News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

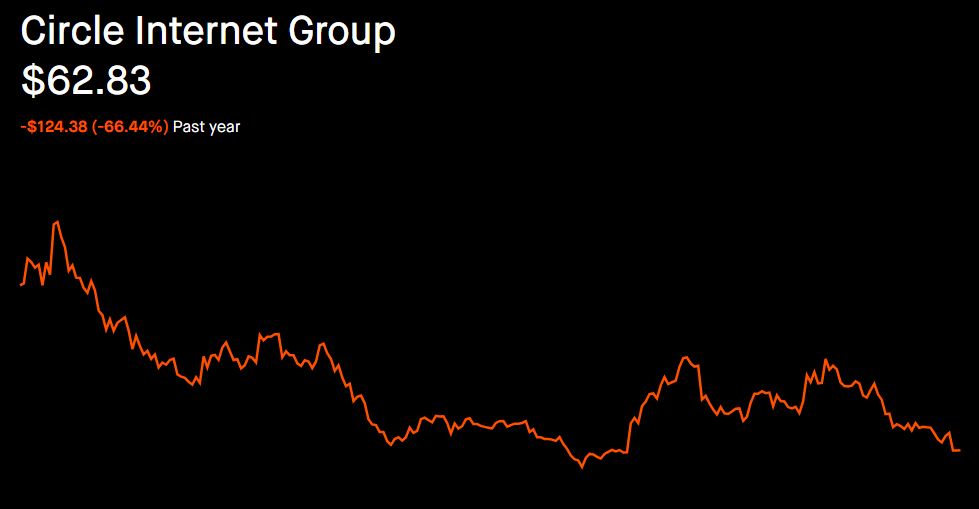

Shares of Circle Internet Group ($CRCL) slid 17.5% in a single session to close at $62.63, their lowest level in roughly four months, as markets digested the launch of a new consortium-backed dollar stablecoin, Open USD (OUSD). The selloff underscored a growing investor concern that Circle’s USDC-driven business model is facing a structural challenge as the stablecoin industry experiments with more ‘open’ and revenue-sharing frameworks.

The drop compounded an already sharp pullback. Circle is now down more than 40% over the past month, about 21% year-to-date, and roughly 51% below its 2026 peak. Some fund commentators have characterized the stock as a case where ‘crypto exposure’ can mask classic equity risks—namely margin sensitivity, partner concentration, and business-model durability in a fast-evolving market.

Street views remain divided. MarketBeat data cited Circle’s estimated fair value around $64.56, while the average 12-month price target stood near $117.38, with a wide dispersion between $190 on the high end and $55 on the low end. Notably, Compass Point analysts turned sharply more cautious, cutting their target to $55 from $97—an adjustment that aligns with the market’s reassessment of how defensible Circle’s economics are if stablecoin distribution partners gain more leverage.

At the center of the repricing is Open USD, a new dollar-pegged stablecoin launched by what reports describe as a consortium of more than 140 corporate partners spanning financial firms, crypto companies, and key USDC distribution players. The model’s defining pitch is partner alignment: OUSD is designed to redistribute a larger share of reserve interest income to participating members than traditional issuer-centric structures.

That proposition directly challenges Circle’s core profit engine. Circle derives approximately 99% of its revenue from interest earned on USDC reserves, making net income highly sensitive to both the level of interest rates and the company’s ability to retain economics in distribution agreements. In 2024, Coinbase ($COIN) reportedly paid Circle about $908 million in revenue-sharing related to USDC; analysts say the decision by major distributors to join the Open Standard alliance could increase pressure on Circle’s margins and bargaining power.

Market strategists also point to architecture. OUSD’s ‘open standard’ approach may erode the moat enjoyed by issuer-led stablecoins by making it easier for multiple stakeholders to coordinate issuance, distribution, and incentives under shared governance. Circle’s CEO has publicly raised concerns about consortium governance, referencing difficulties Circle faced in prior attempts to operate within similar multi-party structures—an implicit warning that shared control can complicate decision-making, risk management, and compliance responsibilities.

The competitive backdrop is already shifting. USDC’s market share is estimated to have fallen about 17% so far this year. Meanwhile, regulation is reshaping stablecoin supply lines, particularly in Europe as MiCA compliance changes which tokens can be offered and on what terms. Against that backdrop, OUSD’s arrival is being interpreted as an accelerant for an industry-wide move toward ‘shared economics’—a model that could force incumbents to choose between defending margins or protecting distribution.

Circle’s latest operating results added to the market’s caution. The company reported earnings per share that missed expectations by $0.06 and posted a net profit margin of about -2.76%. Analysts linking those figures to the current debate argue that when nearly all revenue is tied to reserve yield, any dilution of interest income—whether through revenue-sharing, competitive pricing, or partner renegotiations—can quickly translate into ‘existential margin pressure’.

For equity investors, the volatility risk is also rising. A one-day decline of 17% and reports that the stock could be excluded from certain Russell growth benchmarks may reduce passive inflows and complicate liquidity conditions. Institutional investors are estimated to hold roughly $25.25 million in $CRCL, though some allocators have reportedly begun reclassifying the position as primarily an equity-risk exposure rather than a proxy for crypto beta.

Circle has not announced a formal revised roadmap in response to OUSD. Still, market participants increasingly expect the company will need to revisit USDC distribution economics—potentially renegotiating revenue splits or incentives with key platforms and distributors to keep USDC competitive versus partner-friendly alternatives. Investors are likely to focus on any upcoming disclosures around USDC distribution costs, changes in revenue-sharing terms, or broader moves to diversify income streams beyond reserve interest.

Ultimately, the selloff reflects a larger question: whether the centralized, issuer-led stablecoin model can maintain its dominance as the market experiments with consortium governance, ‘open standards,’ and revenue-sharing that spreads reserve yield across ecosystems. With OUSD entering the arena, the balance of power in stablecoins appears to be shifting—and Circle is now a focal point for how incumbents respond to that shift.

🔎 Market Interpretation

- CRCL reprices on business-model risk: Circle shares fell 17.5% to ~$62.63 (4-month low) as investors reacted to the debut of consortium-backed Open USD (OUSD), viewing it as a structural threat to Circle’s issuer-centric stablecoin economics.

- “Open + shared economics” challenges issuer margins: OUSD’s pitch—redistributing more reserve interest income to partners—puts pressure on Circle’s ability to retain take-rate in distribution deals, an issue magnified because ~99% of Circle revenue is tied to USDC reserve interest.

- Street targets highlight uncertainty: Fair value estimates cluster near the current price (~$64.56), but 12-month targets are dispersed (low ~$55, high ~$190). Compass Point’s cut to $55 from $97 signals a shift toward “distribution partners gaining leverage” as the key bear case.

- Fundamental softness amplifies the narrative: A recent EPS miss (-$0.06 vs expectations) and net margin around -2.76% reinforce concerns that even small economic give-ups (revenue share, pricing, renegotiations) can quickly depress profitability.

- Market-structure headwinds: Large single-day volatility and potential Russell growth benchmark exclusion could reduce passive inflows and worsen liquidity dynamics, increasing downside sensitivity during negative catalysts.

💡 Strategic Points

- Watch distribution economics first: The critical KPI is how Circle adjusts USDC revenue-sharing with major partners (notably Coinbase) and what “cost to distribute” looks like going forward. Any increase in revenue split or incentives is a direct margin hit.

- Partner concentration is the key equity risk: With Coinbase historically central to USDC distribution (and material cash flows referenced via revenue-sharing), consortium participation by distributors can structurally weaken Circle’s negotiating position.

- Scenario map for investors:

- Defend margins: Hold issuer economics → risk distribution loss/share erosion as partners favor higher payouts.

- Defend distribution: Pay partners more → preserve footprint but accept lower profitability and more rate-sensitivity.

- Diversify revenues: Build non-reserve-interest lines (payments, tooling, custody/infra fees, enterprise services) → reduces “single-driver” exposure but requires execution and time.

- Governance/operational risk is non-trivial: While OUSD’s consortium model may improve partner alignment, shared governance can complicate decision-making, compliance accountability, and risk management—an area Circle’s CEO flagged based on prior multi-party structure experience.

- Regulation as a competitive lever: MiCA-related changes in Europe can reshape which stablecoins are offered and under what conditions; compliance and distribution access may become as important as yield-sharing in determining winners.

- Market share momentum matters: USDC share is cited as down ~17% this year; continued slippage would imply partners and users are responding to competitive incentives—raising the likelihood Circle must concede economics to stabilize distribution.

📘 Glossary

- Stablecoin: A token designed to maintain a stable value (typically pegged to $1) using reserves and redemption mechanisms.

- USDC: Circle’s U.S. dollar-pegged stablecoin; Circle’s financial performance is heavily linked to its scale and economics.

- Reserve interest income (reserve yield): Interest earned on assets backing a stablecoin (e.g., T-bills/cash equivalents). For Circle, this is the dominant revenue source.

- Revenue-sharing / distribution economics: Agreements where the issuer shares reserve income with exchanges/platforms that distribute the stablecoin (e.g., paying partners to promote/hold/use the token).

- Consortium-backed stablecoin: A stablecoin issued/governed by a group of firms rather than a single issuer, typically with shared incentives and governance.

- Open standard (in stablecoins): A framework intended to let multiple stakeholders coordinate issuance, distribution, and incentives under a common rule set, potentially lowering switching costs.

- Moat: A durable competitive advantage (brand, distribution, regulation/compliance, liquidity) that protects profits from competitors.

- MiCA: The EU’s Markets in Crypto-Assets regulation, which sets rules for crypto assets including stablecoin issuance and distribution in Europe.

- Russell growth benchmarks: Equity indices used for passive/benchmark tracking; exclusion can reduce index-linked demand for a stock.

- Crypto beta vs equity risk: “Crypto beta” implies price moves mainly with the crypto market; “equity risk” emphasizes company-specific fundamentals like margins, concentration, and execution.

Comment 0