News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Crypto is no longer just a speculative bet — it’s turning into a working part of personal finance. The surge in Visa and Mastercard-backed “crypto cards” this year has turned payments into a new battleground, blending rewards, staking yields, and decentralized finance (DeFi) features into a single piece of plastic — or rather, a line of code.

The global crypto card market is projected to expand from roughly $1.5 billion in 2024 to $1.8 billion in 2025. InsightAce Analytic forecasts annualized growth above 18%, driven largely by Europe and Asia-Pacific, where regulators have shown more openness to digital asset integration with traditional payment rails.

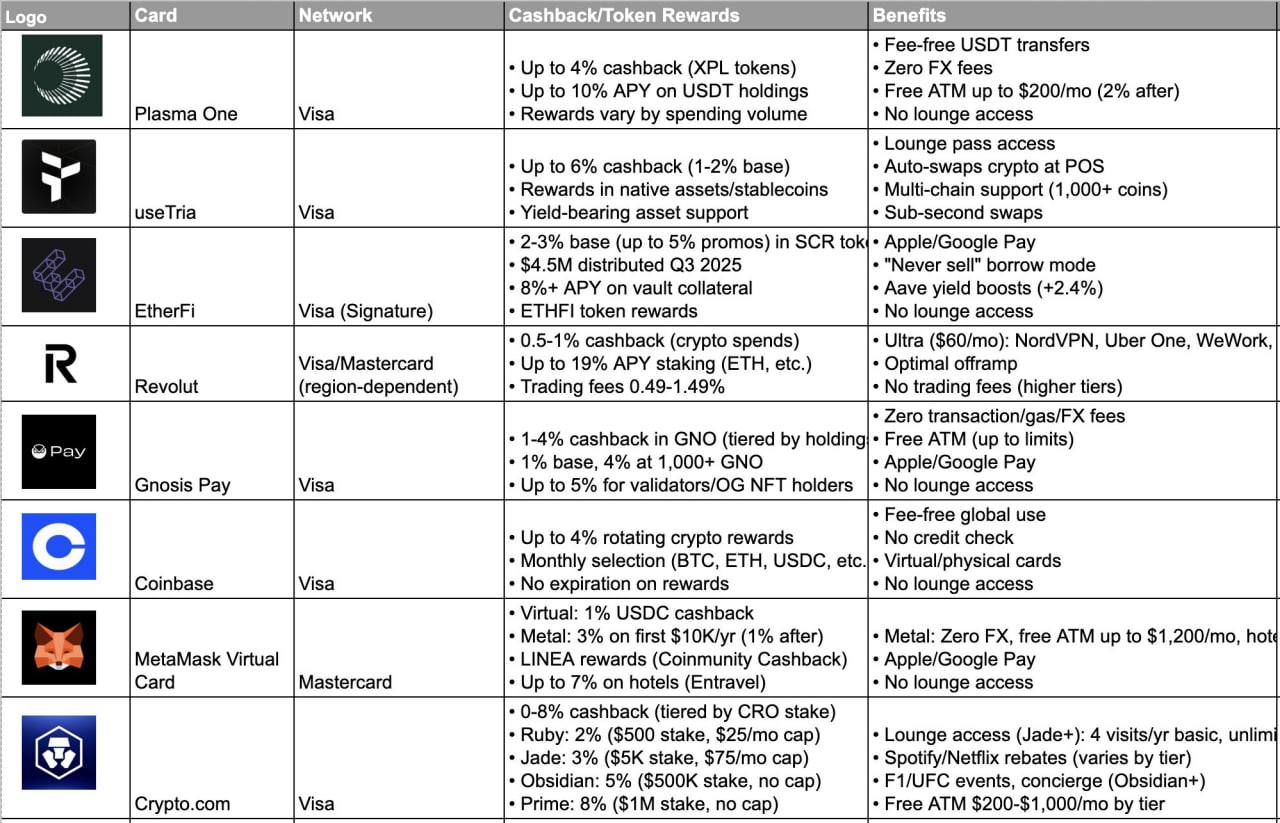

Across this fast-evolving landscape, a handful of contenders are defining what “spending crypto” really means. Plasma One, running on Visa, offers up to 4% cashback in XPL tokens and 10% annual returns on USDT deposits, alongside zero FX fees and free global transfers. EtherFi, also on Visa’s Signature tier, operates on a non-custodial model — users retain control of their assets while earning 8% or more on vault collateral, with features like Aave-integrated boosts and “never-sell” loan options.

Meanwhile, useTria, still in beta, markets itself as a multi-chain lifestyle card with up to 6% promotional cashback, sub-second swaps, and even lounge access under testing. Revolut, already a household fintech brand, is leaning into crypto as a yield enhancer, offering up to 19% APY staking on select assets, plus small cashback on everyday spending. Premium users also gain bundled perks like NordVPN, WeWork credits, and Uber One.

On the more crypto-native side, Gnosis Pay leverages its Safe wallet ecosystem to enable gas-free transactions. Cardholders earn 1–4% cashback in GNO, rising to 5% for validators and OG NFT holders. MetaMask’s Virtual Card, a Mastercard product, extends the brand’s wallet dominance into payments — offering 1–3% cashback, Linea-based rewards, and compatibility with Apple and Google Pay. And Crypto.com’s Visa, arguably the veteran in this space, continues to dominate tiered cashback rewards tied to CRO token staking, along with Netflix and Spotify rebates, and lounge access for higher-tier users.

The common thread among these products is how they’ve transformed crypto cards from simple payment tools into income-generating financial instruments. Yield-bearing accounts like Plasma One and EtherFi make traditional savings accounts look lethargic, while cashback-focused products such as Crypto.com and useTria reward everyday consumption like investment behavior. Each swipe, tap, or online checkout doubles as a staking or earning event.

That fusion of finance and blockchain has also sparked a quiet “staking war.” Revolut and Crypto.com use tiered staking to gate benefits, while EtherFi and MetaMask tie directly into DeFi protocols to court more advanced users. Revolut’s decision to push staking APYs as high as 19% reflects how far fintechs are willing to go to compete for crypto liquidity.

Yet the yield race comes with familiar caveats. Most APY rates are variable and depend heavily on market conditions. Token-based rewards can lose value quickly, and beta-stage products like useTria have yet to prove long-term stability or compliance across jurisdictions. Regulatory uncertainty, regional access limits, and security audits remain weak points in this new ecosystem.

Still, the direction is clear. What began as a novelty — the ability to buy coffee with Bitcoin — has matured into a full-fledged financial layer bridging traditional banking and decentralized networks. In 2025, crypto cards are no longer just a gateway to payments; they’re becoming the front door to Web3 finance itself — where yield, credit, and identity live side by side in the same digital wallet.

Comment 0