical levels and macro-driven risk events—without implying a clear directional outcome for spot prices.

🔎 Market Interpretation

- Altcoin options sentiment split: Solana (SOL) shows a stronger upside bias (call-heavy), while Ethereum (ETH) and XRP lean more defensive with greater near-term demand for downside hedges (put activity).

- Same-day expiry positioning (June 5): Open interest stood at 153,417 ETH contracts (~$269.11M), 12,069 SOL (~$8.25M), and 5,175 XRP (~$5.97M), indicating ETH dominates short-dated options risk.

- Open-interest put/call ratios: ETH 0.92 (near-neutral/slight call skew), SOL 0.55 (clear call dominance), XRP 1.16 (more puts than calls overall).

- Volume-based sentiment turned more defensive in ETH/XRP: Over the past 24 hours, put/call by volume rose to 1.48 (ETH) and 1.32 (XRP), while SOL remained call-driven at 0.51—suggesting active hedging in ETH/XRP versus more rebound positioning in SOL.

- “Max pain” magnets into expiry: Estimated max pain levels were $2,000 (ETH), $82 (SOL), $1.30 (XRP), which traders sometimes watch as potential settlement “gravity” points.

- Spot backdrop was risk-off: Prices were lower at the snapshot—ETH $1,756 (-1.22%), SOL $68.27 (-2.34%), XRP $1.156 (-2.15%)—making the SOL call skew notable relative to weak spot performance.

- Key takeaway: The tape does not confirm a single market direction; instead it highlights divergent hedging vs. risk-on behavior that may influence liquidity and volatility around upcoming expiries.

💡 Strategic Points

- ETH: cautious, support-aware positioning. Despite an OI put/call near 1.0, meaningful put interest around $2,000 and $1,800 plus active trading in $1,600–$1,700 puts (June 26) signals traders are prioritizing drawdown protection near widely watched supports.

- SOL: rebound/breakout expression. Concentrated calls clustered around $82–$88 (e.g., $82/$87/$88) indicate traders are positioning for a faster upside move (recovery or breakout) rather than a slow grind higher.

- XRP: hedging dominates, but upside interest exists. Overall put/call > 1 implies defensive skew, yet notable call OI at $1.20–$1.38 suggests participants are simultaneously hedging near-term downside while keeping exposure to a rebound.

- Interpret put/call ratios with strike context. XRP illustrates a common nuance: headline put/call ratios can look bearish even when the most popular strikes are calls, due to how positions are distributed across strikes and expiries.

- Watch expiry-driven flows. With large same-day expiries and identifiable strike clusters, pinning (price gravitating toward max pain) and rapid changes in dealer hedging can amplify intraday volatility, especially around ETH’s heavily traded downside strikes.

- Scenario framing:

- Consolidation case: Near-parity ETH OI put/call and max-pain proximity may favor range trading into settlement.

- Rebound case: SOL’s call concentration suggests traders see asymmetric upside if momentum returns.

- Risk event sensitivity: Persistent elevated put volume in ETH/XRP implies markets are still pricing meaningful tail-risk, which can keep implied vol supported.

📘 Glossary

- Options Open Interest (OI): The number of outstanding option contracts that remain open (not closed or expired). Higher OI often indicates higher market attention at that expiry/strike.

- Put/Call Ratio (OI-based): Puts divided by calls using open interest; < 1 suggests more calls (more upside positioning), > 1 suggests more puts (more hedging/defensive positioning).

- Put/Call Ratio (volume-based): Puts divided by calls using trading volume over a period; can reveal what traders are doing now, even if OI remains dominated by older positions.

- Call Option: A contract that generally benefits from the underlying price rising (right to buy at a set strike price).

- Put Option: A contract that generally benefits from the underlying price falling (right to sell at a set strike price); often used for downside protection.

- Strike Price: The preset price level at which an option can be exercised; clusters of OI at certain strikes can act as market “reference points.”

- Max Pain Price: The strike level where option buyers would collectively experience the greatest losses at expiry; sometimes watched as a potential “pin” level, though it is not a guarantee.

- Skew: The relative preference/price/positioning between puts and calls (or between strikes), often used to infer whether the market is paying up for downside protection or upside exposure.

- Hedging: Using derivatives (often puts) to reduce downside risk on spot or other exposures.

Comment 0