News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

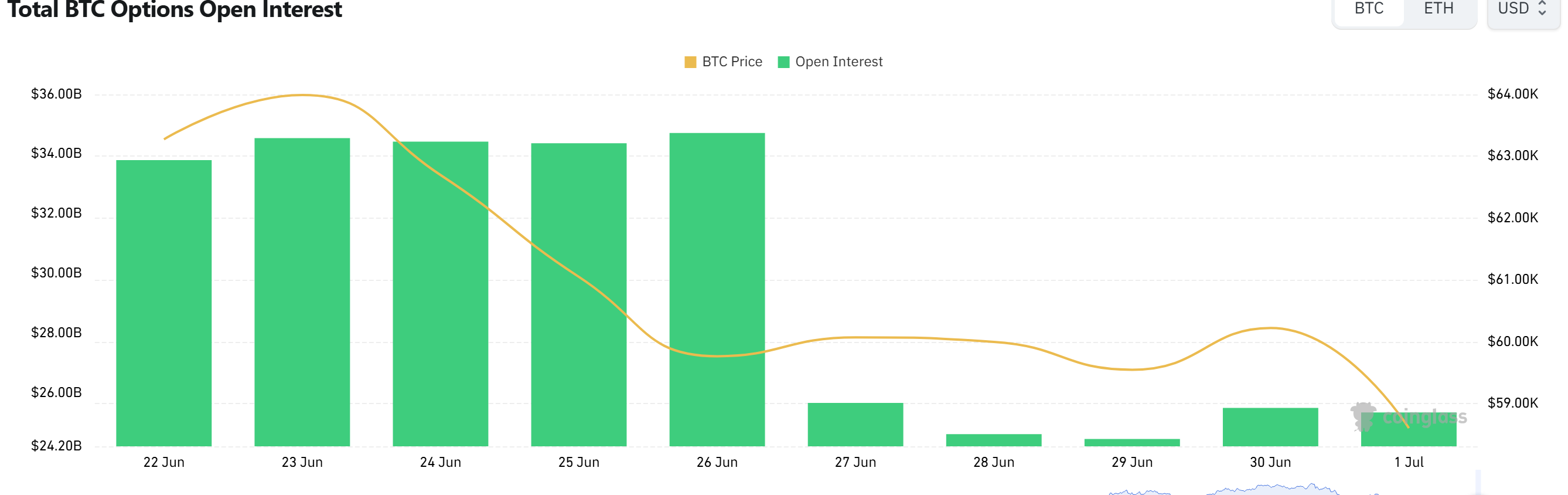

Bitcoin (BTC) options positioning leaned modestly bullish heading into Tuesday in the U.S., with open interest easing slightly while traders funneled most of the past day’s activity into a heavily watched $70,000 call contract on Deribit.

Data compiled by CoinGlass at 12:40 a.m. ET on July 1 showed total BTC options open interest at approximately $24.84 billion, down 0.95% from $25.08 billion a day earlier. Notional trading volume over the prior 24 hours came in around $3.26 billion.

The composition of outstanding positions remained tilted toward upside exposure. Calls accounted for 60.46% of open interest, while puts represented 39.54%. By contrast, the 24-hour flow was nearly balanced, with calls at 50.78% of volume and puts at 49.22%.

That split suggests a market where medium-term positioning still favors higher prices—reflected in the call-heavy open interest—while short-term trading remains two-sided. In practice, a near-even volume mix often indicates that traders are simultaneously pursuing 'upside participation' and 'downside protection' as they manage spot and perpetual exposure, particularly into key expiration windows.

In terms of where risk is concentrated, the largest open interest was clustered in Deribit’s $80,000 call options expiring July 31, followed by Deribit’s $80,000 calls expiring Dec. 25, and Deribit’s $60,000 puts expiring Dec. 25. The lineup points to continued interest in higher strike targets later this year, alongside a meaningful pocket of defensive positioning around $60,000.

Over the past 24 hours, the most actively traded contracts were led by Deribit’s $70,000 calls expiring July 31. Activity then shifted to Bybit’s shorter-dated upside structures, including $60,000 calls and $59,500 calls expiring July 1, highlighting intraday demand for leverage around near-term settlement.

Options are widely used to express directional views with embedded leverage or to hedge spot holdings. A 'call option' gives the right to buy at a predetermined price (typically used for bullish exposure), while a 'put option' gives the right to sell (often used to position for declines or protect against drawdowns). Open interest tracks the total number of outstanding contracts, making it a key gauge of accumulated positioning rather than just day-to-day turnover.

With open interest slightly lower yet trading skewing toward prominent call strikes, the market appears to be rotating exposure rather than layering on fresh risk aggressively. The persistence of sizable put participation in daily flow, however, underscores that traders are still pricing in volatility and keeping hedges close as Bitcoin navigates major strike levels into upcoming expiries.

🔎 Market Interpretation

{

"positioning_signal": [

"BTC options positioning is modestly bullish: calls make up 60.46% of total open interest (OI) vs puts at 39.54%.",

"Total OI dipped slightly to ~$24.84B (-0.95% day/day), suggesting rotation/rebalancing rather than aggressive net new risk-taking.",

"Short-term flow is two-sided: 24h volume is nearly split (calls 50.78% vs puts 49.22%), indicating simultaneous upside participation and downside hedging.",

"Risk is concentrated at key strikes on Deribit: largest OI at $80,000 calls (Jul 31), then $80,000 calls (Dec 25), with a notable defensive cluster in $60,000 puts (Dec 25).",

"Most active trading focused on $70,000 calls (Jul 31), while very short-dated Bybit calls ($60,000 and $59,500 expiring Jul 1) point to intraday leverage demand into settlement."

],

"what_it_implies": [

"Medium-term traders are positioned for upside continuation (call-heavy OI), but near-term participants are actively hedging, consistent with elevated uncertainty around expirations.",

"Heavy attention to $70k/$80k calls suggests these levels act as psychological and gamma-relevant targets; $60k puts represent a commonly referenced downside ‘line in the sand.’",

"The combination of slightly falling OI and concentrated activity implies repositioning (rolling strikes/expiries) instead of broad-based risk-on escalation."

]

}

💡 Strategic Points

{

"key_levels_to_watch": [

{

"level": "$70,000",

"why_it_matters": "Most traded contract (Deribit Jul 31 call) suggests high attention and potential dealer-hedging effects near this strike into expiry windows."

},

{

"level": "$80,000",

"why_it_matters": "Top OI concentration (Jul 31 and Dec 25 calls) signals upside targets and potential ‘pinning’/volatility effects as expiration nears."

},

{

"level": "$60,000",

"why_it_matters": "Meaningful put OI (Dec 25) indicates a key hedging strike where downside protection demand is clustered."

}

],

"read_on_positioning": [

"If call OI remains dominant while spot rises, upside moves may accelerate as hedgers adjust; conversely, heavy put usage in daily flow can dampen rallies by keeping protection bid.",

"A near-50/50 volume split often reflects ‘long spot + long puts’ (protective hedges) and/or ‘sell puts / buy calls’ structures—both consistent with managing volatility rather than pure directional conviction.",

"Monitor whether OI starts rising again: increasing OI alongside rising price can indicate fresh leverage entering; rising OI alongside falling price can indicate growing downside positioning."

],

"practical_takeaways": [

"Into expiries, expect higher sensitivity to sharp spot moves around large strikes due to hedging flows.",

"Short-dated call activity (Bybit Jul 1) highlights tactical, event-driven positioning—these trades can unwind quickly after settlement.",

"Sustained put participation in flow suggests traders continue to pay for insurance; abrupt drops in put demand can coincide with complacency and thinner downside protection."

]

}

📘 Glossary

{

"terms": [

{

"term": "Call option",

"definition": "A contract giving the right (not obligation) to buy an asset at a set price (strike) by a certain date; commonly used for bullish exposure."

},

{

"term": "Put option",

"definition": "A contract giving the right (not obligation) to sell an asset at a set strike by a certain date; commonly used for bearish exposure or downside hedging."

},

{

"term": "Open Interest (OI)",

"definition": "The total number (or notional value) of outstanding option contracts that remain open; a measure of accumulated positioning, not just daily trading."

},

{

"term": "Notional trading volume",

"definition": "The dollar value of options traded over a period (e.g., 24 hours), reflecting turnover/flow rather than total outstanding positions."

},

{

"term": "Strike price",

"definition": "The predetermined price at which the option can be exercised (buy for calls, sell for puts)."

},

{

"term": "Expiration (expiry)",

"definition": "The date when an option contract ends; positioning and hedging activity often intensify as this date approaches."

},

{

"term": "Hedging",

"definition": "Using derivatives (like puts/calls) to reduce risk in a spot or perpetual position, often by limiting downside or locking in outcomes."

}

]

}

Comment 0