News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

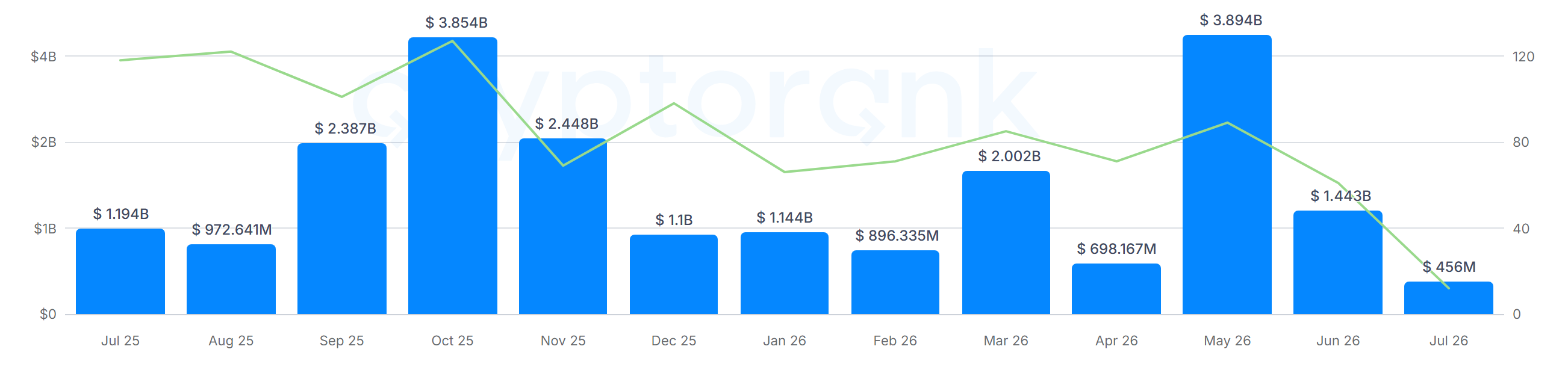

Crypto venture funding has cooled sharply in early July, with startups raising a combined $456 million across 12 disclosed rounds from July 1 to July 12, according to data compiled by CryptoRank. The pullback underscores a broader risk-off tone in private markets, even as major tokens continue to benefit from periodic bursts of spot demand and headline-driven volatility.

In month-over-month terms, the slowdown is stark. Total dollars invested fell 68.4% from June’s roughly $1.44 billion spread across 61 rounds, while the number of deals dropped 80.3%. Compared with May—when activity reached about $3.89 billion across 89 rounds—July’s funding tally is down 88.3%, highlighting how quickly the market shifted from spring’s relatively active pace to a more cautious summer posture.

The biggest disclosed raise in the period came from Prime Intellect, which secured $130 million in a Series A led by Radical Ventures and other investors on July 8. While the report did not provide detailed business metrics, the size of the round stood out in a month defined by smaller checks and fewer transactions, suggesting that capital is concentrating in a narrower set of high-conviction themes and teams.

Other notable rounds included Gauntlet’s $125 million Series C on July 9 and EDX Markets’ $76 million Series C on July 7, both listing SBI Holdings as an investor. Mercado Bitcoin also raised $20 million in a strategic investment from Tether, while KOR Protocol brought in $7.5 million in a Series A backed by Blockchain Capital and others. Earlier in the month, M1X Global raised $5.5 million in a seed round involving Paradigm and additional participants.

M&A activity was also recorded, though financial terms were not disclosed. Cypher was acquired by Nium, and 01.xyz was acquired by N1, according to the same dataset.

Beyond the first-half-of-month snapshot, broader indicators also point to weaker momentum. Over the most recent 30-day window, the report’s investment activity index declined 50% from the prior month, landing in the ‘Low’ range. During that period, 56 rounds were tracked—down 50%—with total investment volume estimated at approximately $1.79 billion, a 79.9% month-over-month decline.

The average round size was generally in the $3 million to $10 million range, suggesting that investors are still willing to fund early and mid-stage projects, but with tighter underwriting standards and fewer large-scale financings. ‘Strategic investment’ rounds were cited as the most active stage, a pattern often associated with corporates and ecosystem players prioritizing partnerships, product integration, and distribution advantages amid uncertain market conditions.

Capital flows were most concentrated in the API segment during the latest period, indicating sustained demand for infrastructure that helps institutions and developers connect to on-chain activity, data, and execution venues. Over the past six months, however, the largest share of funding was attributed to payments, accounting for 27.88% of investment allocation, followed by API (23.08%), ‘real-world assets’ (RWA) (18.27%), decentralized exchanges (DEX) (16.35%), and developer tools (14.42%).

On the investor side, Coinbase Ventures was the most active firm by deal count with 30 investments over the referenced window. It was followed by Animoca Brands (20), Tether (18), Andreessen Horowitz (a16z) crypto (17), GSR (12), Castrum Capital (10), and Becker Ventures (10). The distribution suggests that a core group of specialized crypto investors continues to drive much of the market’s deal flow, even as total volumes contract.

Overall, the early-July data paints a market in consolidation: fewer deals, smaller average checks, and a premium placed on infrastructure and revenue-adjacent categories like payments. If the subdued pace persists, the remainder of the quarter may hinge on whether token prices stabilize enough to revive ‘risk capital’ appetite—or whether investors continue to prioritize select, high-signal opportunities while leaving the broader startup field in a funding drought.

🔎 Market Interpretation

- Sharp venture cooldown in early July: Crypto startups raised $456M across 12 rounds (Jul 1–12), signaling a decisive shift to risk-off behavior in private markets despite ongoing token-price volatility.

- Compression versus prior months: Funding fell 68.4% vs June ($1.44B/61 rounds) and 88.3% vs May ($3.89B/89 rounds), while deal count dropped 80.3% vs June—a rapid re-pricing of capital availability.

- Capital is concentrating: Mega-rounds are rarer, but select deals still clear: Prime Intellect ($130M Series A), Gauntlet ($125M Series C), EDX Markets ($76M Series C). This points to investors favoring high-conviction teams/themes over broad exposure.

- Momentum indicators confirm weakness: The 30-day investment activity index dropped 50% into the “Low” range; estimated volume was $1.79B (down 79.9% MoM) across 56 rounds (down 50% MoM).

- Stage mix suggests partnership-led deployments: “Strategic investment” was the most active stage, implying corporates/ecosystem players are prioritizing distribution, integrations, and commercial tie-ups rather than large speculative financings.

- Sector preference: Recent flows concentrated in API/infrastructure (connectivity to on-chain data/execution). Over 6 months, allocation skewed to payments (27.88%), then API (23.08%), RWA (18.27%), DEX (16.35%), dev tools (14.42%)—favoring revenue-adjacent plumbing over higher-beta apps.

💡 Strategic Points

- For founders: Expect longer fundraising cycles and tighter diligence. Position raises around clear revenue paths, measurable traction, and integration-ready product narratives—especially in payments, API, and institutional tooling.

- Round sizing reality: With average rounds clustering around $3M–$10M, plan burn and milestones accordingly; prioritize capital efficiency and milestone-based extensions over assuming a quick upsized Series.

- Target “strategic” capital: Given activity in strategic rounds, pursue partnerships that can deliver distribution (exchanges, stablecoin issuers, custodians, payment rails) and reduce CAC via ecosystem channels.

- Investor behavior: Deal flow is increasingly driven by a core set of specialists—Coinbase Ventures (30 deals), Animoca (20), Tether (18), a16z crypto (17), GSR (12). Optimize outreach toward investors still actively deploying.

- Watchlist signals for a rebound: A meaningful pickup likely requires (1) token-price stabilization, (2) improved macro risk appetite, and (3) renewed issuance/exit pathways. Until then, expect consolidation and selective funding.

- M&A as an alternative outcome: With terms undisclosed but activity present (Cypher→Nium, 01.xyz→N1), weaker funding markets may increase acqui-hires and tuck-in acquisitions for teams with strong tech but limited runway.

📘 Glossary

- Risk-off: Investor preference shifts toward safer assets/strategies, reducing speculative allocations like early-stage venture.

- Round / Deal: A disclosed financing event (seed, Series A/C, strategic), typically reported with amount, investors, and stage.

- Series A / Series C: Venture stages; Series A often funds early scaling after product validation, while Series C supports later-stage growth/expansion.

- Strategic investment: Capital deployed primarily for business synergies (partnerships, distribution, integration) rather than purely financial returns.

- Underwriting standards: The diligence and risk criteria investors apply (unit economics, compliance, market size, runway, governance).

- API segment: Infrastructure enabling software-to-software connectivity (on-chain data access, trading/execution, wallets, custody interfaces).

- RWA (Real-World Assets): Tokenization or on-chain representation of off-chain assets (bonds, credit, real estate, commodities).

- DEX (Decentralized Exchange): On-chain trading venue using smart contracts rather than centralized order matching and custody.

- M&A: Mergers and acquisitions; common in downcycles as stronger firms buy tech, talent, or market share.

Comment 0