News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

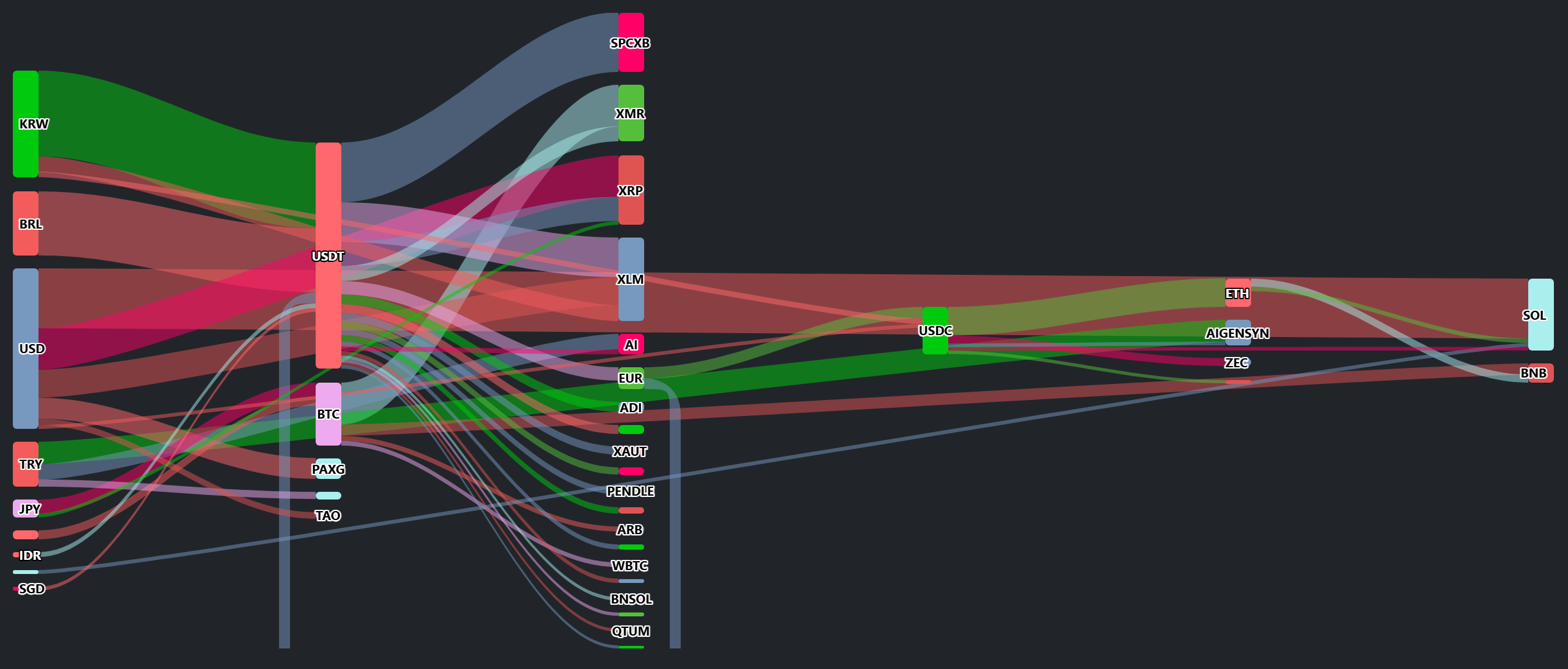

Ripple has cemented a $50 billion valuation after completing a $750 million share buyback, reaffirming its commitment to remain private and signaling it has no near-term plans for an initial public offering. The move lands at an awkward moment for token markets: XRP (XRP) fell 23.7% in the first quarter, intensifying a long-running debate over whether Ripple’s expanding business lines can meaningfully translate into value for XRP holders.

As of Tuesday ET, XRP was trading around $1.32, keeping its position as the No. 5 cryptocurrency by market capitalization at roughly $81.2 billion. Spot turnover rose 18.3% over the past 24 hours to about $1.8 billion, but the token remains down 29.2% over the past 90 days and more than 40% below its cycle high, underscoring the gap between improving corporate fundamentals at Ripple and subdued price momentum in the token.

Ripple said it delivered its “best-ever” performance in the first quarter of 2026, driven in part by the ramp-up of businesses it has acquired over the past year. Revenue tied to prime brokerage activities at Hidden Road—purchased for $1.25 billion—reportedly tripled, supported by a client base of more than 300 institutional customers processing an estimated $3 trillion in annual volume. Meanwhile, GTreasury, acquired for $1 billion, has become a corporate treasury workflow product capable of moving funds within a minute for Fortune 500 clients, and Ripple said total payment volumes on its rails have exceeded $100 billion.

For equity holders, the buyback and valuation mark provide clarity on corporate value. For XRP holders, the same developments rekindle concerns about 'decoupling'—the idea that Ripple’s business growth does not automatically create incremental demand for XRP. Many of Ripple’s fastest-growing units can operate without integrating the token directly, leaving markets to question how much of Ripple’s enterprise expansion actually accrues to XRP’s utility and price.

That tension is most visible in stablecoins. Ripple USD (RLUSD) has grown to a market capitalization of roughly $1.56 billion, with about 88% of supply issued on Ethereum (ETH). Ripple has positioned RLUSD as a settlement and liquidity tool for institutions, and the asset has reportedly been used in payment contexts by major financial players including Deutsche Bank, Aviva Investors, and Société Générale. However, market participants increasingly note that many institutional flows appear to prefer direct fiat-to-RLUSD settlement paths—effectively bypassing XRP—raising the possibility that successful RLUSD adoption could dilute, rather than amplify, XRP demand.

In a sign that major banks are taking a more measured view of near-term token performance, Standard Chartered analyst Geoffrey Kendrick cut his 2026 year-end price target for XRP to $2.80 from $8, a 65% reduction. Kendrick cited slower-than-expected recovery after XRP’s dip to $1.16 in February. He maintained longer-dated targets—$12.60 by the end of 2028 and $28 by 2030—but framed the near-term outlook as constrained by limited catalysts and muted follow-through from recent rallies.

XRP briefly climbed to the $1.35–$1.36 area on upbeat remarks from CEO Brad Garlinghouse and renewed speculation around exchange-traded products, before slipping back into a familiar $1.30–$1.50 range. In the U.S., seven spot XRP ETFs have attracted about $1.32 billion in cumulative inflows, though weekly inflows have slowed to roughly $2 million. Grayscale is in the process of converting a roughly $2.1 billion trust into a spot ETF structure, while Franklin Templeton has entered the field with a low 0.15% fee, adding competitive pressure to the category.

Regulatory signals have also improved. The Securities and Exchange Commission and the Commodity Futures Trading Commission have reportedly leaned toward treating XRP as a digital 'commodity', an interpretation that market participants view as helpful for reducing compliance uncertainty. Still, clarity alone has not been enough to pull XRP out of its range, as traders look for evidence that regulation will translate into real, token-linked transaction demand.

Ripple CTO David Schwartz revisited a long-running argument from 2017, asserting that a higher XRP price can reduce costs for payment utility—countering the claim that a low token price is inherently better for network usage. The point is closely tied to Ripple’s On-Demand Liquidity (ODL) model, which uses XRP as a potential bridge asset for cross-border settlement. Yet skeptics note a persistent mismatch between theoretical token utility and current product deployment: key revenue drivers such as Hidden Road and GTreasury can scale without meaningfully routing activity through XRP.

Garlinghouse has said he expects the U.S. 'Clarity Act' to pass by late May, after an earlier timeline pointing to April slipped. Supporters argue that, if enacted, the legislation could give U.S. banks a clearer framework for stablecoin activity and potentially open the door for broader ODL adoption—an outcome that could strengthen XRP’s role in cross-border settlement markets. Whether banks will choose XRP-based paths over fiat-stablecoin routes remains the central question.

Ripple’s decision to lock in its valuation through a buyback while forgoing an IPO offers corporate stability and liquidity to shareholders, but it is a 'double-edged sword' for token investors. The stronger Ripple’s private-market business becomes without corresponding XRP integration, the more pronounced the narrative risk that the company’s success and the token’s price can move independently. For now, the market’s focus is split between near-term technical levels around the $1.30–$1.50 band and longer-term catalysts, including regulatory follow-through and the evolution of ETF flows. The durability of the Ripple-XRP disconnect—and whether regulatory clarity converts into sustained token-linked demand—looks set to define XRP sentiment into the second half of 2026.

🔎 Market Interpretation

- Ripple locks in private-market value: A $750M share buyback implies a ~$50B valuation, reinforcing Ripple’s intent to remain private and removing an IPO as a near-term catalyst.

- XRP lags despite stronger corporate fundamentals: XRP is ~No.5 by market cap (~$81.2B) but remains down sharply (Q1 -23.7%, ~90D -29.2%) and well below cycle highs, highlighting weak price momentum versus Ripple’s business growth.

- “Decoupling” narrative intensifies: Markets are increasingly questioning whether Ripple’s expanding revenue lines (Hidden Road, GTreasury, payments rails) create direct, incremental demand for XRP.

- Stablecoin success may bypass XRP: RLUSD (~$1.56B market cap) is mostly issued on Ethereum (~88%), and institutional settlement flows may favor fiat↔RLUSD routes, potentially reducing the need for XRP as an intermediary.

- ETFs and regulation help sentiment, not breakout: Spot XRP ETF inflows (~$1.32B cumulative) have slowed (~$2M weekly). Regulators leaning toward a “commodity” framing reduces uncertainty, but traders still want proof of token-linked demand.

- Near-term range persists, catalysts debated: XRP continues to trade around the $1.30–$1.50 band, with focus on whether legislation ("Clarity Act") and product adoption translate into sustained XRP usage.

💡 Strategic Points

- Track “usage routing,” not just Ripple growth: Monitor whether ODL corridors and institutional payment flows are actually settled via XRP versus stablecoins/fiat, as this determines whether Ripple’s success accrues to token demand.

- RLUSD distribution is a key leading indicator: Watch chain mix (Ethereum vs XRPL), issuance/redemption patterns, and major treasury/payment integrations—rising RLUSD adoption could be bullish for Ripple’s enterprise footprint but neutral/bearish for XRP if XRP is not part of the path.

- ETF flows are supportive but insufficient alone: Slowing inflows suggest marginal demand is fading; competition (e.g., low-fee entrants) and large conversions (e.g., trust-to-ETF) may affect short-term supply/demand dynamics.

- Regulatory clarity is necessary, not sufficient: A “commodity” interpretation and potential U.S. legislation may enable banks to engage, but the decisive factor is whether institutions choose XRP as a bridge asset rather than stablecoin-only settlement.

- Valuation buyback is double-edged for token holders: A stronger private Ripple without deeper XRP integration can strengthen the decoupling thesis, increasing narrative risk and keeping XRP tied to technical levels and catalyst timing.

- Price-level framework: The $1.30–$1.50 range remains the market’s reference band; a durable breakout likely requires evidence of sustained, token-linked transaction throughput, not only corporate announcements.

📘 Glossary

- Share buyback: A company repurchasing its own shares, often to provide liquidity to shareholders and signal confidence, which can also anchor a private-market valuation.

- IPO (Initial Public Offering): When a private company lists shares on a public exchange. Ripple signaling “no near-term IPO” removes a traditional valuation catalyst.

- Decoupling (Ripple vs XRP): The view that Ripple’s business performance and XRP’s token price/utility can diverge if products scale without using XRP.

- Prime brokerage: Services (financing, custody, execution, clearing) provided to institutional traders; in this context tied to Hidden Road’s business and volumes.

- Stablecoin: A token designed to track a stable value (typically USD). RLUSD is Ripple’s USD-pegged stablecoin used for settlement/liquidity.

- ODL (On-Demand Liquidity): Ripple’s model for cross-border settlement that can use XRP as a bridge asset to reduce friction and pre-funded accounts.

- Spot ETF: An exchange-traded fund that holds the underlying asset directly; inflows/outflows can affect real-time demand for the asset.

- Trust-to-ETF conversion: Restructuring a trust product into an ETF format, often changing fees, creation/redemption mechanics, and market impact.

- Commodity (digital commodity framing): A regulatory classification implying oversight and compliance expectations closer to commodities than securities, potentially reducing legal uncertainty.

Comment 0