News

News  Coin Information

Coin Information  About us

About us  Customer Service

Customer Service

The U.S. Securities and Exchange Commission (SEC) has signaled a meaningful shift in its posture toward XRP, indicating the token should be treated as a 'digital commodity' rather than a security—while stressing that how Ripple markets and distributes XRP could still trigger securities-law scrutiny.

According to the update, the SEC’s framing separates the asset from the conduct around it: XRP itself is not being characterized as a security, but promotional messaging and sales practices remain a potential enforcement focus. In practical terms, regulators are looking closely at whether Ripple’s sales efforts could create an 'expectation of profit' among buyers—a key element traditionally associated with securities analysis. If XRP distributions are structured or marketed in a way that resembles an investment contract, the SEC suggested securities laws could still apply to those specific transactions.

The distinction matters for the broader market because it reinforces an approach increasingly favored by policymakers: treating many tokens as commodities by default, while policing fundraising-style sales, aggressive marketing, and issuer-driven distribution programs separately. Legal observers say that framework could influence how other large-cap crypto assets are evaluated in future enforcement actions and rulemaking, particularly where token issuers retain substantial influence over supply, messaging, or liquidity programs.

Beyond the regulatory angle, XRP’s utility narrative is also receiving renewed attention. The report said the cross-border payments initiative 'Mbridge,' described as an XRP-based settlement network, moved from a pilot phase into live deployment in March 2026. Multiple countries are reportedly using the technology for state-level payment flows, with expectations that by 2031 a larger share of XRP activity could shift away from retail exchange trading toward automated corridors such as Ripple’s On-Demand Liquidity (ODL) channels and institution-facing settlement pools.

ODL uses XRP as a bridge asset to source just-in-time liquidity—converting from one fiat currency to XRP, then into the destination currency—aiming to cut the time and cost of cross-border transfers. Supporters argue that model challenges traditional correspondent-banking rails by enabling near-real-time settlement, though adoption ultimately depends on regulatory certainty, integration with banking systems, and consistent liquidity in key currency corridors.

Ripple also received approval to establish a trust bank, the report said, granting legal authority to provide traditional financial services such as custody, remittances, and payments. If confirmed, the move would position Ripple less as a token issuer and more as a regulated financial infrastructure provider—an evolution that could lower 'institutional' onboarding friction by aligning corporate operations with compliance expectations familiar to banks, asset managers, and payments firms.

On the supply side, market data cited in the report indicated that roughly 7 billion XRP was withdrawn from exchanges over the past month, pushing exchange-available supply to an all-time low. Large exchange outflows are often interpreted as a sign of increased long-term holding behavior, which can reduce immediate sell-side pressure—though the effect on price depends on broader demand, macro conditions, and liquidity across venues.

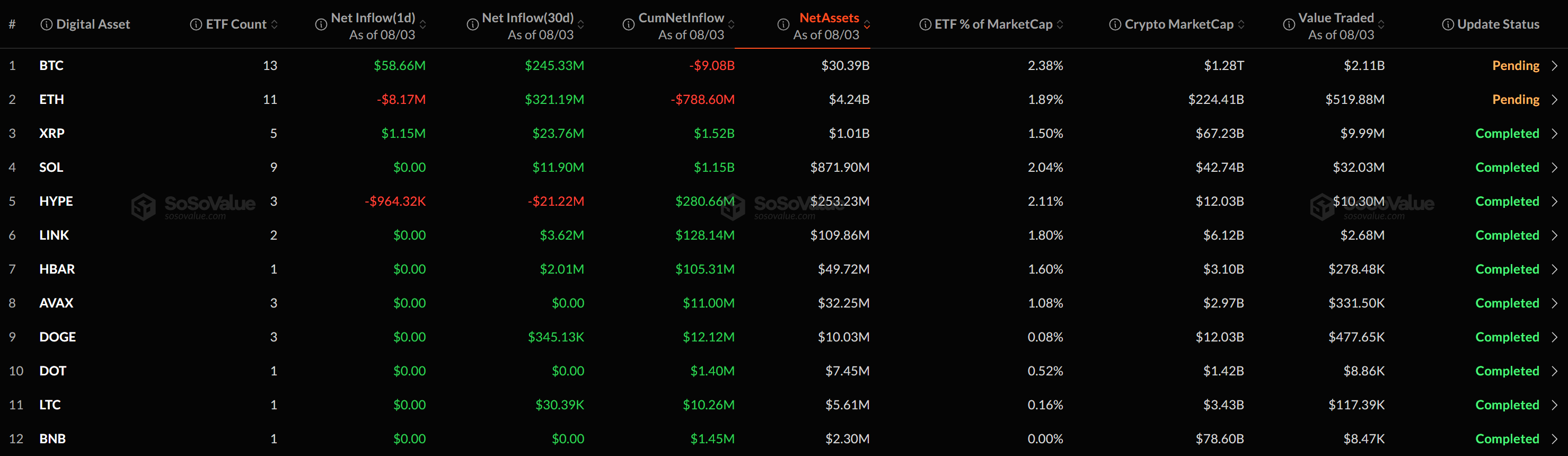

The report pegged XRP’s total supply at 99.9 billion tokens, with circulating supply at 61.2 billion. It estimated a fully diluted valuation of about $144.6 billion and a market share near 3.68%, highlighting XRP’s continued status as a major market asset even as its regulatory classification has remained contested for years.

Analysts quoted in the report argued that a clearer regulatory perimeter—commodities treatment for the asset paired with scrutiny of 'sales mechanics'—combined with expanding payments infrastructure could improve XRP’s long-term prospects for institutional adoption. Near-term price action, however, may remain volatile as the market digests evolving policy signals and as liquidity migrates from retail speculation toward real-world settlement use cases.

If the SEC’s framing holds, XRP’s identity may increasingly tilt away from a retail-driven trading instrument and toward a utility asset used for real-time cross-border settlement—an outcome that could reshape where XRP liquidity concentrates and how market participants value the token within the broader payments ecosystem.

🔎 Market Interpretation

- SEC posture shift: The SEC is signaling XRP may be treated as a digital commodity rather than a security, but it is keeping enforcement attention on how XRP is sold and promoted.

- Asset vs. conduct split: Regulators are separating the token’s nature from transaction mechanics; XRP may be non-security by default, while certain distributions could still be scrutinized as securities offerings.

- Key legal hinge remains buyer expectations: The SEC focus centers on whether Ripple’s marketing/sales create an “expectation of profit”, which can pull specific sales into securities-law territory.

- Policy direction for crypto broadly: The framing reflects a broader approach: treat many tokens as commodities while policing fundraising-style sales, issuer-driven liquidity programs, and promotional campaigns separately.

- Utility narrative strengthening: XRP’s use in cross-border settlement is highlighted via reported Mbridge live deployment (March 2026) and anticipated migration of activity from retail trading to ODL and institutional settlement pools through 2031.

- Institutional positioning: Reported approval for Ripple to establish a trust bank could reposition it as regulated financial infrastructure (custody/remittances/payments), potentially reducing compliance friction for institutional adoption.

- Supply/liquidity signal: ~7B XRP reportedly withdrew from exchanges in a month, pushing exchange supply to an all-time low—often read as more long-term holding, though price impact depends on demand and venue liquidity.

- Market scale remains large: Total supply 99.9B, circulating 61.2B, estimated FDV $144.6B, and market share ~3.68% underscore XRP’s continued prominence amid regulatory evolution.

💡 Strategic Points

- Compliance strategy for issuers: Even if a token is treated as a commodity, teams should design distributions to avoid “investment contract” characteristics (e.g., profit-forward messaging, issuer-led promises, or structured fundraising-like sales).

- Marketing discipline matters: Public statements, incentive programs, and sales channels should be reviewed for language that could imply buyers profit from the issuer’s efforts—often the enforcement trigger even when the asset itself is not labeled a security.

- Watch for transaction-level enforcement: The likely regulatory battleground shifts from “XRP is/isn’t a security” to “which sales are securities transactions,” raising the importance of sale context (counterparty type, disclosures, lockups, incentives).

- Adoption depends on rails + certainty: ODL’s growth hinges on consistent corridor liquidity, bank/payment integrations, and regulatory clarity; institutional usage may expand fastest where these three align.

- Liquidity migration risk/opportunity: If XRP activity shifts toward automated settlement corridors, exchange-driven price discovery could change—potentially lowering retail-driven volatility over time but also altering where liquidity concentrates.

- Interpreting exchange outflows: Lower exchange supply can reduce immediate sell pressure, but it can also thin order books; traders and institutions should monitor on-venue liquidity, spreads, and cross-venue depth.

- Institutional pathway: A trust bank structure (if confirmed) may enable custody and payment services under a regulated framework, helping counterparties meet internal risk and compliance requirements.

📘 Glossary

- Digital commodity: A token treated more like a commodity (e.g., gold/oil) than a security, typically implying different oversight and disclosure obligations than securities.

- Security / investment contract: A regulated financial instrument; in crypto, analysis often centers on whether a sale resembles an “investment contract.”

- Expectation of profit: A key factor in securities analysis—whether buyers are led to expect profits primarily from others’ efforts (e.g., issuer development/marketing).

- Sales mechanics: The structure and execution of token distributions (who sells, to whom, with what incentives/terms, and what is promised or implied).

- ODL (On-Demand Liquidity): Ripple’s model using XRP as a bridge asset—fiat → XRP → destination fiat—to source just-in-time liquidity for cross-border transfers.

- Bridge asset: An intermediary asset used to exchange value between two currencies or networks when direct liquidity is limited or costly.

- Correspondent banking: Traditional cross-border payment rails where banks route transfers through intermediary banks, often slower and more expensive.

- Settlement: Final completion of a transaction—when funds/claims are definitively transferred and recorded.

- Liquidity corridor: A trading/transfer route between two currencies/markets where sufficient volume and depth enable efficient conversion.

- Exchange outflows: Net token withdrawals from centralized exchanges; often interpreted as movement to self-custody or long-term holding.

- Circulating supply: Tokens currently available in the market (excluding locked or non-circulating reserves depending on methodology).

- Fully diluted valuation (FDV): Market cap implied if the entire token supply were in circulation at the current price.

- Trust bank: A regulated financial entity often able to provide custody and certain banking/payment services under a defined supervisory framework.

Comment 0