News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Crypto venture funding cooled sharply in the fourth week of April, as the market shifted from headline-grabbing mega-rounds to smaller early-stage checks—an abrupt slowdown that underscores how quickly risk appetite can fade in the current macro and regulatory backdrop.

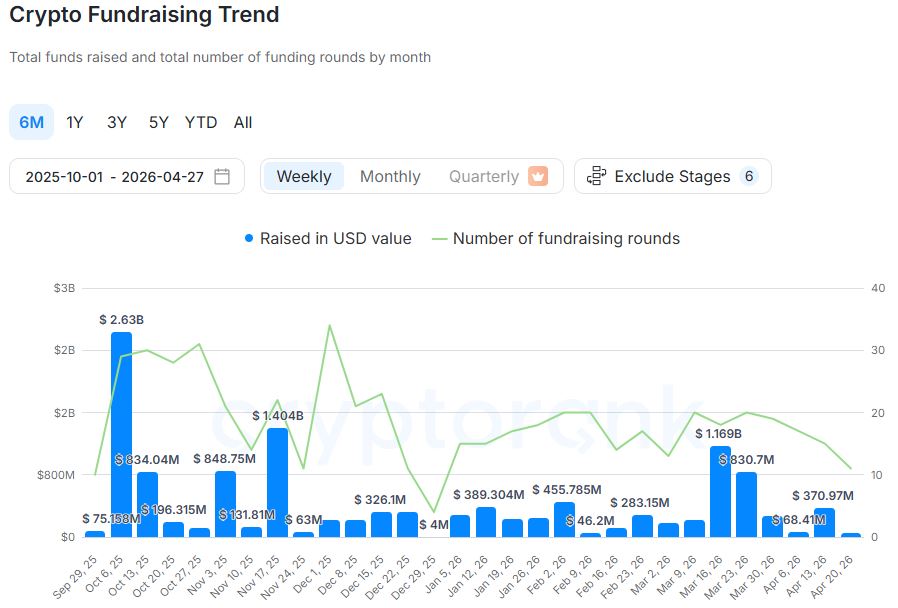

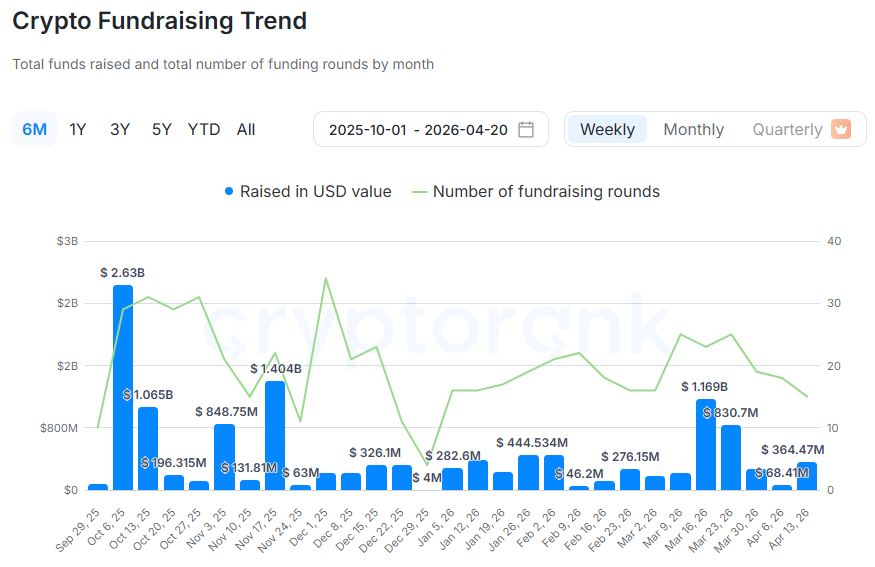

Data compiled by CryptoRank shows that between April 20 and April 26, crypto and blockchain startups raised about $51.98 million across 11 funding rounds. That marked an 86% week-over-week drop from the prior week (April 13–19), when 15 rounds brought in roughly $370.97 million. The decline reflects both fewer deals and, more importantly, the absence of large late-stage raises that had recently propped up aggregate totals.

Among the week’s most notable transactions were several mid-sized rounds. Hata raised $8 million in a Series A led by Bybit, while KAIO secured $8 million in a strategic round backed by multiple investors including Further Ventures. On April 22, BetHog announced a $10 million Series A involving RockawayX and other participants, while Valour disclosed an $11 million funding round with terms not publicly detailed. Earlier-stage deals continued to dominate: ILITY raised $2 million in a strategic round joined by Animoca Brands, Cluster Protocol collected $5 million in an undisclosed round backed by dao5, and 3F raised $4 million in a seed round involving Maven 11 Capital and others. Additional smaller transactions included RealGO’s $3.5 million round with participation from Animoca Brands and Robin Market’s $475,000 angel round involving Fabric Ventures and others.

The weekly pullback fits a broader deceleration in activity seen over the past month. CryptoRank’s 30-day investment activity index fell 43% month-over-month to a 'Low' level, signaling reduced deal velocity and softer capital inflows. Over that same 30-day window, 69 funding rounds were recorded—down 33.6% from the prior month—while total capital raised slid to around $2 billion, a 72.9% decline.

Despite the weaker headline numbers, the underlying pattern suggests a market still funding experimentation, particularly at the seed stage, while reserving larger allocations until valuations, revenue visibility, and regulatory clarity improve. Average round sizes over the period were largely clustered in the $3 million to $10 million range, highlighting how investors are concentrating on smaller, risk-contained bets rather than scale-stage expansion.

On a month-by-month basis, the first quarter showed uneven momentum: January logged 66 rounds totaling $1.14 billion, February saw 70 rounds bringing in $894.34 million, and March surged to 84 rounds with $2.6 billion raised. In April through April 26, 50 rounds had been recorded for $555.26 million—suggesting a more subdued finish to the month unless a major late-stage raise lands after the reporting window.

Sector allocation data points to where capital remains most resilient. Over the past six months, 'payments' accounted for 33.48% of funding share, making it the largest category by a wide margin. Decentralized exchanges (DEX) followed at 20.54%, with real-world assets (RWA) at 19.2%. Lending and API-focused infrastructure each represented 13.39%, reflecting continued interest in the rails that support on-chain finance rather than purely speculative applications.

Investor participation rankings over the same period were led by Coinbase Ventures with 27 deals, followed by GSR and Animoca Brands with 16 deals each. Tether was involved in 15 deals, while Castrum Capital recorded 13. YZi Labs participated in 11, and a16z Crypto logged 10—a lineup that suggests both exchange-linked capital and specialized crypto investment firms remain active even as overall deployment slows.

With deal sizes compressing and fewer large rounds closing, the latest data reinforces a cautious market posture: founders can still raise, particularly in areas tied to 'real-world utility' and financial infrastructure, but the bar for larger checks appears higher—and the funding cycle looks increasingly sensitive to broader liquidity conditions.

🔎 Market Interpretation

- Venture funding whiplash: Weekly crypto startup funding fell to $51.98M across 11 rounds (Apr 20–26), an 86% WoW drop from $370.97M across 15 rounds (Apr 13–19), largely due to the absence of late-stage mega-rounds.

- Risk appetite is narrowing, not disappearing: Capital is still flowing, but primarily into seed and smaller strategic rounds, indicating investors are prioritizing optionality over aggressive scaling.

- Broader downshift confirmed: CryptoRank’s 30-day investment activity index fell 43% MoM to “Low,” with 69 rounds (down 33.6%) and about $2B raised (down 72.9%).

- Round-size compression: Average checks clustered around $3M–$10M, signaling investors want risk-contained bets amid macro and regulatory uncertainty.

- April tracking weaker vs Q1: Through Apr 26, April recorded 50 rounds / $555.26M, implying a subdued month-end unless a large late-stage deal closes after the window.

- Where money still concentrates: Over 6 months, funding share is led by Payments (33.48%), then DEX (20.54%), RWA (19.2%), with Lending and API/infra at 13.39% each—pointing to preference for financial infrastructure and utility.

- Active investors remain engaged: Deal activity leaders include Coinbase Ventures (27), GSR (16), Animoca Brands (16), Tether (15), Castrum (13), YZi Labs (11), and a16z Crypto (10), suggesting platform-linked capital continues deploying even in a slower tape.

💡 Strategic Points

- For founders: optimize for “fundable proof,” not hype. Expect stronger emphasis on revenue visibility, unit economics, and clear paths to compliance before larger checks reappear.

- Seed remains the highest-probability lane: With investors clustering in $3M–$10M rounds, teams should structure raises as milestone-based (e.g., launch, traction, licensing, integrations) rather than valuation-maximizing.

- Positioning that matches capital resilience: Projects in payments rails, DEX infrastructure, RWA tokenization, lending primitives, and API/infra are better aligned with where capital is still allocating.

- Plan for funding cyclicality: The week-to-week variance shows aggregate totals can be skewed by a few late-stage rounds; operational planning should assume longer timelines and smaller tranches.

- Investor mapping matters more than ever: Given the active roster (exchange-affiliated and specialist funds), founders should tailor outreach by category fit (payments/infra/RWA) and demonstrate distribution advantages (integrations, institutional partners, compliance readiness).

- Interpretation for markets: Lower venture throughput can reduce near-term “narrative funding momentum,” but sustained seed activity suggests continued experimentation and a pipeline for future product cycles once liquidity/regulatory conditions improve.

📘 Glossary

- Funding round: A formal capital raise (e.g., seed, Series A) where investors provide funds in exchange for equity/tokens.

- Seed round: Early-stage financing aimed at building an initial product and proving demand/traction.

- Series A: A growth-oriented round typically used to scale a proven product with early traction.

- Strategic round: Investment often led by partners (exchanges, corporates, funds) that can provide distribution, liquidity, or infrastructure support.

- Late-stage/Mega-round: Large financings that meaningfully lift weekly/monthly totals; their absence can make funding appear to “collapse” even if early-stage activity persists.

- DEX (Decentralized Exchange): An on-chain trading venue that matches trades via smart contracts rather than a centralized operator.

- RWA (Real-World Assets): Tokenized representations of off-chain assets (e.g., treasuries, credit, real estate) used in on-chain finance.

- API/Infrastructure: Developer tooling and backend services that power wallets, compliance, data, and on-chain integrations.

- Deal velocity: The pace at which investment rounds are being completed over a period of time.

- Round-size compression: A shift toward smaller average check sizes, reflecting reduced risk tolerance and tighter underwriting.

- Macro backdrop: Broader economic conditions (rates, liquidity, risk sentiment) that influence investment behavior.

- Regulatory clarity: Predictability of legal rules for tokens, exchanges, custody, and compliance—often critical for larger institutional allocations.

Comment 0