News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

U.S. crypto markets saw a renewed burst of 'institutional demand' on Thursday, as spot Bitcoin (BTC) and Ethereum (ETH) ETFs posted sizable daily inflows, while regulators and lawmakers signaled potential progress on long-awaited market structure reforms—from crypto 'perpetual futures' to clearer rules for digital-asset oversight.

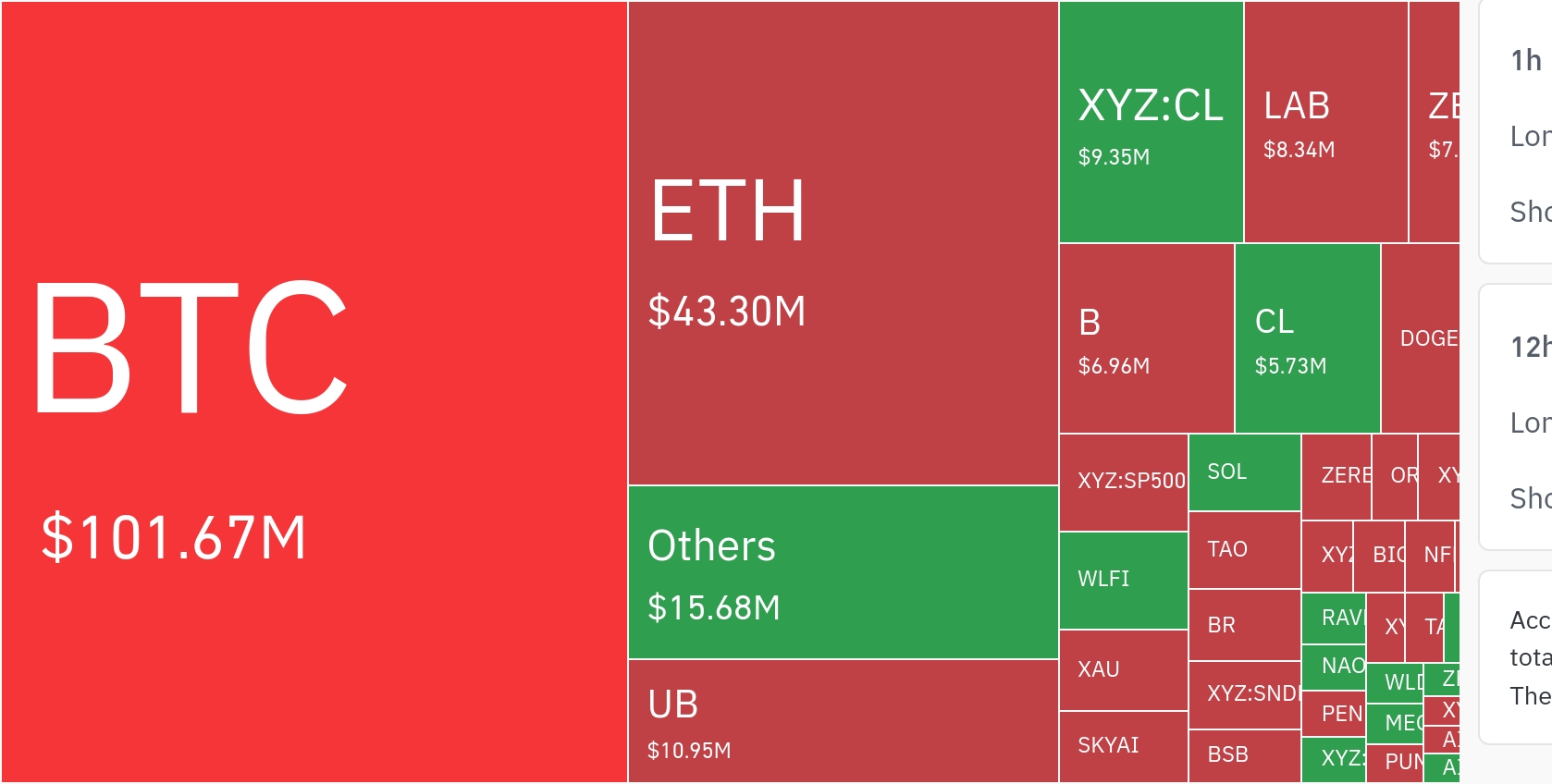

According to data cited by Odaily from SoSoValue, U.S. spot Bitcoin ETFs recorded a combined net inflow of $630 million on May 1 (U.S. Eastern Time). BlackRock’s iShares Bitcoin Trust ($IBIT) led the pack with $284 million in net inflows, followed by Fidelity’s Wise Origin Bitcoin Fund ($FBTC) with $213 million.

SoSoValue data showed cumulative net inflows reaching $32.7 billion for $IBIT and $11.08 billion for $FBTC. Total net assets across U.S. spot Bitcoin ETFs were reported at $103.79 billion, representing about 6.66% of Bitcoin’s total market capitalization, with cumulative net inflows at $58.72 billion.

Spot Ethereum ETFs also attracted fresh allocations. On May 1 ET, the category recorded $101 million in net inflows, led by Fidelity’s Ethereum Fund ($FETH) with $49.39 million. BlackRock’s iShares Ethereum Trust ($ETHA) followed with $43.16 million. Total net assets in U.S. spot Ethereum ETFs stood at $13.60 billion, or roughly 4.93% of Ethereum’s market cap, with cumulative net inflows at $12.02 billion, according to figures cited by Odaily.

Beyond ETF flows, derivatives regulation emerged as a key catalyst. Michael Selig, a commissioner at the U.S. Commodity Futures Trading Commission (CFTC), said in an interview with Anthony Pompliano that 'true crypto perpetual futures' could be legalized in the U.S. within weeks, depending on how the agency finalizes the products’ regulatory classification. Perpetual futures—highly liquid, leveraged contracts without an expiry date—are a cornerstone of offshore crypto trading but have remained constrained in the U.S. due to regulatory uncertainty.

Selig argued the move would replace long-running workarounds with a more formal framework, describing the initiative as a win for both the industry and the U.S. public if properly regulated. Market participants have long viewed onshore availability of regulated perpetuals as a potential boost to 'liquidity inflow' and risk-managed access—though critics warn that broader leverage in retail-facing venues could amplify volatility if guardrails are insufficient.

On the legislative front, White House correspondent Pete Rizzo reported on X that the Bitcoin industry and major U.S. banks have reached a compromise around the CLARITY Act, potentially allowing a broader market structure bill to advance into the congressional markup stage. Markup is the formal process where legislators review and amend bill text, often serving as a key inflection point before committee and floor votes.

Internationally, Taiwan entered the growing conversation around sovereign Bitcoin reserves. WuBlockchain reported that Taiwanese legislator Ko Ju-chun submitted a report to the Executive Yuan and Taiwan’s central bank proposing the use of foreign exchange reserves to establish a Bitcoin reserve. The Bitcoin Policy Institute was cited as pointing to the report as evidence Taiwan could consider Bitcoin as part of its reserve framework, though there was no confirmation that the government or central bank has initiated an official policy review.

Stablecoins drew fresh attention on both issuance and forecasting. Circle minted an additional 250 million USDC on the Solana (SOL) network, according to PANews citing on-chain data—an action typically associated with meeting anticipated settlement and trading demand, though not necessarily a direct signal of immediate market buying pressure.

Separately, JPMorgan projected that stablecoin market capitalization could reach $500 billion to $600 billion by 2028, cautioning against expectations of a near-term $1 trillion market. The bank attributed its conservative view to rising stablecoin 'velocity'—the idea that greater payments usage can increase transaction throughput without requiring proportional growth in total supply outstanding.

In Washington’s regulatory arena, Anchorage Digital said it submitted a comment letter to the Office of the Comptroller of the Currency (OCC) regarding proposed rules tied to the GENIUS Act framework. The firm said it has partnered on three stablecoins—USAT (with Tether), USDGO (with OSL Group), and USDtb (with Ethena)—and plans to co-issue a fourth stablecoin, UDSPT, with Western Union. Anchorage Digital said it expects to become a formally licensed issuer of payment stablecoins once the GENIUS Act regime is implemented.

Geopolitical compliance risks also moved back into focus. The U.S. Treasury’s Office of Foreign Assets Control (OFAC) warned that paying Iran so-called Strait of Hormuz passage fees—whether in fiat currency, digital assets, barter arrangements, in-kind transfers, or donations routed through certain Iranian-linked entities—could constitute a violation of U.S. sanctions and may be treated as support for the Iranian government or the Islamic Revolutionary Guard Corps (IRGC). OFAC emphasized that U.S. persons and U.S.-controlled foreign entities are generally prohibited from transactions involving Iranian government actors, the IRGC, and Iranian digital asset exchanges, while non-U.S. entities could face secondary sanctions and civil or criminal exposure for facilitating restricted activity.

Adding to these concerns, Reuters reported allegations that Nobitex—described as Iran’s largest crypto exchange—may have helped facilitate sanctions evasion by processing transactions linked to Iran’s central bank and the IRGC. Reuters cited blockchain analytics firm Elliptic as estimating that roughly $500 million in crypto moved through Iran’s central bank wallets between November 2024 and June 2025, with about $347 million flowing into Nobitex in the first half of 2025. The report also noted Nobitex’s sizable flows with offshore exchanges, including Binance, and alleged continued service for some whitelisted users during periods of wartime internet restrictions.

The day’s developments underscored a market increasingly shaped by policy—where ETF flows reflect mainstream access, stablecoins power settlement rails, and regulatory decisions on leverage and market structure could determine how much activity migrates onshore. With Washington weighing framework bills and the CFTC signaling movement on perpetuals, traders are watching for whether clearer rules translate into deeper U.S.-based liquidity—or simply reprice risk across global venues.

🔎 Market Interpretation

- Institutional bid reasserts via ETFs: U.S. spot Bitcoin ETFs logged $630M net inflow (May 1 ET), while spot Ethereum ETFs added $101M—signaling renewed risk appetite through regulated wrappers rather than offshore venues.

- Concentration of flows highlights “benchmark” products: BTC inflows were led by BlackRock IBIT (+$284M) and Fidelity FBTC (+$213M); ETH flows were led by Fidelity FETH (+$49.39M) and BlackRock ETHA (+$43.16M).

- ETF footprint is now material vs. underlying caps: Total U.S. spot BTC ETF assets reached $103.79B (~6.66% of BTC market cap); spot ETH ETF assets reached $13.60B (~4.93% of ETH market cap)—levels that can influence spot liquidity, intraday flows, and basis dynamics.

- Regulatory optionality becomes a volatility driver: The CFTC signaling possible legalization of “true” crypto perpetual futures in weeks introduces a major catalyst for onshore leveraged trading—potentially deepening U.S. liquidity while increasing sensitivity to leverage-related liquidations if safeguards are weak.

- Market-structure legislation inches forward: A reported compromise on the CLARITY Act (industry + major U.S. banks) suggests improved odds of a broader framework reaching markup, which markets may interpret as reduced long-term policy uncertainty.

- Stablecoins: supply expansion + tempered growth outlook: Circle minted 250M USDC on Solana (often tied to anticipated settlement/trading needs). JPMorgan projects $500B–$600B stablecoin market cap by 2028 (below $1T), citing higher velocity meaning more payment throughput without proportional supply growth.

- Compliance/geopolitics reprice counterparty risk: OFAC warnings around Iran-related payments and Reuters allegations concerning Nobitex amplify sanctions exposure concerns—potentially affecting exchange flows, stablecoin rails, and cross-border liquidity.

💡 Strategic Points

- Watch ETF flow persistence, not one-day prints: Sustained BTC/ETH ETF inflows tend to support spot demand and reduce sell-side pressure; reversals can quickly tighten liquidity and widen spreads.

- Track policy catalysts as “macro” for crypto: (1) CFTC classification decisions for perpetuals, (2) congressional markup progress on CLARITY/market structure, and (3) OCC/GENIUS Act stablecoin rulemaking could each shift where volume concentrates (onshore vs offshore) and how risk is priced.

- Perpetual futures legalization could reshape venue share: If U.S.-regulated perps launch, expect migration of some leverage demand from offshore exchanges, potentially improving transparency—while also increasing competition for centralized exchanges and broker platforms.

- Risk management implication of broader leverage: More accessible perps can increase liquidation cascades during sharp moves; traders should monitor funding rate dynamics, margin requirements, and any retail-facing guardrails.

- Stablecoin issuance is a “plumbing” signal: USDC minting on Solana may reflect anticipated settlement demand (market-making, exchange inventory, payments). It is not a clean proxy for immediate directional buying, but it can precede higher on-chain activity.

- Velocity thesis matters for long-run valuations: If stablecoin velocity rises, network/payment utilization can grow faster than total stablecoin supply—supporting usage narratives while limiting market-cap-based “TAM” assumptions.

- Sanctions diligence becomes a trading edge: Heightened OFAC scrutiny increases the importance of counterparties, wallet screening, and exposure mapping (exchanges, market makers, bridges). Compliance shocks can cause abrupt liquidity fragmentation.

- Sovereign reserve discussions are sentiment catalysts, not policy yet: Taiwan’s proposed Bitcoin reserve is exploratory; markets should treat it as narrative support unless confirmed by official review or allocation.

📘 Glossary

- Spot ETF: An exchange-traded fund that holds the underlying asset (e.g., BTC/ETH) rather than futures, providing regulated access via brokerage accounts.

- Net inflow: The day’s creations minus redemptions for an ETF; a positive number implies more capital entering than leaving.

- Total net assets (AUM): The market value of assets held by the ETF(s); often used to gauge product scale and market influence.

- Perpetual futures (“perps”): Leveraged derivatives with no expiry date; they use periodic funding payments to keep prices near spot.

- Funding rate: A periodic payment between long and short perp traders; positive funding generally means longs pay shorts (bullish positioning).

- Market structure reform: Regulatory/law changes defining who oversees which crypto assets, how trading venues operate, and investor protection rules.

- Markup: The stage where a congressional committee debates, amends, and votes on a bill’s text before it can advance further.

- Stablecoin velocity: How frequently stablecoins circulate/are used in transactions; higher velocity can increase economic throughput without requiring more supply outstanding.

- OCC (Office of the Comptroller of the Currency): U.S. regulator overseeing national banks; relevant for custody, banking rails, and stablecoin/payment token frameworks.

- OFAC: U.S. Treasury office administering sanctions; violations can create civil/criminal liability and secondary sanctions risk.

- Secondary sanctions: Penalties applied to non-U.S. entities for engaging in certain sanctioned activities, potentially restricting their access to U.S. markets/financial system.

Comment 0