News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

Cryptocurrencies extended their rebound over the past week, but the recovery came with a twist: trading activity and volatility fell rather than surged. A new report from Crypto.com said the divergence points to a market that is regaining risk appetite while remaining selective—an environment where prices can rise on thinner participation, and where the next quarter’s direction may be dictated less by momentum and more by 'regulation', 'institutional flows', and the fast-evolving 'stablecoin' and tokenization landscape.

Crypto.com’s latest weekly market read showed its crypto price index gain 6.41% over the week, even as spot trading volume dropped 4.26% and volatility slid 15.76%. In the report’s framing, that mix suggests the market is moving out of a reflexive, overheated phase and into a more stable recovery—one that increasingly depends on macro conditions and policy developments rather than headline-driven speculation.

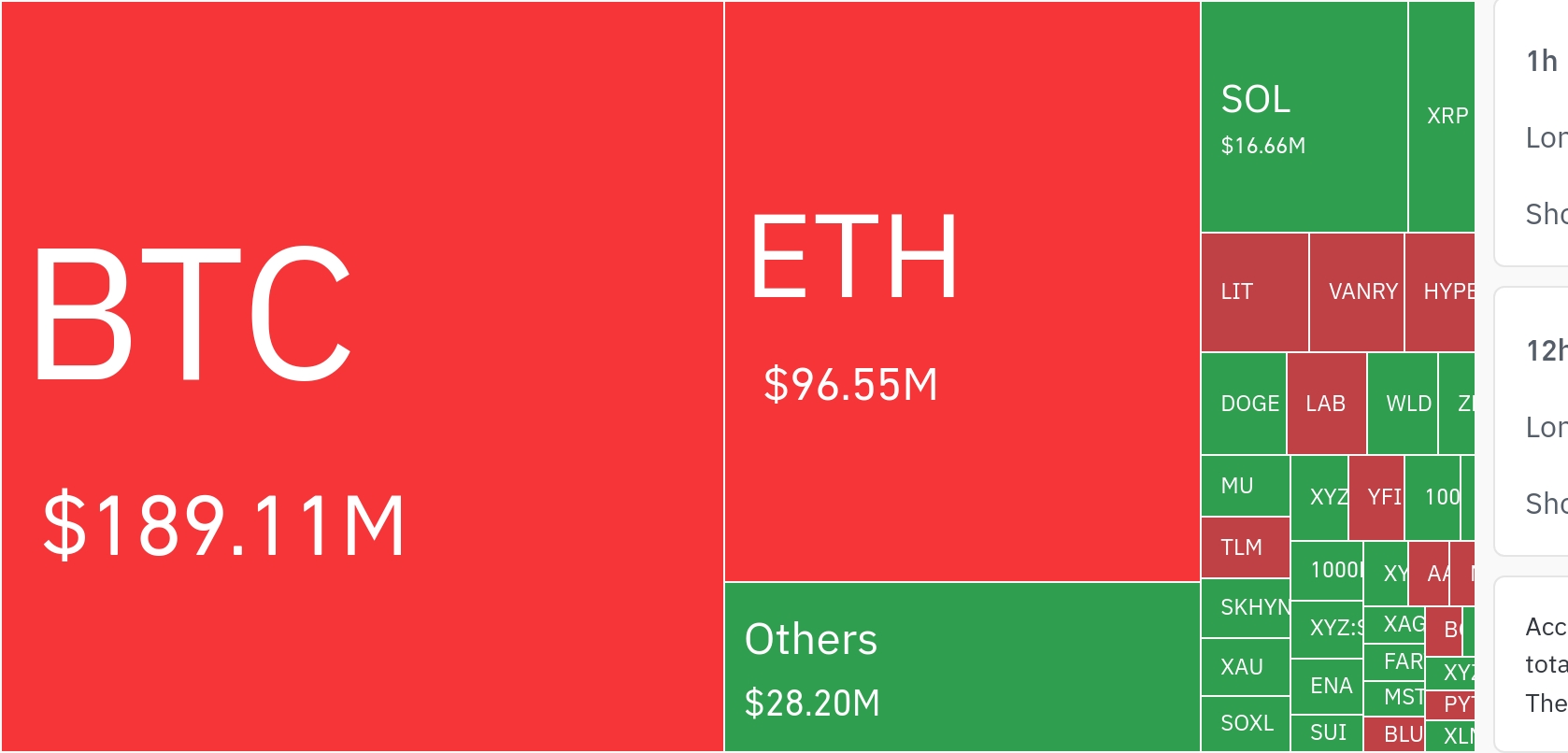

Large-cap leaders powered the move. Bitcoin (BTC) rose 6.60% and Ethereum (ETH) climbed 13.47%, while several major altcoins posted outsized gains. Cardano (ADA) rallied 31.8% and Bitcoin Cash (BCH) surged 27.7%, underscoring a renewed but uneven appetite for beta exposures across the market.

In U.S. spot exchange-traded funds, net outflows continued but moderated compared with the prior week, according to Crypto.com’s figures. Spot Bitcoin (BTC) ETFs saw $526 million in net redemptions, while spot Ethereum (ETH) ETFs recorded $14 million in net outflows. The cooling pace of withdrawals, the report argued, indicates institutional sentiment has not abruptly reversed, even if investors remain cautious about adding exposure aggressively at current levels.

Macro conditions also offered support for risk assets. U.S. nonfarm payrolls increased by just 57,000 in June, easing pressure for further rate hikes and helping improve the backdrop for duration-sensitive and growth-linked assets—including crypto. At the same time, equity markets showed clearer sector rotation, with capital shifting out of richly valued AI-related shares and into value and cyclical names. The Dow Jones Industrial Average ended at 52,900.07, marking the first close above 52,000. Crypto.com Research said the broader easing in macro stress helped stabilize sentiment and underpin the crypto market’s short-term bounce.

Corporate treasury behavior remained a closely watched variable, particularly as publicly listed firms become increasingly important holders of Bitcoin (BTC). Strategy ($MSTR) introduced what it described as a 'digital credit capital framework'—a structure designed to maintain long-term Bitcoin exposure while improving liquidity management. Under the framework, the company approved potential Bitcoin sales of up to $1.25 billion, with proceeds earmarked for dividends, debt repayment, share buybacks, and cash reserves.

Market interpretation has been mixed, but Crypto.com’s report suggested the more common view is that the move reflects balance-sheet optimization rather than a wholesale shift away from Strategy’s long-held bullish posture on Bitcoin. With institutional ownership of crypto expanding, the report added, liquidity and collateralization approaches adopted by listed companies could influence how other corporates evaluate Bitcoin in treasury and capital planning.

Regulatory developments across Europe and key Asia-Pacific markets were highlighted as another major swing factor for the coming quarter. The European Union’s Markets in Crypto-Assets framework (MiCA) entered full application on July 1 UTC as the transition period ended, making comprehensive licensing mandatory for crypto-asset service providers operating across the bloc. In parallel, the European Commission began reviewing potential updates to the existing framework in response to the growth of stablecoins and 'real-world asset' (RWA) tokenization—an acknowledgement that market structure is evolving faster than many rulebooks were designed to accommodate.

In the U.K., the Financial Conduct Authority (FCA) proposed a capital buffer of 1% of issued value for stablecoin issuers—less stringent than MiCA’s 2% level—signaling an attempt to balance regulatory certainty with competitiveness. Australia also moved on July 1 UTC, implementing 'travel rule' requirements for domestic exchanges that mandate collecting and verifying sender and recipient information for qualifying transfers. Crypto.com characterized these measures as less about punitive tightening and more about structural alignment—anti-money laundering controls, consumer safeguards, and formal integration into mainstream finance.

Perhaps most consequential, the report said, is the pace of institutional adoption in stablecoins and tokenization, where traditional finance and crypto-native firms are increasingly converging. An open standards consortium involving more than 140 financial and crypto firms launched a dollar-pegged stablecoin, OpenUSD (OUSD), with a fee-free issuance and redemption model and a structure that returns interest income from reserves to member firms—an approach that challenges conventional stablecoin business models and revenue distribution.

Elsewhere, Standard Chartered and Circle ($CRCL) began offering institutional clients minting and redemption services for USD Coin (USDC) via the Dubai International Financial Centre (DIFC), with an eye toward broader global rollout. BlackRock ($BLK) integrated Ethena’s synthetic dollar, USDe, into its Aladdin risk management platform, while its tokenized fund BUIDL has been positioned as a core reserve asset for new white-label products—signs that stablecoin-like instruments and tokenized cash equivalents are moving deeper into institutional plumbing.

In Europe, Crédit Agricole, through its CACEIS banking unit, issued 20 million units of a MiCA-compliant euro-linked stablecoin, 'EURXT', on the Ethereum (ETH) network. In the U.S., New York Life Investment Management—an asset manager overseeing more than $800 billion—entered the on-chain fund space by launching the 'NYLIM Anemoy fund' on Centrifuge, structured around higher-yield corporate credit exposure.

Crypto.com’s central takeaway is that the current rebound is not just a price story. It is unfolding across three reinforcing pillars: regulatory normalization, accelerating institutional participation, and deeper integration of crypto instruments with financial infrastructure. With Bitcoin (BTC) and Ethereum (ETH) leading the market higher, the report argued that longer-term durability will hinge on the trajectory of ETF flows, cross-jurisdiction regulatory coherence, and whether stablecoin ecosystems continue to expand within regulated rails—developments that could determine whether the next leg of crypto’s cycle is driven by speculative leverage or by institutional utility.

🔎 Market Interpretation

- Price rebound on thinner participation: Crypto markets rose while spot volume (-4.26%) and volatility (-15.76%) fell, implying a calmer rebound with fewer traders driving price—supportive in the short term but potentially fragile if demand doesn’t broaden.

- Large caps led, beta rotated selectively: BTC (+6.60%) and ETH (+13.47%) anchored gains, while pockets of higher-beta altcoins (e.g., ADA +31.8%, BCH +27.7%) surged—suggesting risk appetite is returning, but capital allocation remains uneven.

- ETF flows still a headwind, but pressure easing: U.S. spot ETF outflows persisted (BTC ETFs -$526M, ETH ETFs -$14M) yet slowed versus the prior week—consistent with “cautious, not capitulating” institutional behavior.

- Macro backdrop turned less restrictive: Softer U.S. payrolls (57k) reduced rate-hike pressure, aiding risk assets. Equity sector rotation away from crowded AI trades and into value/cyclicals reinforced the “risk rebalancing” narrative supporting crypto’s bounce.

- Corporate treasuries add a new market lever: Strategy (MSTR) introduced a liquidity-focused "digital credit capital framework," authorizing potential BTC sales up to $1.25B for dividends, debt reduction, buybacks, and reserves—framed as balance-sheet optimization rather than a bearish pivot.

- Next-quarter drivers shift from momentum to structure: The report argues near-term direction is increasingly dictated by regulation, institutional flows, and the evolving stablecoin/tokenization stack rather than headline-driven speculation.

💡 Strategic Points

- Watch “rising price + falling volume” as a confirmation test: If volume and breadth fail to recover, rallies may be more vulnerable to sudden reversals; improving participation would strengthen trend durability.

- Use ETF flow momentum as a regime indicator: Stabilizing or reversing ETF outflows could signal renewed institutional risk-on; continued redemptions may cap upside even if spot prices drift higher.

- Track policy convergence across regions: MiCA’s full application (EU), FCA’s proposed stablecoin buffer (UK), and Australia’s travel rule implementation could reshape where liquidity, issuers, and service providers cluster.

- Stablecoin competition is moving to “plumbing” and economics: OpenUSD’s fee-free model and sharing reserve interest with members challenges incumbent business models; adoption may hinge on distribution, compliance, and institutional integration.

- Institutional rails are expanding: Standard Chartered + Circle enabling USDC mint/redeem in DIFC, BlackRock integrating USDe into Aladdin, and positioning BUIDL as a reserve-like asset suggest tokenized cash equivalents are becoming operational tools, not just trades.

- Tokenization growth broadens investable on-chain yield: NYLIM’s on-chain corporate credit fund (via Centrifuge) highlights the shift toward on-chain credit products—potentially increasing stablecoin utility, collateral demand, and regulated yield offerings.

- Corporate BTC liquidity strategies may set a template: If more public companies adopt collateralization/liquidity frameworks, BTC could behave more like a treasury-managed financial asset—altering supply dynamics during stress and rallies.

📘 Glossary

- Spot Trading Volume: The total value of crypto bought/sold for immediate settlement on exchanges; often used to gauge market participation and conviction.

- Volatility: The magnitude of price fluctuations over time; falling volatility can indicate stabilization or complacency depending on context.

- Beta (Crypto Context): A proxy for how strongly an asset tends to move relative to the broader market; “high-beta” altcoins typically swing more than BTC/ETH.

- Spot ETF: An exchange-traded fund that holds the underlying asset (e.g., Bitcoin) rather than futures; flows can materially influence demand.

- Net Outflows/Redemptions: More ETF shares being redeemed than created, implying capital is leaving the fund and potentially reducing spot demand.

- Nonfarm Payrolls (NFP): A key U.S. jobs report that impacts interest-rate expectations and overall risk appetite.

- MiCA (Markets in Crypto-Assets): The EU’s comprehensive crypto regulatory framework requiring licensing and setting rules for issuers and service providers.

- Travel Rule: AML regulation requiring crypto service providers to collect/verify originator and beneficiary information for certain transfers.

- Stablecoin: A token designed to maintain a stable value (often pegged to USD/EUR), typically backed by reserves or alternative mechanisms.

- RWA Tokenization: Representing real-world assets (e.g., funds, credit, treasuries) on-chain via tokens to improve settlement and programmability.

- Minting/Redemption (Stablecoins): Creating stablecoins in exchange for fiat/reserves (mint) and exchanging stablecoins back for fiat/reserves (redeem).

- Synthetic Dollar (e.g., USDe): A dollar-referenced crypto instrument that targets price stability via derivatives/collateral structures rather than traditional cash reserves.

- Tokenized Fund (e.g., BUIDL): A fund whose shares are issued and transferred on a blockchain, often used as on-chain cash equivalent or collateral.

Comment 0