News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

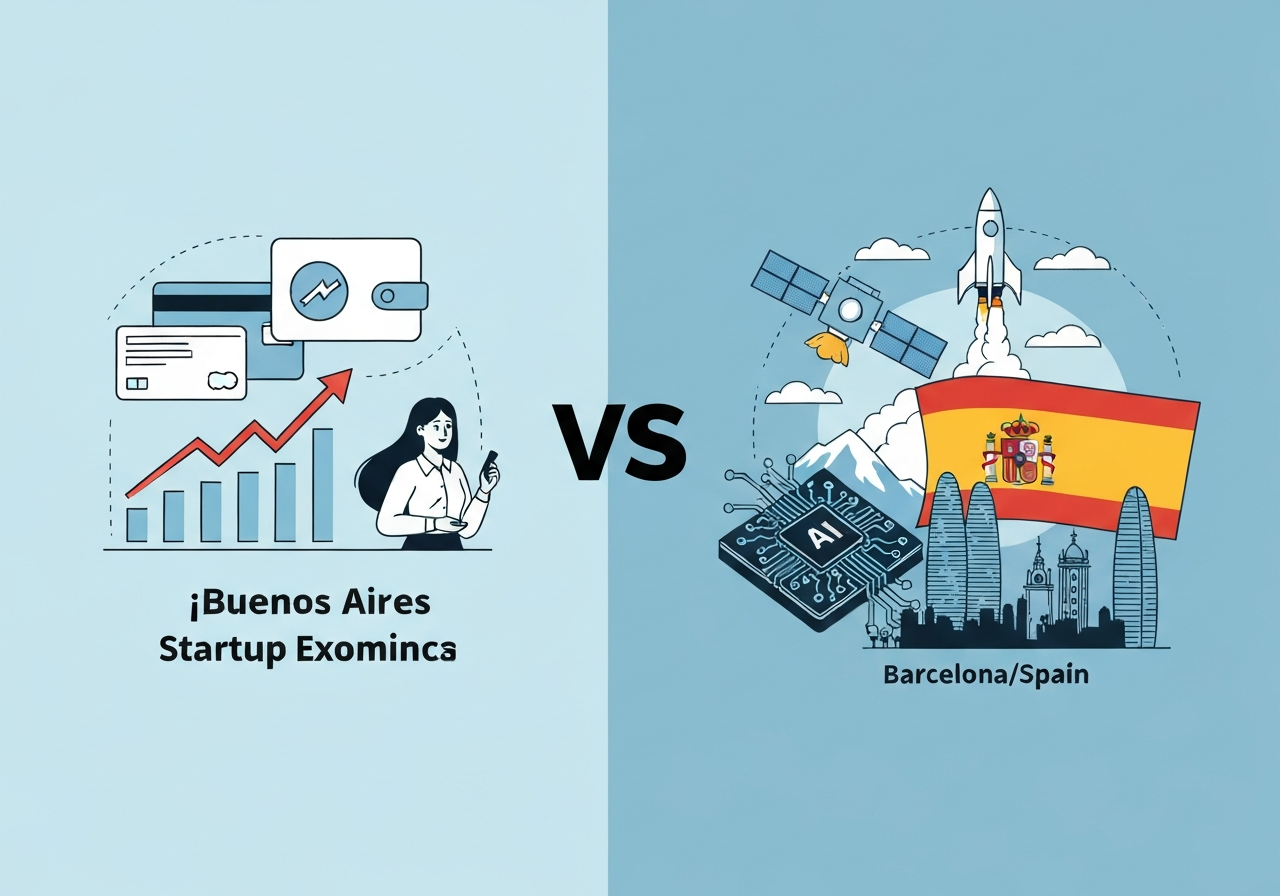

Spain and Argentina may be household names on the football pitch, but in the global race for venture capital they remain relative ‘underdogs’—even as recent funding rounds suggest both ecosystems are sharpening distinct competitive edges. For global investors tracking where the next wave of ‘liquidity inflow’ could emerge outside the usual hubs, the latest deal flow points to Argentina’s fintech resilience and Spain’s growing footprint in space and AI.

Both countries still account for a modest share of worldwide startup funding, particularly as the current AI-driven cycle continues to concentrate capital in Silicon Valley and a handful of dominant innovation centers. Yet 2026 has brought a clearer signal: Argentina is leaning into financial infrastructure and consumer fintech, while Spain is building momentum around aerospace ambitions and enterprise AI.

Argentina: a ‘small but durable’ fintech engine

Argentina’s venture market remains smaller than regional heavyweights such as Brazil and Mexico, typically attracting only several hundred million dollars annually. Still, it has repeatedly produced outsized success stories—an important indicator in markets where high volatility and macro uncertainty often discourage long-duration risk capital.

The most emblematic example is MercadoLibre ($MELI), the Latin American e-commerce and fintech giant that began as a garage startup in Buenos Aires and is now headquartered in Uruguay. The Nasdaq-listed company’s market capitalization stands at roughly $94 billion, underscoring Argentina’s ability to generate globally scaled outcomes despite limited domestic funding depth.

Recent attention has centered on Buenos Aires-based fintech Ualá, which has raised a total of $1.1 billion to date. In March alone, the company secured $195 million, reinforcing a broader pattern in 2026: the largest Argentine rounds continue to cluster around payments, collections, and embedded finance infrastructure.

Payment infrastructure startup Pomelo raised $55 million in its Series C, co-led by Kaszek and Insight Partners, while payments and collection infrastructure firm Tapi brought in $27 million in a February Series B. Market participants note that Argentina’s annual totals can swing sharply depending on whether one or two mega-rounds land in a given year—yet 2026 funding is already tracking above last year’s full-year performance, highlighting renewed investor willingness to back category leaders.

Spain: smaller totals, bigger bets on space and AI

Spain’s startup funding remains behind larger European peers. In 2026 to date, Spanish startups have raised less than $2 billion across stages—roughly one-third of France’s total over the same period. However, the country’s pipeline appears increasingly defined by sector specialization rather than sheer volume.

The year’s largest round went to PLD Space, a space company that raised $206 million in a March Series C. The company has positioned itself as a ‘global space transportation service provider’ supporting missions tied to lunar and Martian exploration, aligning Spain’s venture narrative with broader global interest in sovereign launch capabilities and commercial space logistics.

Barcelona-based Factorial, an AI-enabled HR and payroll management platform, also secured a major financing in June—raising $150 million in a Series D at a reported $2.5 billion valuation. The company’s cumulative equity funding now exceeds $350 million, illustrating growing investor appetite for enterprise software platforms that can scale beyond domestic markets.

Madrid-based firms have added to the momentum. EOS-X Space, focused on near-space infrastructure, space tourism, and aerospace data, raised $140 million in a May Series D. Meanwhile, Zummit—an AI tools developer for geospatial data analysis—closed a $130 million Series B in April, reflecting continued demand for applied AI in mapping, climate, and infrastructure intelligence.

Over the past several years, total annual venture investment in Spain has generally ranged between $1.8 billion and $2.8 billion. With 2026 deal activity expanding, analysts expect the country could close the year with a stronger showing than 2025, even if it remains a secondary market compared with the continent’s largest hubs.

Underdogs with distinct identities

Despite their cultural prominence and deep talent pools, Spain and Argentina remain outside the top tier of venture destinations. The macro backdrop is not especially favorable: global capital has become more selective, and the AI cycle has intensified winner-takes-most dynamics that funnel funding toward established ecosystems.

Still, the latest funding patterns suggest each market is developing a clearer identity—Argentina as a fintech proving ground, Spain as an emerging European node for ‘space commercialization’ and applied AI. If global venture capital broadens its geographic aperture in coming quarters, both ecosystems could benefit disproportionately, supported by visible success cases and increasingly mature founders.

Ultimately, recent activity underscores a familiar venture truth: scale matters, but focus matters too. In markets where the pool of capital is smaller, the ability to concentrate resources on a few defensible sectors—and produce repeatable breakout outcomes—can become the foundation for the next phase of growth.

Comment 0