News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

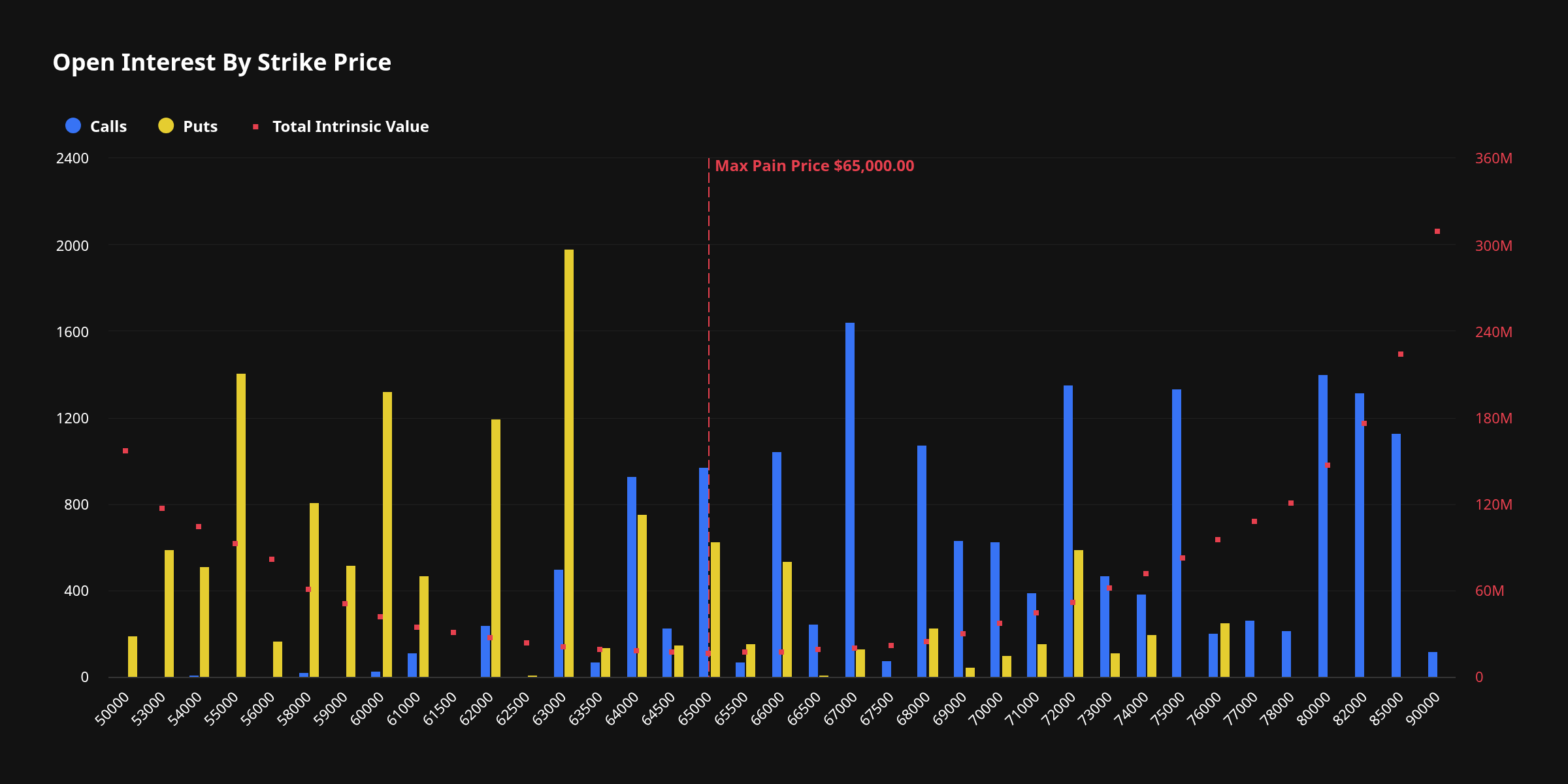

Bitcoin (BTC) options traders are sending mixed signals, with same-day expiry positioning clustered around a $63,000 put while longer-dated open interest remains skewed toward upside bets led by an $80,000 call—highlighting a market that is hedging near-term downside risk even as it keeps one eye on a higher-price regime.

Data from Deribit, the largest cryptocurrency options exchange, showed total Bitcoin options open interest at 30,569 contracts as of Thursday UTC (June 19), representing roughly $1.92 billion in notional value. Call open interest stood at 17,162 contracts versus 13,407 puts, putting the put/call ratio at 0.78—typically interpreted as mildly bullish, as demand for 'call options' outweighs 'put options' in aggregate positioning.

The implied battleground for spot prices was clear: the so-called 'max pain' level—the price at which options buyers would collectively experience the greatest losses at expiry—was estimated around $65,000. While max pain is not a forecast, it is closely watched as a rough marker for where hedging flows and dealer positioning can sometimes amplify short-term price gravitates near key expiries.

In the same-day expiry bucket, open interest was most concentrated in the $63,000 put, suggesting heightened attention to defending that level or protecting against a breakdown below it. Large positioning was also evident in the $67,000 call and the $55,000 put, indicating that traders are simultaneously preparing for a rebound attempt and a sharper downside scenario—a common setup when volatility expectations stay elevated.

Across all expiries, the largest open interest sat in the $80,000 call, reinforcing that a meaningful share of the market continues to express 'upside convexity'—a preference for leveraged exposure to a larger rally. At the same time, the $60,000 put also carried substantial open interest, reflecting persistent demand for downside hedges, while the $75,000 call ranked among the busiest strikes for longer-dated bullish positioning.

Trading activity over the past 24 hours looked more balanced than the open-interest picture. Deribit data showed put volume at 14,425.5 contracts versus call volume at 15,035.0 contracts, with a 24-hour put/call ratio of 0.96—near parity. Still, the slight edge in call volume suggested traders were marginally leaning toward a near-term bounce even as put activity stayed elevated, consistent with a market that is both positioning for recovery and paying protection.

The most actively traded contracts reflected that split. Downside hedging demand was pronounced in puts around $58,000 to $60,000 expiring June 26, while traders also concentrated call buying in the $67,000 to $75,000 range for July 31 expiry—signaling that bullish risk-taking is being expressed further out the curve rather than purely intraday.

Open interest was most concentrated in expiries on Dec. 25 (with calls accounting for 66%), Sept. 25 (64% calls), and June 26 (54% calls). By volume, the busiest expiries were July 31 (80% calls), June 26 (69% puts), and June 19 (52% calls), underscoring how hedging and speculative interest are rotating between near-dated protection and mid-dated upside exposure.

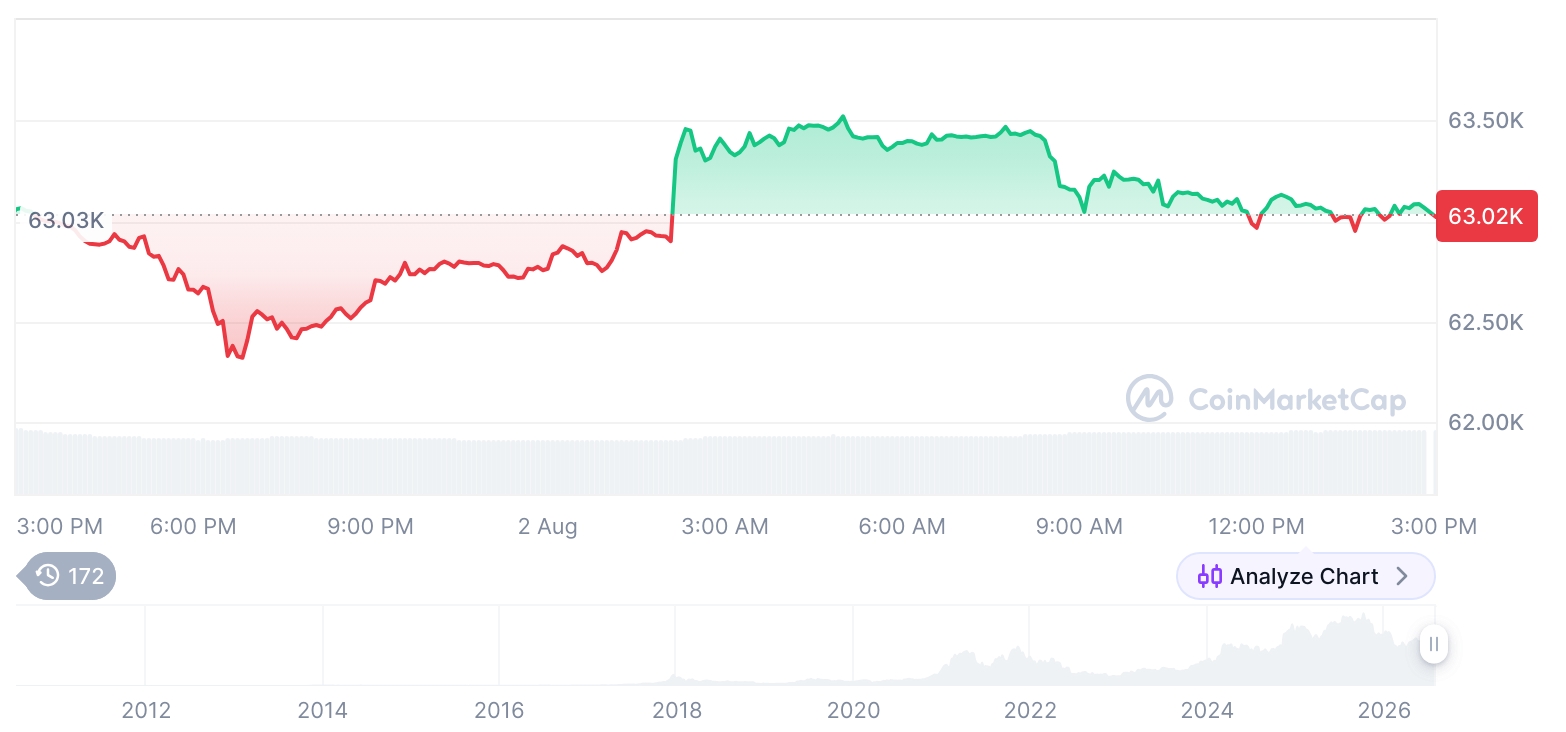

Bitcoin changed hands near $62,955 at 02:35 a.m. ET on June 19, down 2.37% from the prior day, according to TokenPost Market data. The current options backdrop suggests traders remain cautious about near-term downside around the low-$60,000s while maintaining longer-term conviction that a stronger rally—potentially toward the mid-$70,000s to $80,000—remains on the table, depending on broader liquidity conditions and spot-market momentum.

🔎 Market Interpretation

- Mixed options messaging: Near-term positioning is defensive (same-day open interest clustered at the $63,000 put), while longer-dated positioning keeps meaningful upside exposure (largest strike overall is the $80,000 call).

- Overall positioning mildly bullish: Total open interest is 30,569 contracts (~$1.92B notional). Calls (17,162) exceed puts (13,407), producing a put/call ratio of 0.78, typically read as modestly bullish in aggregate.

- Key expiry “gravity” zone: The estimated max pain is ~$65,000, a level watched for potential dealer-hedging flows and short-term price stickiness around expiries (not a price forecast).

- Same-day expiry shows two-sided risk planning: Concentration at the $63K put (breakdown protection) alongside interest in the $67K call (rebound attempt) and $55K put (tail-risk hedge) signals elevated uncertainty and volatility pricing.

- Volume is near neutral: Past 24h volume put/call ratio is 0.96 (near parity), implying balanced trading flow, with a slight call edge suggesting a tentative bounce bias despite persistent put demand.

- Hedging short-dated; upside expressed further out: Active downside hedges cluster in $58K–$60K puts (Jun 26), while call buying concentrates in $67K–$75K calls (Jul 31), indicating traders prefer paying for protection near-term but taking bullish risk in mid-dated maturities.

- Spot context: BTC traded near $62,955 (down 2.37% day/day), aligning with the market’s focus on the low-$60Ks as a near-term stress zone while keeping $75K–$80K as a longer-term upside target range.

💡 Strategic Points

- Near-term risk management dominates: The heavy same-day $63K put interest suggests traders are actively defending/hedging against a break below that level; spot dips toward the low-$60Ks may invite hedging-related flows and faster intraday moves.

- Watch $65K as an options magnet: With max pain near $65K, price may oscillate around this level into key expiries as dealers adjust hedges—especially if spot remains range-bound.

- Upside convexity remains: Large open interest at the $80K call indicates investors are still positioned for an outsized rally; if momentum and liquidity improve, gamma/hedging dynamics could intensify upside moves.

- Two-tier scenario map implied by strikes:

- Bear case: Increased attention to $60K and $55K puts implies concern about an air-pocket move if $63K fails.

- Bull case: Active calls at $67K–$75K and large OI at $80K outline the market’s rally pathway if spot reclaims resistance.

- Expiry rotation matters: By open interest, later expiries (e.g., Sep/Dec) skew call-heavy, while near-dated volume (e.g., Jun 26) shows heavier put usage—suggesting the market is paying for short-term insurance while keeping longer-horizon optimism.

- Practical read-through for traders/investors: Consider the current structure as “hedged bullish”—participants are not abandoning upside views, but they are actively buying downside protection while BTC trades below/around key levels.

📘 Glossary

- Option: A derivative contract giving the right (not obligation) to buy or sell an asset at a specified price by a certain date.

- Call option: Benefits if the underlying price rises above the strike; often used to express bullish exposure.

- Put option: Benefits if the underlying price falls below the strike; commonly used for downside hedging.

- Strike price: The price at which the option can be exercised (e.g., $63K put, $80K call).

- Expiry/Maturity: The date the option contract ends (e.g., same-day, Jun 26, Jul 31, Sep 25, Dec 25).

- Open interest (OI): The number of outstanding option contracts currently held (not yet closed/expired); used to gauge positioning.

- Notional value: The underlying dollar value represented by derivatives exposure (here, ~$1.92B).

- Put/Call ratio: Puts divided by calls (by OI or by volume). Lower values generally imply more bullish positioning; near 1 implies balanced flow.

- Max pain: A theoretical price level where option buyers collectively lose the most at expiry; watched for potential pinning effects, not a prediction.

- Implied volatility: The market’s priced expectation of future volatility; often rises when demand for protection increases.

- Convexity (upside convexity): Non-linear payoff exposure where gains can accelerate if price rises sharply; commonly sought via calls.

- Dealer hedging / gamma effects: Market makers adjust spot/futures hedges based on option exposure, which can amplify or dampen price moves near expiries.

Comment 0