News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Crypto research units are increasingly converging on the same conclusion: the market’s next leg is being constrained less by narratives and more by a stubborn combination of tightening risk, muted marginal buying, and a growing need for infrastructure that makes on-chain activity feel as seamless as mainstream fintech.

In a weekly round-up circulated Thursday ET, multiple reports—including notes from Kaiko Research, Crypto.com, Tiger Research, and Messari Research—flagged three themes shaping sentiment: lingering macro-policy uncertainty, weak incremental demand for Bitcoin (BTC) despite rising long-term holder supply, and a pivot toward the “plumbing” of the next cycle—execution layers for DeFi, tokenized real-world assets (RWA), stablecoins, and privacy-preserving computation.

Rate-path uncertainty returns as a market constraint

Kaiko Research argued that crypto has become newly sensitive to the U.S. rate outlook after U.S. inflation re-accelerated to 3.8% and a policy transition at the Federal Reserve heightened perceived tightening risk. According to Kaiko’s analysis, since the sequence of headlines around the Fed leadership and the subsequent pause in rate cuts, Bitcoin (BTC) fell around 18%, Ethereum (ETH) declined roughly 27%, and XRP (XRP) slid about 21%.

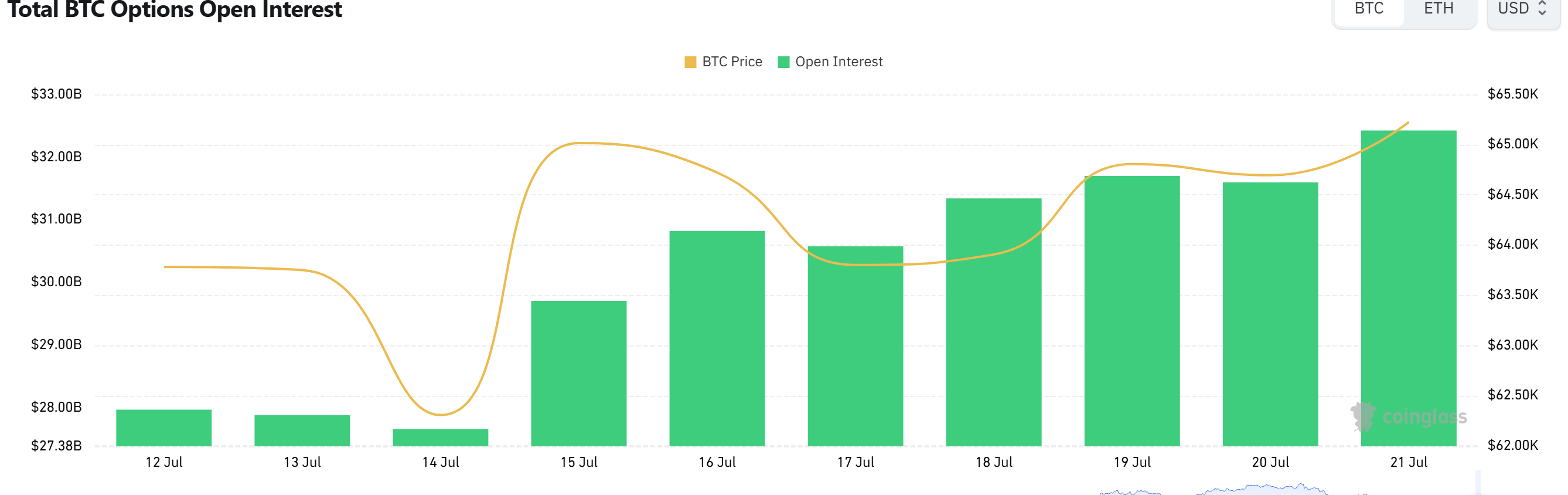

Derivatives positioning thinned alongside spot weakness. Kaiko said BTC perpetual futures ‘open interest’ dropped about 32%—from roughly $23 billion to $16 billion—signaling reduced leverage appetite and less fuel for a rapid rebound if liquidity conditions tighten again.

The firm warned that upcoming inflation and employment readings could become the decisive catalysts. If the data revive expectations for further tightening, the industry could face renewed ‘liquidity compression,’ a dynamic that typically weighs more heavily on high-beta digital assets than on traditional risk markets.

Bitcoin supply tightens—but buyers don’t step in

Crypto.com, meanwhile, focused on a paradox in Bitcoin structure: long-term holder supply has climbed above 15.8 million BTC, an all-time high, yet price momentum has not followed. The company’s read is that the record long-term holdings may reflect ‘buyer stagnation’ as much as conviction—meaning coins are not necessarily being aggressively accumulated, but simply not being traded due to a lack of new demand.

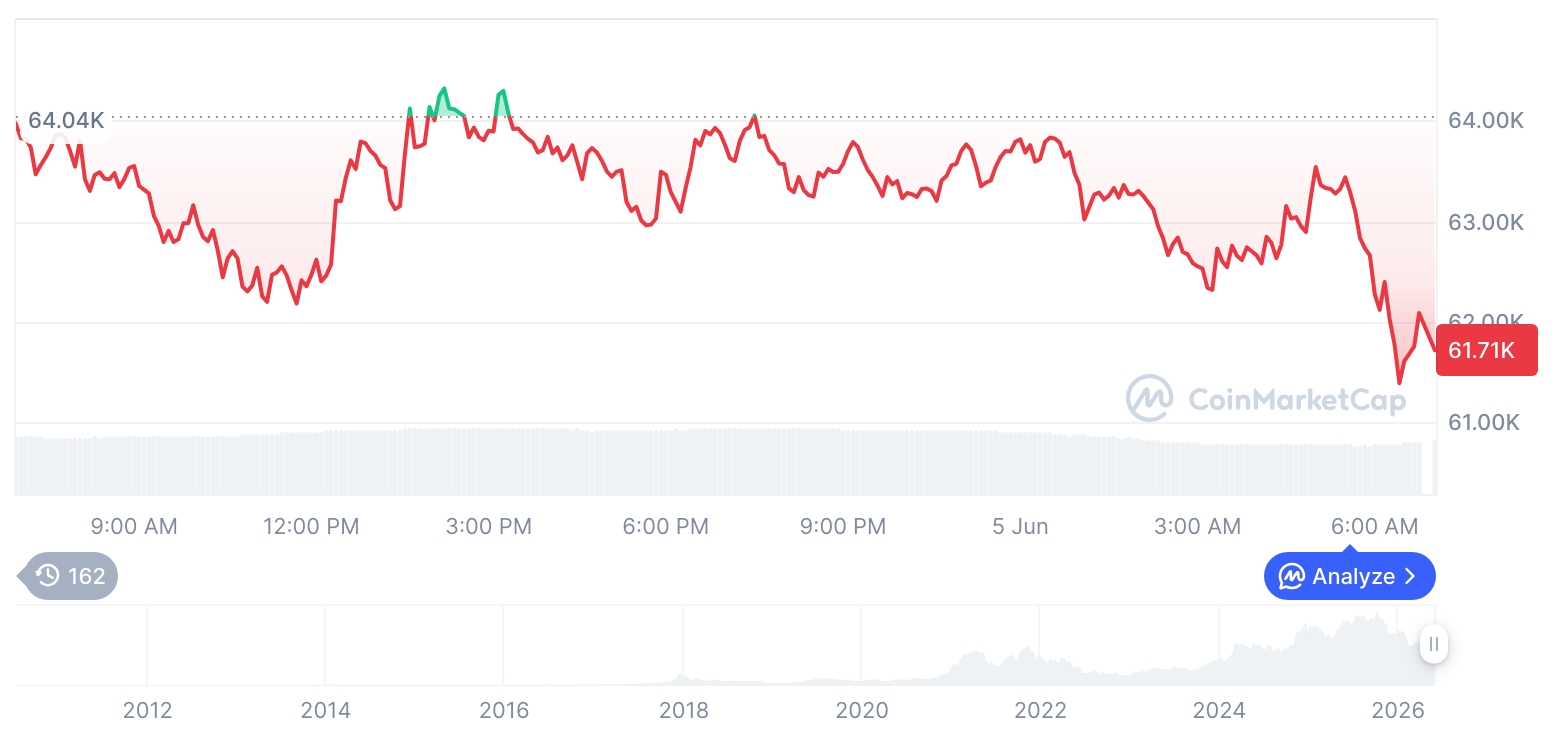

ETF flows reinforced that caution. Crypto.com estimated that U.S.-listed spot Bitcoin (BTC) ETFs recorded approximately $1.4 billion in net outflows over the week, while spot Ethereum (ETH) ETFs saw about $241 million leave. Over the same period, BTC and ETH fell roughly 4.4% and 4.5%, respectively.

The takeaway, according to the report: supply-side tightening alone is not enough to power a recovery if fresh inflows do not return. In the near term, the market’s resilience may hinge on whether ETF demand stabilizes and whether new discretionary buyers re-enter.

DeFi’s bottleneck shifts from protocols to ‘execution layers’

On the product side, Tiger Research argued that DeFi has largely solved core primitives—swaps, lending, yield products, and derivatives—but still lacks the consumer-grade apps and ‘execution layer’ needed to keep non-crypto natives engaged. The firm framed this gap as less about chain throughput and more about simplifying the user journey: onboarding, transaction handling, and multi-chain complexity.

As a case study, Tiger Research highlighted defi.app, saying the product has accumulated $44 billion in total transaction volume and 1.06 million cumulative sign-ups since its February 2025 launch. The report claimed daily active users have grown roughly 3,000% from early levels.

Tiger pointed to ‘gas abstraction’ and ‘chain abstraction’—design patterns that hide fees and cross-chain mechanics from the end user—as key to reducing friction. But it also suggested that long-term retention will depend on repeat-use offerings such as perpetuals products like Rocket Perps, as well as clearer disclosure around on-chain buybacks to build trust through verifiable transparency.

XRPL’s institutional pitch expands via stablecoins and tokenization

Messari Research reported that XRP (XRP) maintained its position as the fourth-largest crypto asset excluding stablecoins, ending Q1 2026 with an approximate market capitalization of $82.21 billion. More importantly, Messari argued that the XRP Ledger (XRPL) is broadening from a payments-focused network toward institutional tokenization and regulated activity.

Messari’s figures showed average daily transactions on XRPL at about 2.48 million, up 35.3% quarter-over-quarter. It also tracked growth in ecosystem components linked to institutional use cases: RLUSD market cap at roughly $340.3 million, up 44.9%, and XRPL-based RWA at about $2.25 billion, up 124.1%.

The report suggested that the combination of a potential spot XRP (XRP) ETF and compliance-oriented DeFi features could push a re-rating of XRPL—from a settlement rail to an institutional-grade infrastructure layer for tokenized assets—particularly if regulated issuers continue to experiment with stablecoin and RWA structures on the network.

Privacy evolves from niche feature to base-layer infrastructure

Messari also examined Octra and its attempt to operationalize fully homomorphic encryption (FHE), a cryptographic method that enables computation on encrypted data. Rather than positioning privacy as only private transfers, the analysis framed Octra as a Layer 1 aimed at executing applications and processing workloads while data remains encrypted—an architecture that could matter for on-chain AI inference and institutional workflows that cannot expose sensitive inputs.

Messari estimated that ‘total private value’ (TPV) across major privacy protocols increased 34% over the past year, from about $8.31 billion to $11.17 billion, reflecting gradual adoption despite regulatory and compliance headwinds. It also noted that Octra’s token, Octra (OCT), has risen roughly 450% from its launch reference price, within a stated total supply structure of 1 billion tokens.

The key question, Messari argued, is whether privacy-preserving compute becomes a real demand driver—through private DeFi, encrypted AI inference, or enterprises seeking confidentiality on public infrastructure. If it does, ‘privacy’ may shift from an optional add-on to a default expectation in blockchain design.

Together, the reports paint a market caught between macro constraints and a structural build-out phase. With rate-path uncertainty and ETF flows shaping near-term risk appetite, research attention is increasingly turning to the layers that can unlock the next wave of users and institutional activity—execution experiences in DeFi, tokenized RWAs and stablecoins, and privacy tech that can support real-world data and computation on-chain.

Comment 0