News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

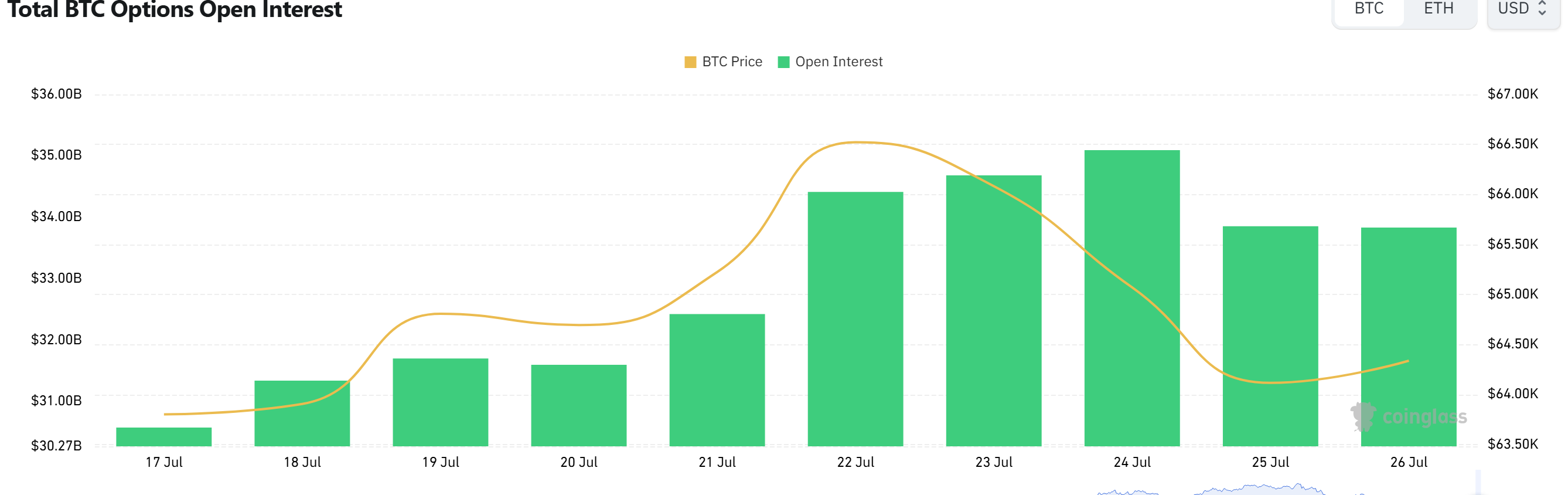

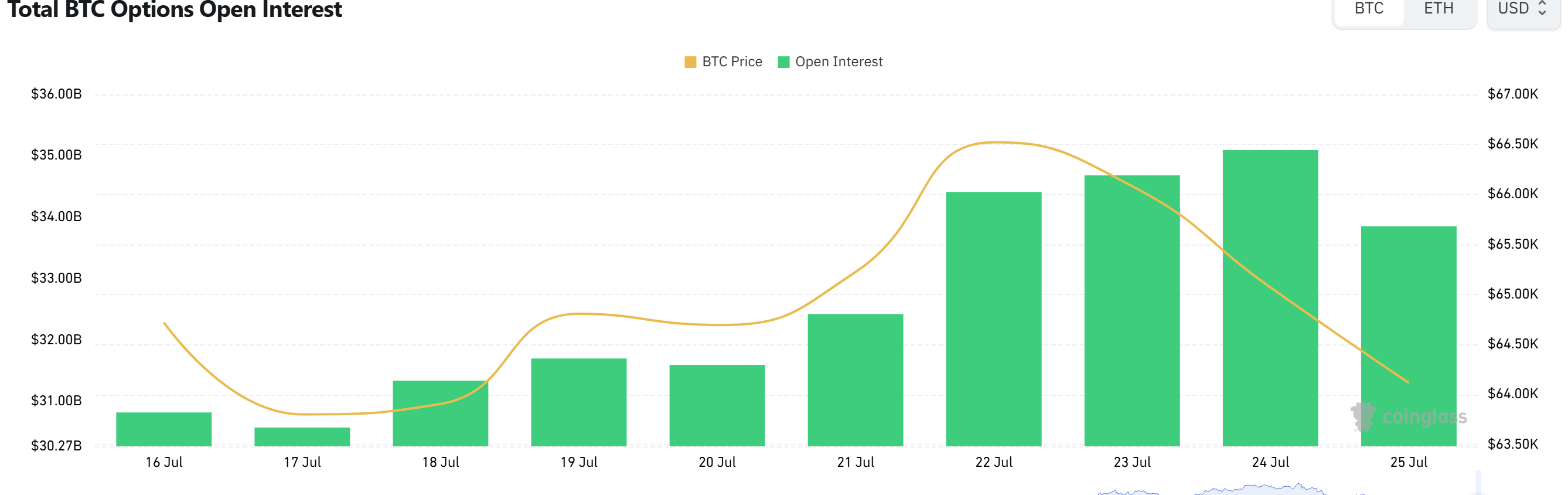

Bitcoin (BTC) options 'open interest' has fallen sharply in recent days, signaling a notable cooling in outstanding leveraged positioning even as the market’s longer-dated bias remains tilted toward calls. At the same time, put options have climbed to the top of the volume rankings, suggesting traders are increasingly paying for near-term downside protection.

As of Sunday 01:00 ET (05:00 UTC), data compiled by Coinglass showed total BTC options open interest at $32.64 billion. While that marked a 1.78% increase from the prior day’s $32.07 billion, open interest has remained materially lower since Friday, pointing to recent position unwinds or expiries removing risk from the system.

In terms of positioning, calls still accounted for the majority of outstanding contracts at 57.58%, versus 42.42% for puts—an imbalance commonly interpreted as a market that is still structurally oriented toward upside exposure. However, the flow picture has turned more defensive. Total options trading volume over the past 24 hours was about $1.65 billion, with puts narrowly leading at 50.33% versus calls at 49.67%.

Exchange-by-exchange volume data highlighted where activity is concentrating. Deribit led with roughly $631 million, followed by Bybit at about $477 million, Binance at about $250 million, OKX at approximately $203 million, and CME at roughly $44 million. The dominance of offshore crypto venues—particularly Deribit—underscored that much of the hedging and speculative flow continues to occur in the derivatives-native ecosystem rather than in traditional markets.

The largest open-interest clusters remained in higher-strike calls, reinforcing the idea that longer-horizon positioning is still skewed toward upside scenarios. The top contracts by open interest were the $80,000 call expiring May 29 on Deribit, the $120,000 call expiring Dec. 25 on Deribit, and the $90,000 call expiring June 26 on Deribit.

Yet the most actively traded contracts over the past 24 hours told a different story about immediate sentiment. The leading contract by volume was the $60,000 put expiring June 26 on Deribit, followed by the $88,000 call expiring June 26 on Deribit. The third-ranked contract was the $77,500 put expiring Sunday on Bybit. Market participants often interpret heavy put volume at a widely watched strike—such as $60,000—as evidence of heightened demand for 'short-term hedging' around a key psychological level.

Options are derivatives that allow traders to take leveraged views on price direction or hedge existing spot and futures exposure. A 'call option' gives the right (but not the obligation) to buy the underlying asset at a preset price by a certain date, while a 'put option' provides the right to sell at a preset price. 'Open interest' represents the total number of outstanding contracts still open in the market, offering a window into how much risk capital remains positioned across expiries and strike prices.

With open interest having reset lower since Friday but put volumes rising to match—and slightly surpass—calls, the data points to a market that is reducing overall leverage while simultaneously paying closer attention to downside risk. How long that defensive tone persists may depend on whether BTC can hold key support levels without triggering another wave of hedging-driven demand for puts.

🔎 Market Interpretation

- Leverage is coming off: BTC options open interest sits at $32.64B, up slightly day-over-day but materially lower since Friday, implying position unwinds and/or expiries reduced outstanding risk.

- Structure still bullish, flow turns defensive: Outstanding positioning remains call-heavy (57.58%) versus puts (42.42%), but the latest 24H volume is put-led (50.33%), signaling near-term demand for protection.

- Hedging focus near key levels: The most-traded contract was the $60,000 put (Jun 26, Deribit), suggesting traders are actively insuring against a dip around a widely watched psychological/support zone.

- Offshore venues dominate price-risk transfer: Most activity is concentrated on crypto-native derivatives exchanges, led by Deribit (~$631M), indicating hedging/speculation remains driven primarily by offshore liquidity rather than traditional venues like CME (~$44M).

- Longer-dated upside bets still visible: The largest open-interest clusters remain in higher-strike calls (e.g., $80K May 29, $90K Jun 26, $120K Dec 25), reflecting continued longer-horizon upside optionality despite near-term caution.

💡 Strategic Points

- Read OI + volume together: Falling open interest alongside rising put volume often implies de-risking while simultaneously buying near-term hedges—a shift from “risk-on” to “protect capital.”

- Watch $60K as a hedging magnet: Elevated trading in the $60K put can amplify moves if spot approaches that level (gamma/hedging effects), potentially increasing short-term volatility.

- Differentiate time horizons: Strong call open interest at higher strikes can coexist with short-term put demand—interpretable as long-term bullishness paired with near-term uncertainty.

- Monitor expiry/roll behavior: If put-heavy volume persists into upcoming expiries (e.g., Jun 26) and open interest rebuilds, it would confirm a more sustained defensive stance; if put buying fades, it may indicate the hedge wave is temporary.

- Follow venue signals: Deribit leadership suggests institutional/large-derivatives traders are active; an increase in CME share would hint at greater traditional finance participation in the hedging cycle.

📘 Glossary

- Options Open Interest (OI): The total number (or notional value) of option contracts that remain outstanding (not closed or expired). Often used as a proxy for how much risk is currently positioned.

- Call Option: A contract giving the buyer the right (not obligation) to buy the asset at a specified strike price before/on an expiry. Typically benefits from upside moves.

- Put Option: A contract giving the buyer the right (not obligation) to sell the asset at a specified strike before/on expiry. Commonly used for downside protection.

- Strike Price: The preset price at which the option can be exercised (e.g., $60,000, $80,000).

- Expiry (Expiration Date): The date after which the option ceases to exist (e.g., May 29, Jun 26, Dec 25).

- Volume: The amount of options traded over a period (e.g., last 24 hours). High put volume can indicate increased hedging demand.

- Hedging: Using derivatives (often puts) to reduce portfolio downside risk, especially around key support levels.

- Derivatives-native venues: Exchanges primarily focused on derivatives trading (e.g., Deribit), often leading in options liquidity compared with traditional venues (e.g., CME).

Comment 0