News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

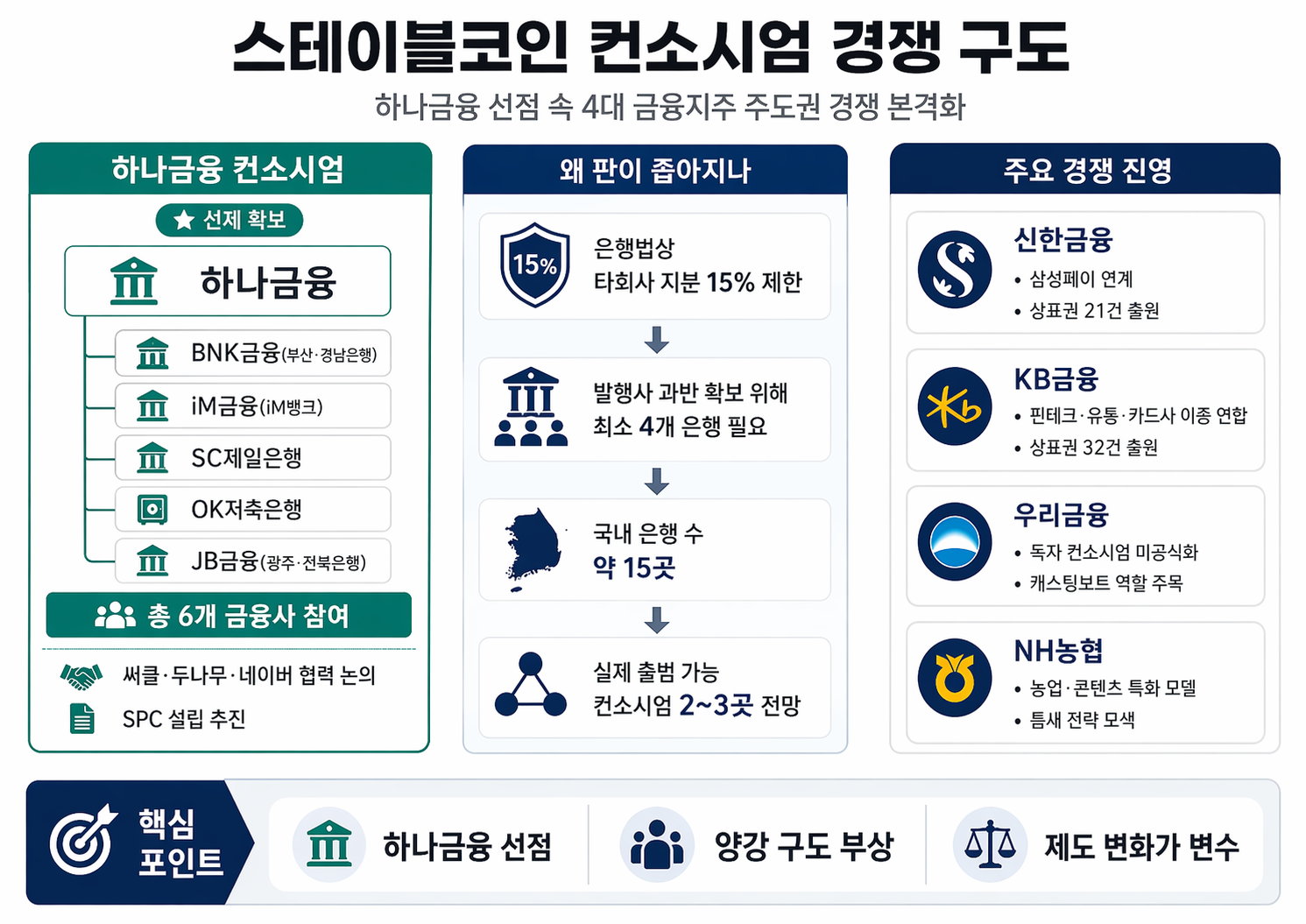

South Korea’s push toward bank-backed stablecoins is rapidly turning into a race for control, as Hana Financial Group moves to lock in partners early—potentially squeezing rivals as regulatory limits make it difficult for more than a handful of issuance groups to form.

Hana Financial Group said it has effectively secured a six-institution lineup for a stablecoin issuance consortium, drawing in BNK Financial Group (parent of Busan Bank and Kyongnam Bank), iM Financial Group (iM Bank), Standard Chartered First Bank Korea (SC First Bank), OK Savings Bank, and JB Financial Group (linked to Jeonbuk Bank and Gwangju Bank). The group is widely viewed as the first among Korea’s “big four” financial holding companies to formalize a bank-heavy structure aimed at launching a won-linked stablecoin.

The consortium approach matters because of a key structural constraint in Korea’s banking rules. Under the country’s Bank Act, banks are generally restricted to holding no more than 15% of another company’s equity. In practice, that cap means a stablecoin issuer designed to be bank-controlled—requiring over 50% ownership—would need at least four banks to participate simply to reach majority control. With a limited pool of domestic banks, early recruitment could determine which consortia are viable and which are not.

Korea’s commercial banking universe is relatively small: about seven nationwide banks, five regional banks, three internet-only banks, plus SC First Bank. With Hana already tying up multiple banks, the remaining pool for competing consortia narrows quickly—particularly because major incumbents are competitors and may be reluctant to share governance inside a single issuer.

Industry sources also expect internet banks to pursue more independent paths, leveraging ties to platform ecosystems such as Kakao and Toss. “Unless the 15% ownership cap is adjusted, you need multiple banks to build a consortium,” one banking-sector official said, adding that legal amendments would be difficult. Even if regulators allow multiple licenses, market participants increasingly estimate that only two or three issuance groups could realistically launch at scale under the current framework.

Hana’s early move is also being reinforced by partnerships beyond banking. The group has signed an MOU with Circle, the issuer behind USD Coin (USDC), and has reportedly maintained discussions with Dunamu (operator of Upbit) and Naver Financial over potential collaboration. Separately, it is pursuing additional agreements with companies in travel, telecommunications, insurance, and commerce to secure real-world payment and settlement use cases—while also working on plans to establish a special purpose company (SPC) that would serve as the issuing entity.

Shinhan Financial Group is widely seen as Hana’s closest rival in the emerging ‘two-horse race.’ Shinhan Chairman Jin Ok-dong has taken a direct interest in stablecoin discussions, and the group has filed 21 related trademark applications. Shinhan’s core strategy is integration with Samsung Pay’s payment rails, aiming to translate domestic point-of-sale reach into a scalable stablecoin distribution network and build out a cross-border remittance angle in parallel.

KB Financial Group is pursuing differentiation through a broader ‘cross-industry alliance’ rather than a bank-centric coalition. Potential partners cited by market participants include fintech and platform players such as Toss (Viva Republica), Samsung Card, and Circle. KB is also reported to have completed a proof-of-concept with Circle. The group’s messaging has centered on ‘programmable money’—a concept that enables conditional payments and automated settlement via smart contract-like logic—positioned as a tool to support small merchants and local economies, while emphasizing ‘stability’ and standardized ‘interoperability.’ KB has filed 32 trademarks tied to stablecoin-related branding, the most among the major players.

Woori Financial Group has not yet announced a standalone consortium, leaving the market to treat it as a potential ‘kingmaker.’ The group is reportedly reviewing ways to expand collaboration with Samsung Wallet and exploring corporate use cases through its equity investment in custody provider BDACS. Analysts say Woori’s eventual alignment could determine whether Korea settles into a durable ‘two-leader’ structure or tips toward a more dominant single consortium.

NH NongHyup Bank is experimenting with a narrower, sector-focused model that diverges from the large commercial-bank playbook. It has been working with Samsung Securities and SK Securities on joint development of a token platform and has discussed linking stablecoins to K-pop content finance with Musicow and Aton. Local reports also indicate that NH is preparing token issuance tied to ‘smart farm’ initiatives that leverage its agricultural network.

With the regulatory architecture still unsettled, some observers are now raising a scenario in which additional banks choose to join Hana’s consortium—even at the cost of smaller individual equity stakes—because the combination of a large user base, a major exchange operator, and everyday payment channels could strengthen distribution. At the same time, the same legal structure that forces broad consortia today could be altered if regulators classify stablecoin issuance as a permitted bank-subsidiary business. That shift could allow a bank to exceed the 15% cap and, in theory, establish an issuer with majority or even full ownership—dramatically changing consortium math and competitive dynamics.

Another unresolved issue is whether a single bank could participate in multiple consortia. Korea’s past internet-bank formation process raised conflicts-of-interest concerns when shareholders joined competing groups, but market participants note that stablecoin issuers could be treated differently depending on licensing design, governance rules, and the eventual contours of the country’s forthcoming digital asset legislation.

For now, most arrangements remain at the non-binding MOU stage, leaving room for realignment. Still, bankers say momentum is building. “The likely structure is that major commercial banks lead, with regional banks and other institutions joining,” one industry official said. “Hana moved first by bringing in multiple regional finance groups, and other large banks will intensify their response so they don’t fall behind as stablecoins become a core part of the next payments and settlement stack.”

🔎 Market Interpretation

- First-mover lock-in: Hana Financial is moving early to assemble a bank-heavy stablecoin consortium, potentially constraining rivals because Korea’s limited number of banks makes partner availability a scarce resource.

- Regulatory math drives consolidation: The Bank Act’s 15% equity cap on banks owning other companies means a bank-controlled stablecoin issuer (needs >50% bank ownership) typically requires at least four banks, pushing the market toward a small number of viable consortiums.

- Likely market structure: 2–3 scalable issuers: Even if multiple licenses are allowed, participants believe only two or three issuance groups can realistically reach scale under current constraints and competitive frictions.

- Competition shifts from “who can issue” to “who can distribute”: Beyond licensing, distribution advantages (payments, wallets, exchanges, platform ecosystems) are emerging as the decisive battlefield for adoption.

- Policy risk is the swing factor: If regulators reclassify stablecoin issuance as a permitted bank-subsidiary business (or otherwise relax the cap), the market could pivot from broad consortia to single-bank-led issuers, reshuffling competitive dynamics.

💡 Strategic Points

- Hana’s blueprint: bank consortium + global stablecoin expertise: Hana has lined up six institutions (BNK, iM, SC First Bank, OK Savings Bank, JB Financial) and is reinforcing credibility via an MOU with Circle (USDC), while exploring partnerships with Dunamu (Upbit) and Naver Financial to strengthen distribution and use cases.

- Consortium governance as a moat: Because major banks are competitors, governance friction can prevent “mega-consortiums.” Hana’s early coalition may force rivals into smaller groups or cross-industry alliances with different control profiles.

- Shinhan’s strategy: payments rail capture: Shinhan is positioning around Samsung Pay to convert point-of-sale reach into stablecoin circulation, while pairing it with a cross-border remittance narrative; the group is signaling intent through 21 trademarks.

- KB’s strategy: programmable money + interoperability: KB is leaning toward a broader alliance (fintech/platform partners like Toss, Samsung Card, Circle), highlighting conditional/automated payments and standardized interoperability; it has filed 32 trademarks, the most among peers.

- Woori as a “kingmaker”: With no dedicated consortium announced, Woori’s eventual alignment (Samsung Wallet collaboration, custody angle via BDACS) could determine whether the market stabilizes into a two-leader structure or a more dominant single camp.

- NH’s niche play: NH NongHyup is testing sector-specific issuance concepts (token platform with securities firms; potential links to K-pop content finance; “smart farm” tokenization), suggesting a specialized model rather than mass-retail payments first.

- Key open questions to watch:

- Can a bank join multiple consortia? Potential conflicts-of-interest may arise depending on final licensing and governance rules.

- Will MOUs convert into binding structures? Many partnerships are non-binding, so late-stage reshuffles remain likely as regulation clarifies.

- Issuer vehicle design: Hana’s plan for an SPC indicates how groups may structure ownership to satisfy control requirements while bringing in non-bank distribution partners.

📘 Glossary

- Stablecoin: A digital token designed to maintain a stable value, typically pegged to a fiat currency (here, the Korean won).

- Won-linked stablecoin: A stablecoin pegged to KRW, intended for domestic payments/settlement and potentially remittances.

- Consortium (issuance consortium): A group of institutions jointly forming/owning an issuer entity to meet regulatory ownership/control requirements and share governance.

- Bank Act 15% ownership cap: A Korean rule generally limiting banks to holding no more than 15% of another company’s equity—driving the need for multi-bank ownership to achieve majority control.

- Majority control (>50%): Ownership level typically required to be considered “bank-controlled” for a stablecoin issuer under the described structure.

- SPC (Special Purpose Company): A dedicated legal entity created for a specific function—here, to act as the stablecoin issuing vehicle and accommodate ownership rules.

- MOU (Memorandum of Understanding): A non-binding agreement outlining intent to cooperate; often a precursor to definitive contracts.

- USDC: USD Coin, a major U.S. dollar stablecoin issued by Circle, often used as a reference model for reserve management and compliance practices.

- Programmable money: Money that can execute rules/conditions automatically (e.g., release payment on delivery confirmation), often implemented with smart-contract-like logic.

- Interoperability: The ability for different payment networks, wallets, exchanges, and institutions to transfer and recognize the same digital asset smoothly and consistently.

- Payment rails: The underlying infrastructure and networks that move money (e.g., Samsung Pay-enabled merchant acceptance networks).

Comment 0